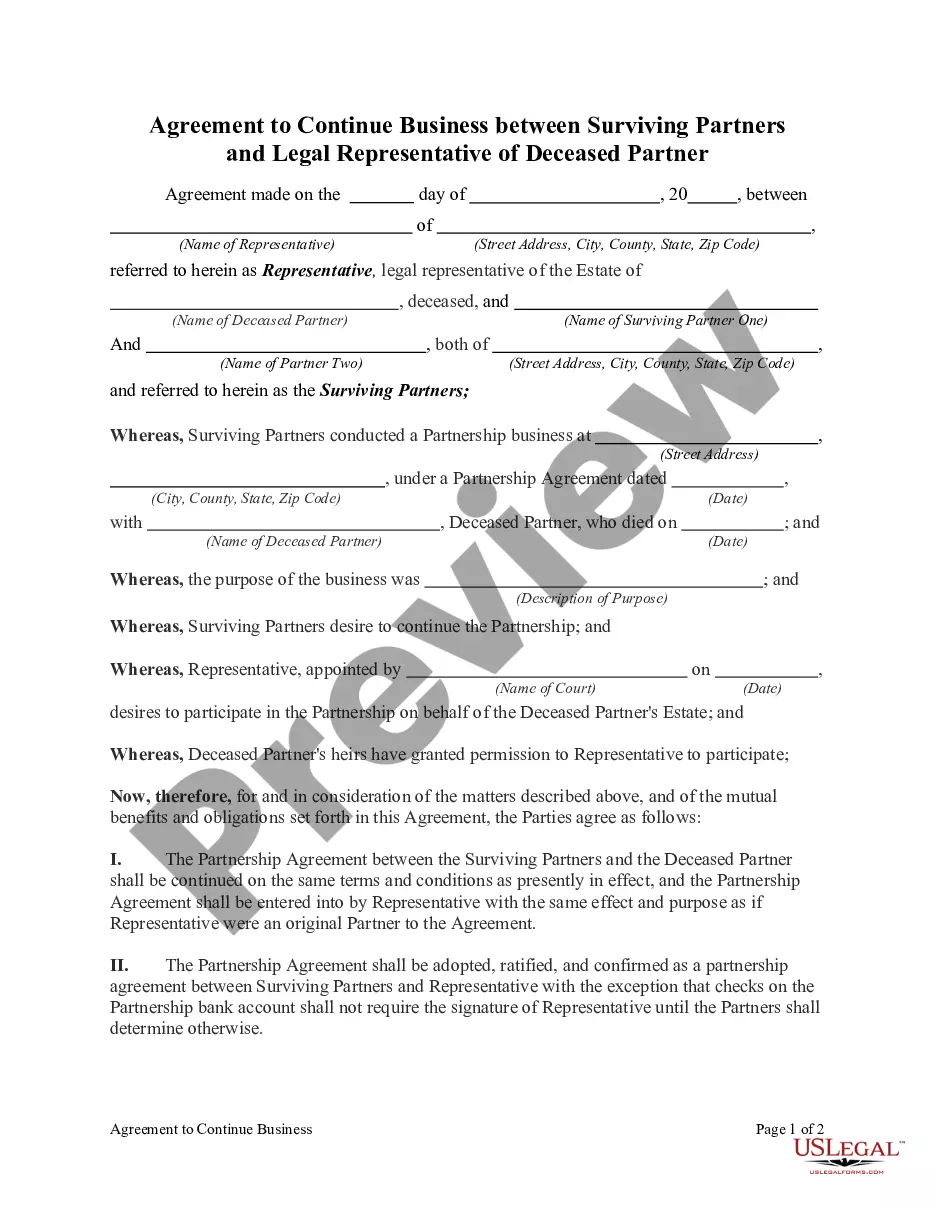

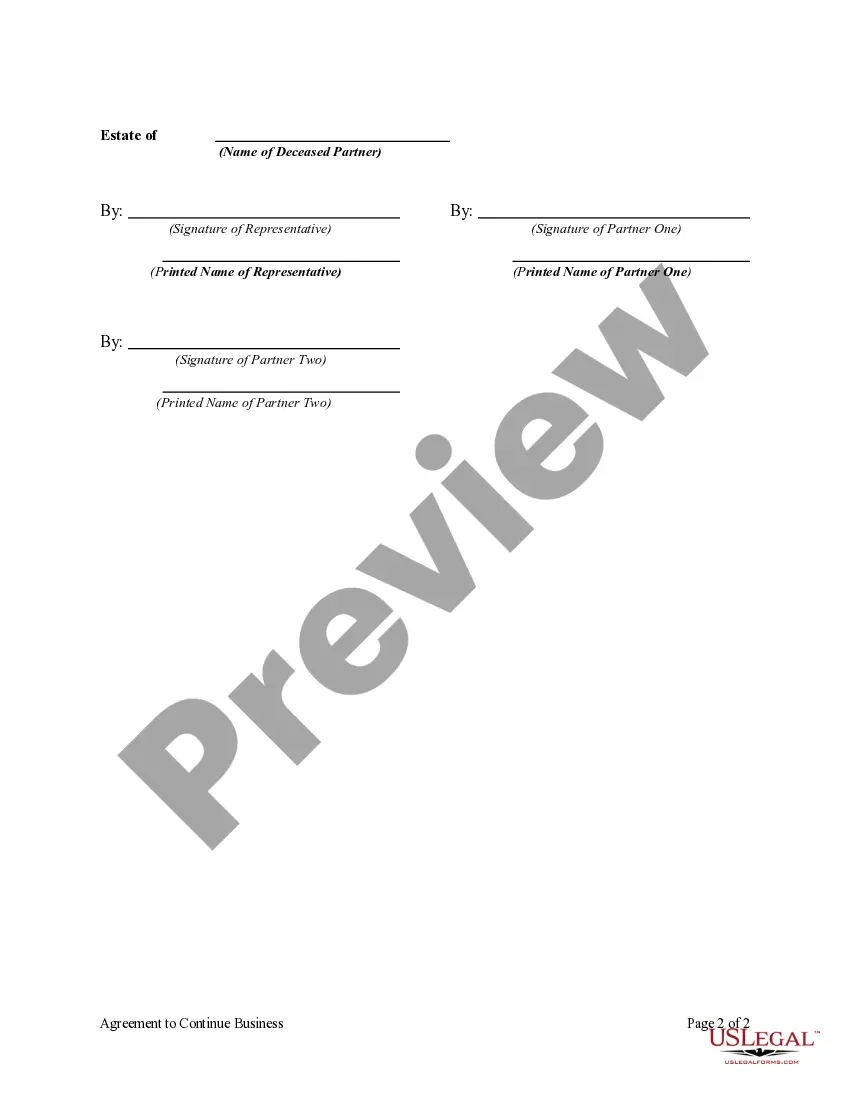

The Rhode Island Agreement to Continue Business Between Surviving Partners and Legal Representative of Deceased Partner is a legal document that regulates the ongoing operations of a business after the death of one of the partners. This agreement outlines the obligations and rights of the surviving partner(s) and the legal representative of the deceased partner. Keywords: Rhode Island, agreement, continue business, surviving partners, legal representative, deceased partner. In Rhode Island, there are two primary types of agreements to continue business between surviving partners and legal representatives of deceased partners. 1. General Partnership Agreement: This type of agreement governs the operations and responsibilities of the partnership during the lifetime of the partners and continues after the death of one partner. It outlines the decision-making process, profit-sharing, and management duties. In the event of the death of a partner, this agreement specifies how the surviving partners and the legal representative of the deceased partner should proceed. 2. Limited Partnership Agreement: This type of agreement is specifically designed for limited partnerships, where there are general partners and limited partners. In the event of the death of a general partner, this agreement defines the rights and responsibilities of the surviving general partners, the limited partners, and the legal representative of the deceased general partner. Both types of agreements include similar provisions and address critical aspects such as the continuation of business operations, distribution of profits and losses, management decisions, and the buyout or settlement process of the deceased partner's interest. Regardless of the type of agreement, it is crucial to consult with legal professionals familiar with Rhode Island partnership laws to ensure compliance and the protection of the surviving partners and the legal representative of the deceased partner's interests.

Rhode Island Agreement to Continue Business Between Surviving Partners and Legal Representative of Deceased Partner

Description

How to fill out Rhode Island Agreement To Continue Business Between Surviving Partners And Legal Representative Of Deceased Partner?

Are you inside a position where you need papers for either organization or personal purposes virtually every time? There are a lot of lawful papers layouts available on the net, but getting types you can rely isn`t effortless. US Legal Forms delivers 1000s of develop layouts, much like the Rhode Island Agreement to Continue Business Between Surviving Partners and Legal Representative of Deceased Partner, that are composed to fulfill state and federal specifications.

In case you are already knowledgeable about US Legal Forms internet site and have a merchant account, merely log in. Next, you may download the Rhode Island Agreement to Continue Business Between Surviving Partners and Legal Representative of Deceased Partner web template.

If you do not offer an bank account and wish to begin to use US Legal Forms, adopt these measures:

- Discover the develop you will need and ensure it is for the right town/region.

- Utilize the Review key to review the form.

- Look at the outline to ensure that you have chosen the proper develop.

- If the develop isn`t what you are searching for, make use of the Lookup discipline to get the develop that fits your needs and specifications.

- When you obtain the right develop, click Buy now.

- Choose the rates strategy you want, fill in the necessary information to create your bank account, and purchase your order with your PayPal or credit card.

- Choose a hassle-free document structure and download your backup.

Find each of the papers layouts you may have bought in the My Forms food selection. You can get a more backup of Rhode Island Agreement to Continue Business Between Surviving Partners and Legal Representative of Deceased Partner any time, if possible. Just select the required develop to download or printing the papers web template.

Use US Legal Forms, the most considerable variety of lawful forms, to save lots of time and stay away from errors. The support delivers appropriately produced lawful papers layouts which you can use for an array of purposes. Create a merchant account on US Legal Forms and start generating your way of life a little easier.