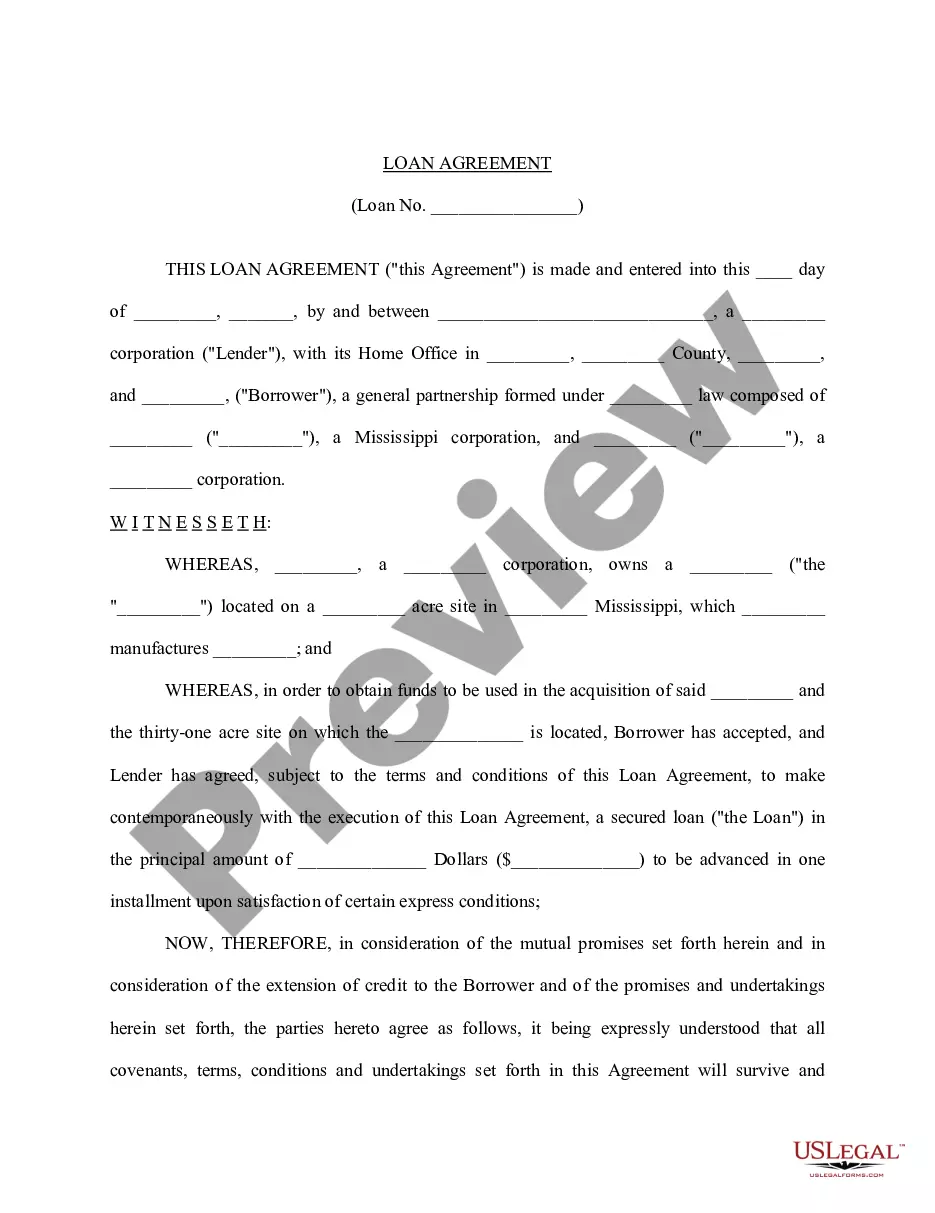

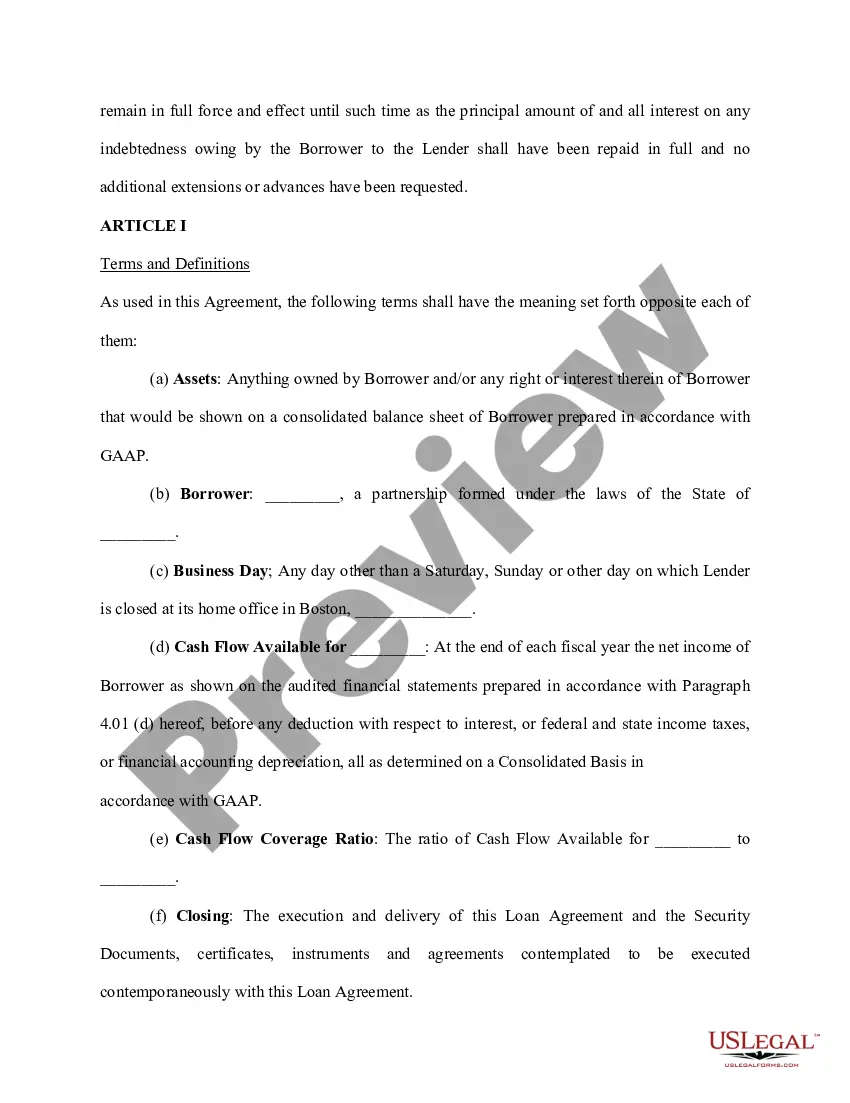

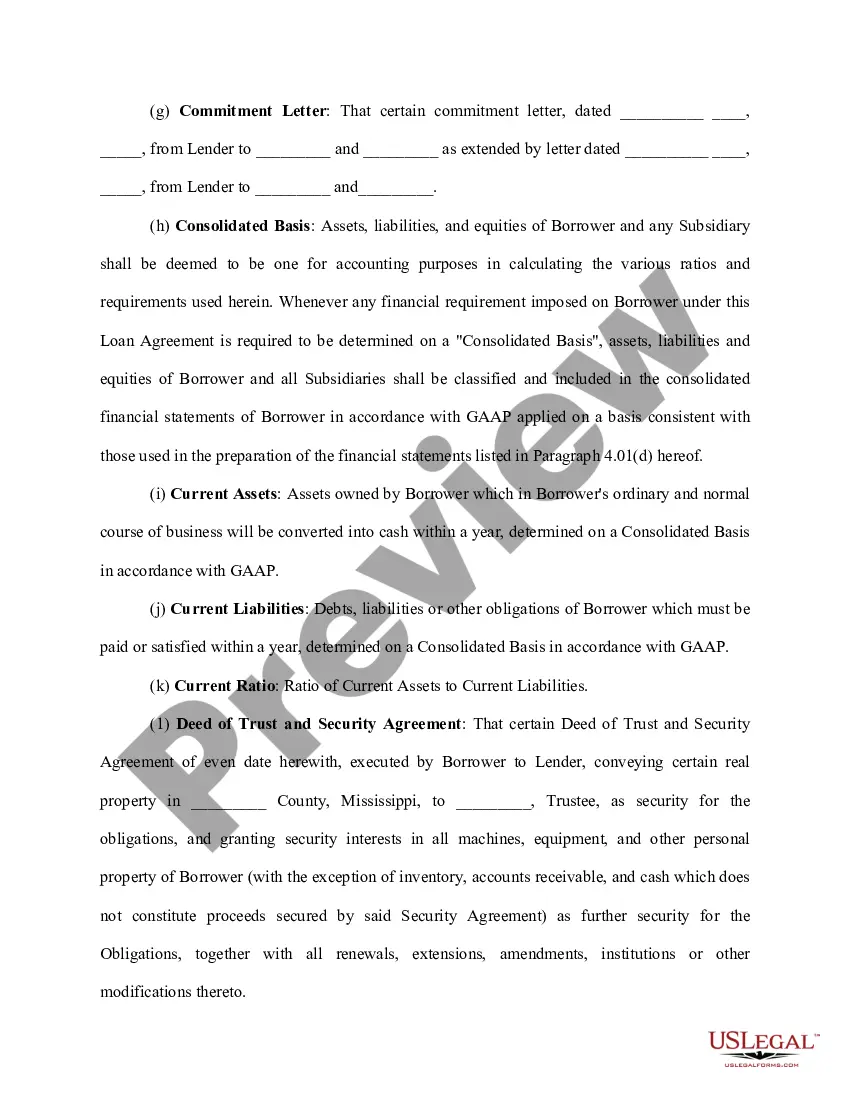

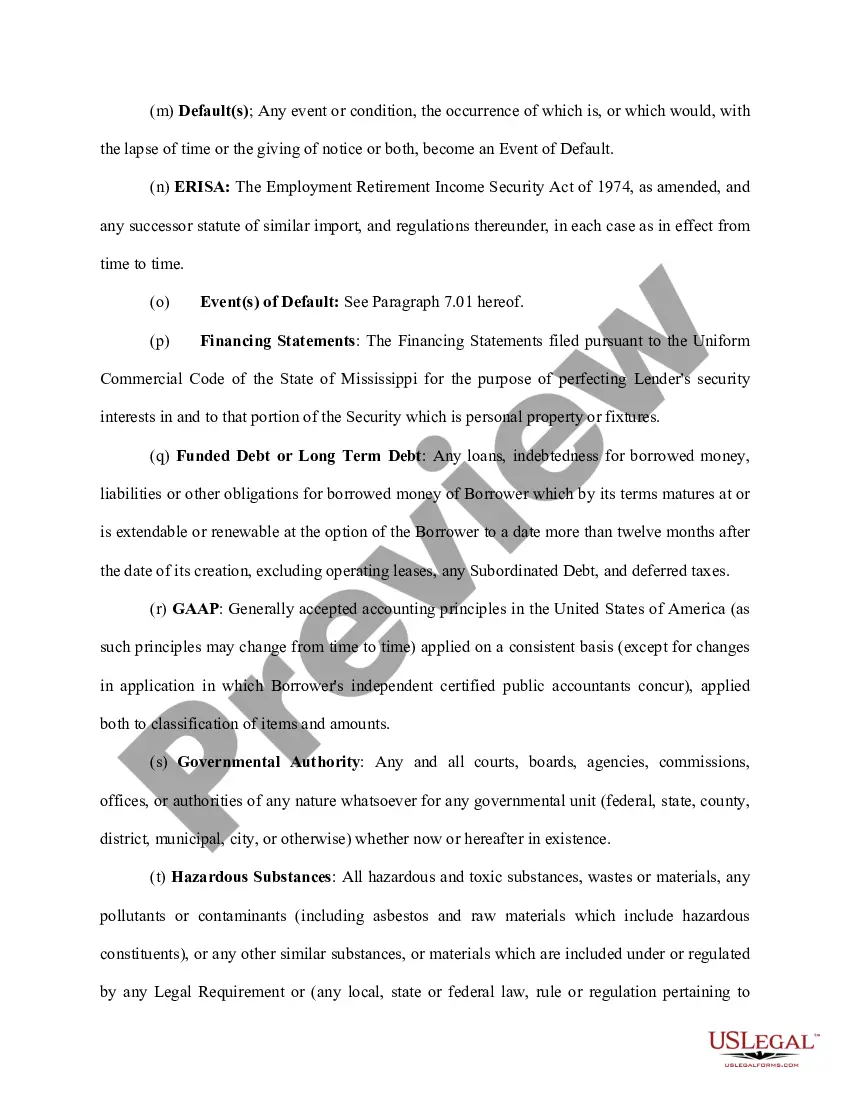

Rhode Island Loan Agreement for Family Member: Understanding the Basics and Types In Rhode Island, a Loan Agreement for Family Member is a legally binding contract between individuals within the same familial relationship, where one party (lender) provides a certain amount of money to another party (borrower) under specific terms and conditions. This agreement ensures clarity, sets expectations, and safeguards the interests of both parties involved. Key elements and terms commonly found in a Rhode Island Loan Agreement for Family Member include: 1. Parties Involved: The agreement begins by clearly identifying the lender (family member providing the loan) and the borrower (family member receiving the loan). 2. Loan Amount: The agreement specifies the exact amount of money being lent to the borrower. This amount can be in the form of cash, check, or other agreed-upon means. 3. Repayment Terms: It is crucial to outline the repayment terms in detail, such as the repayment schedule, whether the loan will be repaid in installments or as a lump sum, and the agreed-upon due dates. 4. Interest: Rhode Island allows family members to charge interest on loans, even though it might not be required. The loan agreement should expressly state whether interest will be charged and at what rate, if applicable. 5. Collateral or Security: If the lender wants to secure the loan against any property or asset (commonly referred to as collateral), such details should be clearly mentioned in the agreement. 6. Late Payment & Default: The agreement should outline the consequences of late payments and the actions that will be taken in case of default. This usually includes late payment penalties, collection fees, and the right to pursue legal action. 7. Governing Law: It is important to state that the agreement will be governed by the laws of the state of Rhode Island, ensuring legal compliance and protection for both parties. Types of Loan Agreements for Family Members in Rhode Island: 1. Secured Loan Agreement: This type of agreement involves collateral or security against the loan amount. If the borrower fails to repay the loan, the lender possesses the right to claim the collateral as repayment. 2. Promissory Note: A promissory note is a simpler form of a loan agreement that primarily focuses on stating the terms of repayment without delving into the extensive details seen in a comprehensive loan agreement. 3. Demand Loan Agreement: A demand loan agreement provides flexibility by allowing the lender to call for complete repayment at any time without specified repayment dates or installments. 4. Installment Loan Agreement: If the lender prefers that the loan be repaid in regular installments over a specific period, an installment loan agreement provides the structure needed to ensure timely repayments. Remember, it is always recommended consulting with a qualified attorney when drafting or entering into a loan agreement to ensure compliance with Rhode Island laws and to protect both parties involved in the loan transaction.

Rhode Island Loan Agreement for Family Member

Description

How to fill out Rhode Island Loan Agreement For Family Member?

You can devote several hours online searching for the legitimate document design that fits the state and federal demands you want. US Legal Forms provides thousands of legitimate varieties which can be examined by professionals. You can actually acquire or print out the Rhode Island Loan Agreement for Family Member from the support.

If you currently have a US Legal Forms bank account, you are able to log in and click the Obtain key. After that, you are able to total, revise, print out, or sign the Rhode Island Loan Agreement for Family Member. Each and every legitimate document design you acquire is yours for a long time. To acquire another duplicate associated with a bought develop, visit the My Forms tab and click the related key.

If you work with the US Legal Forms web site the first time, stick to the easy recommendations listed below:

- First, make certain you have chosen the right document design for that county/city of your choice. Browse the develop explanation to ensure you have picked the correct develop. If offered, take advantage of the Preview key to appear from the document design too.

- If you would like discover another edition in the develop, take advantage of the Lookup field to obtain the design that meets your needs and demands.

- Once you have discovered the design you want, simply click Acquire now to carry on.

- Pick the prices strategy you want, type your credentials, and register for a merchant account on US Legal Forms.

- Complete the deal. You can use your charge card or PayPal bank account to cover the legitimate develop.

- Pick the file format in the document and acquire it to the product.

- Make adjustments to the document if possible. You can total, revise and sign and print out Rhode Island Loan Agreement for Family Member.

Obtain and print out thousands of document layouts while using US Legal Forms web site, which provides the greatest selection of legitimate varieties. Use skilled and express-specific layouts to tackle your organization or personal requirements.