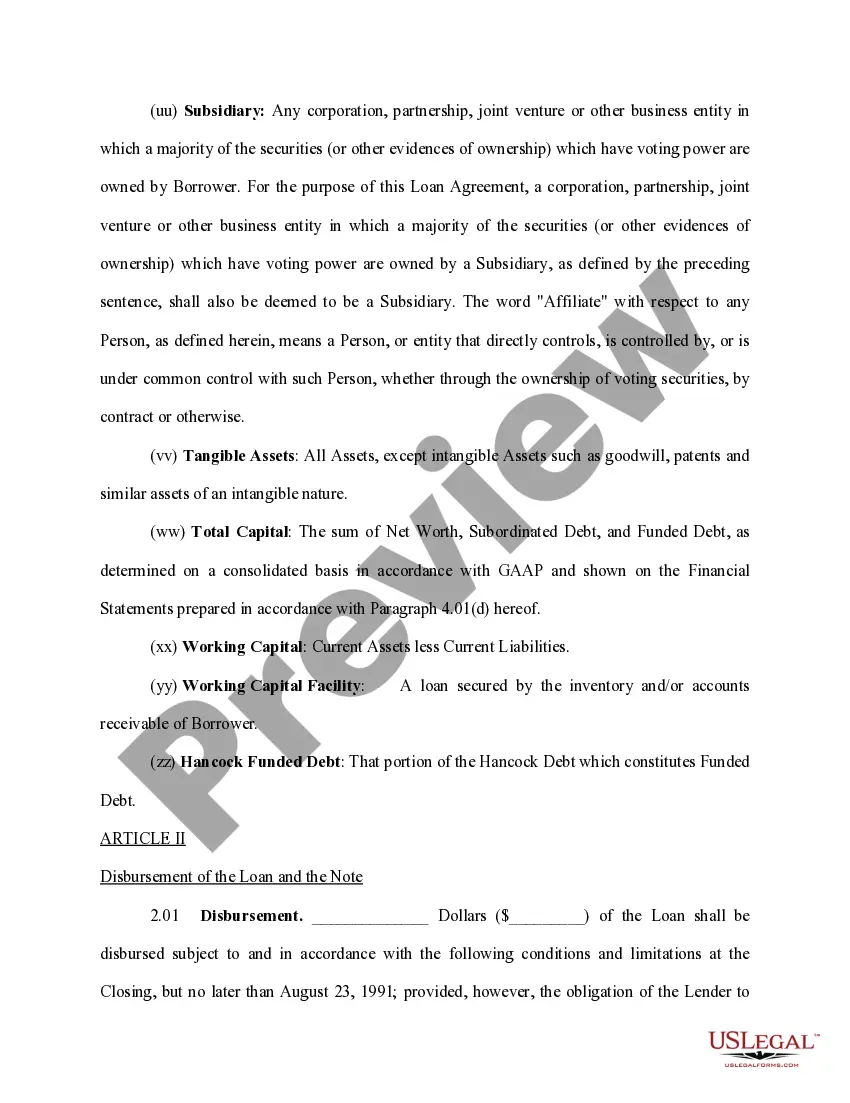

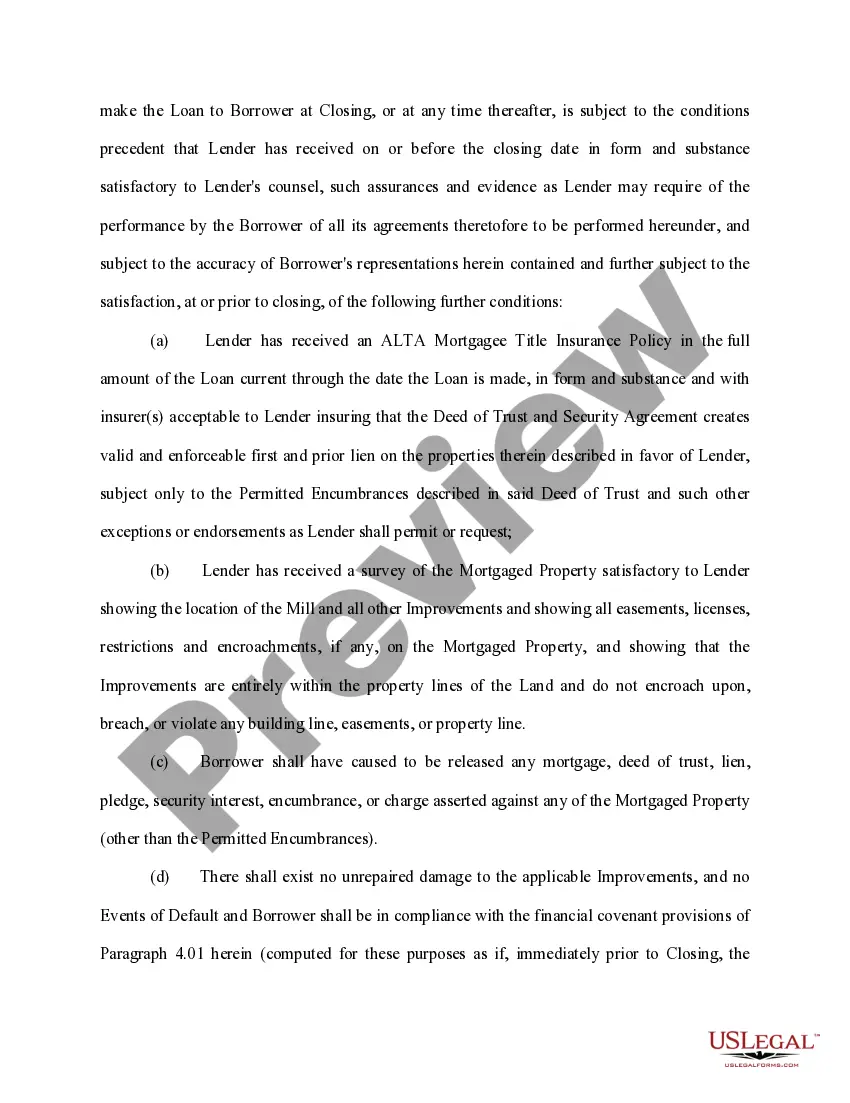

Rhode Island Loan Agreement for Equipment is a legal document that outlines the terms and conditions under which an equipment loan is granted in Rhode Island. This agreement serves as a binding contract between two parties; the lender, typically a financial institution or leasing company, and the borrower, who wishes to borrow the equipment for a specified period. The Rhode Island Loan Agreement for Equipment typically includes the following key elements: 1. Parties Involved: The agreement clearly specifies the names and addresses of the lender (also known as the lessor) and the borrower (also known as the lessee). 2. Description of Equipment: This section provides a detailed description of the equipment being loaned, including its make, model, serial number, and any other relevant details that ensure its proper identification. 3. Purpose of Loan: The agreement stipulates the purpose for which the equipment will be used, whether it is for commercial, industrial, or personal use. 4. Loan Term: This section outlines the duration of the loan, including the start and end dates. It also mentions the possibility of extension or renewal of the loan term at the mutual agreement of both parties. 5. Conditions of Use: The agreement specifies the conditions under which the equipment may be used, including any restrictions or limitations imposed by the lender. It may also include regulations regarding maintenance, repair, and insurance requirements for the equipment. 6. Rental Payments: The agreement outlines the rental or loan payment terms, including the due dates, payment frequency, and the method of payment the borrower must follow. It may also mention any late payment penalties or additional charges applicable in case of default. 7. Security Deposit or Collateral: Some loan agreements require a security deposit or collateral to secure the equipment loan. This section details the amount and terms related to the security deposit, if applicable. 8. Liability and Insurance: This section clarifies the responsibilities and liabilities of both parties regarding the equipment, including any damages or losses that may occur during the loan term. It also specifies the insurance requirements for the equipment, such as the minimum coverage or policy types. 9. Default and Termination: The agreement outlines the consequences of defaulting on the loan, including the lender's right to terminate the agreement and repossess the equipment. It may also mention the dispute resolution process or penalties associated with early termination. Types of Rhode Island Loan Agreement for Equipment: 1. Commercial Equipment Loan Agreement: This type of agreement is used when a business or organization borrows equipment for commercial purposes such as manufacturing, construction, or transportation. 2. Personal Equipment Loan Agreement: This agreement is utilized when an individual borrower wants to borrow equipment for personal use, like household appliances, power tools, or recreational equipment. 3. Lease Agreement for Equipment: Although not precisely a loan agreement, a lease agreement allows the lessee to use the equipment in exchange for periodic rental payments. This type of agreement may have a longer-term and involve provisions for maintenance and repair.

Rhode Island Loan Agreement for Equipment

Description

How to fill out Rhode Island Loan Agreement For Equipment?

If you wish to comprehensive, down load, or print out legal record themes, use US Legal Forms, the most important variety of legal kinds, that can be found on the web. Use the site`s basic and convenient look for to discover the files you need. A variety of themes for enterprise and personal functions are categorized by types and suggests, or keywords. Use US Legal Forms to discover the Rhode Island Loan Agreement for Equipment in just a handful of click throughs.

In case you are currently a US Legal Forms consumer, log in to your account and click on the Obtain button to find the Rhode Island Loan Agreement for Equipment. Also you can entry kinds you previously delivered electronically within the My Forms tab of your account.

If you are using US Legal Forms the first time, refer to the instructions under:

- Step 1. Be sure you have chosen the form for the correct area/nation.

- Step 2. Take advantage of the Review choice to check out the form`s content. Don`t overlook to read through the outline.

- Step 3. In case you are unsatisfied with all the form, make use of the Look for discipline on top of the display to get other variations of your legal form web template.

- Step 4. Once you have identified the form you need, click the Buy now button. Opt for the costs strategy you prefer and add your accreditations to sign up for the account.

- Step 5. Process the financial transaction. You should use your Мisa or Ьastercard or PayPal account to perform the financial transaction.

- Step 6. Select the formatting of your legal form and down load it on the gadget.

- Step 7. Comprehensive, modify and print out or sign the Rhode Island Loan Agreement for Equipment.

Each legal record web template you acquire is the one you have for a long time. You possess acces to each form you delivered electronically within your acccount. Go through the My Forms area and choose a form to print out or down load once more.

Remain competitive and down load, and print out the Rhode Island Loan Agreement for Equipment with US Legal Forms. There are many expert and state-distinct kinds you can use for your enterprise or personal needs.