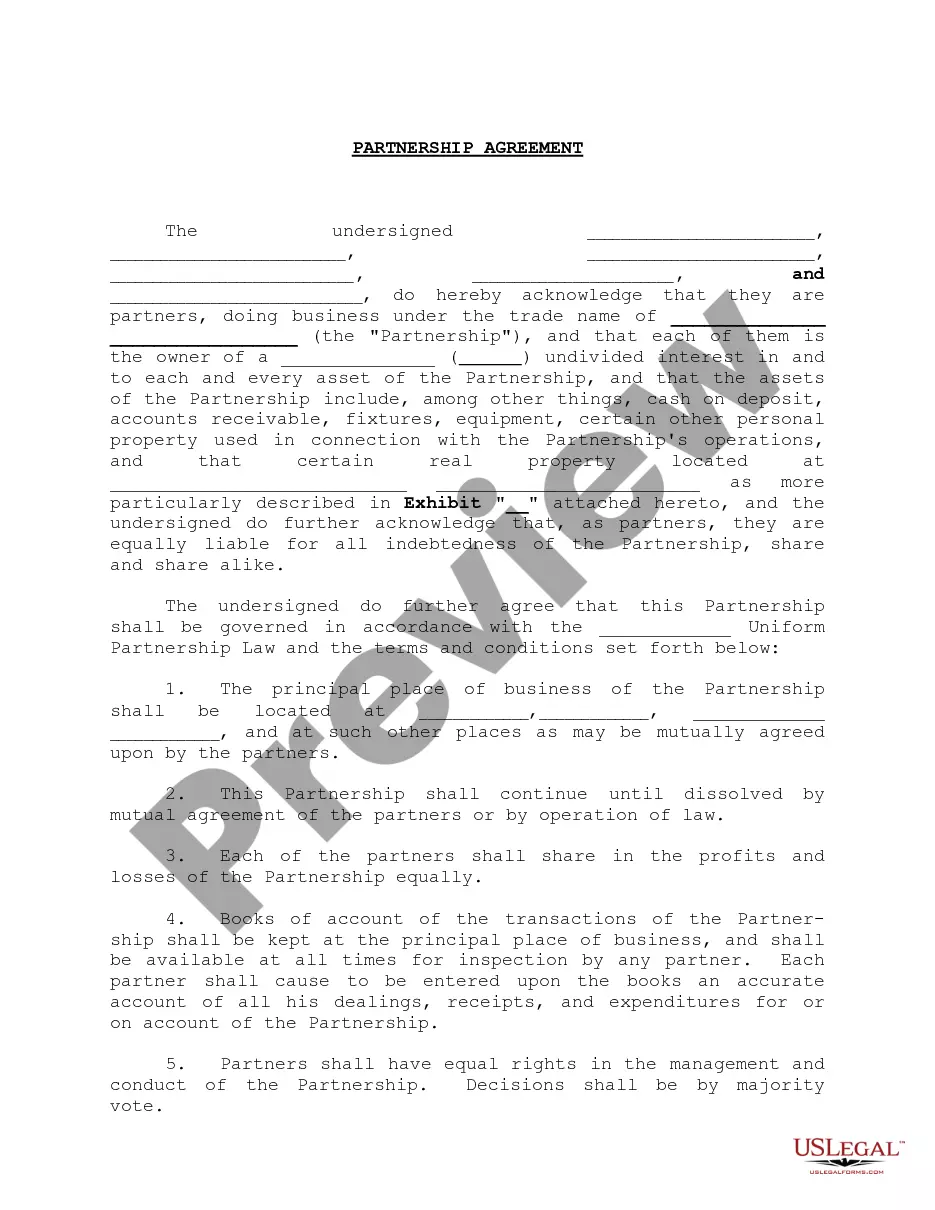

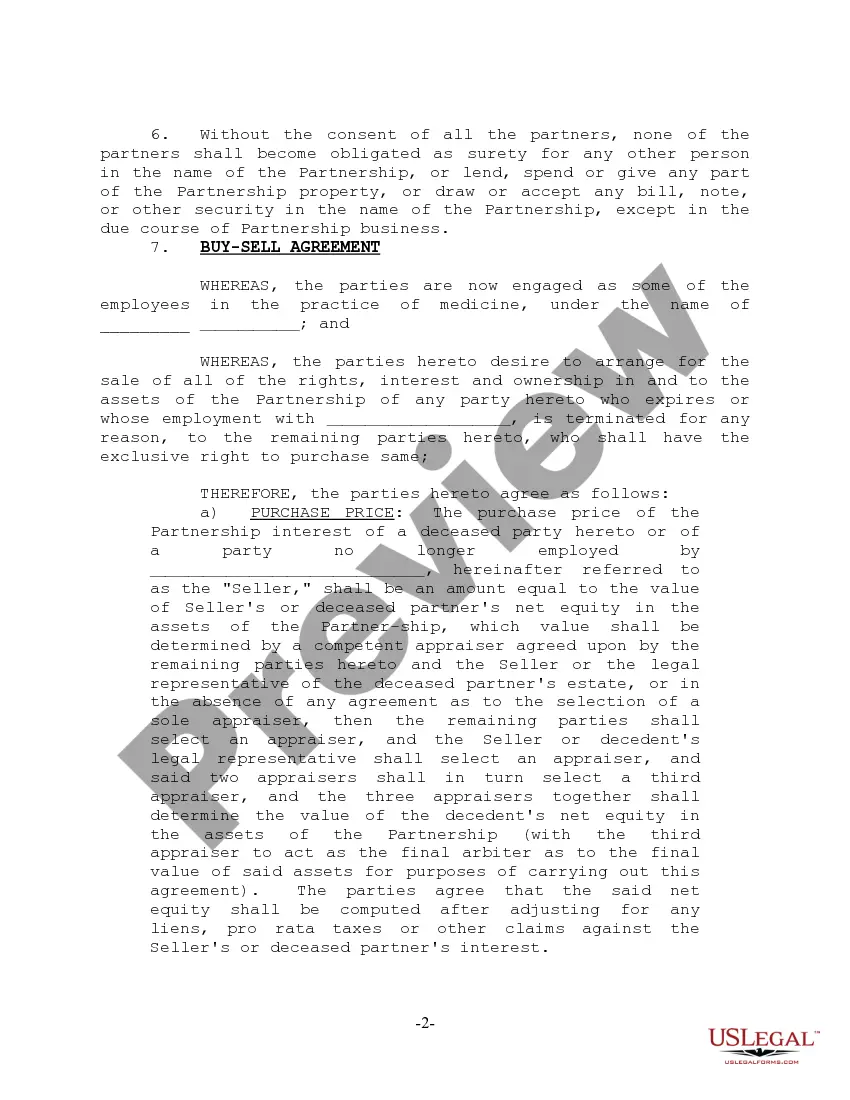

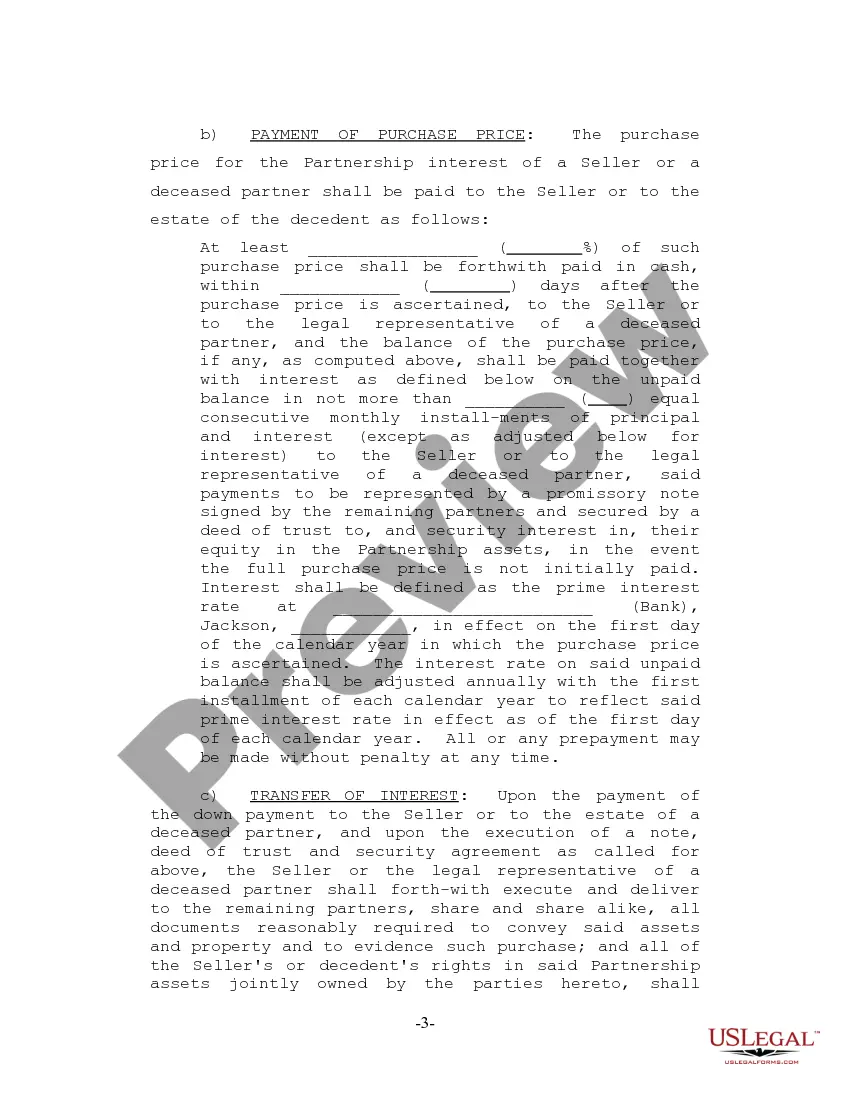

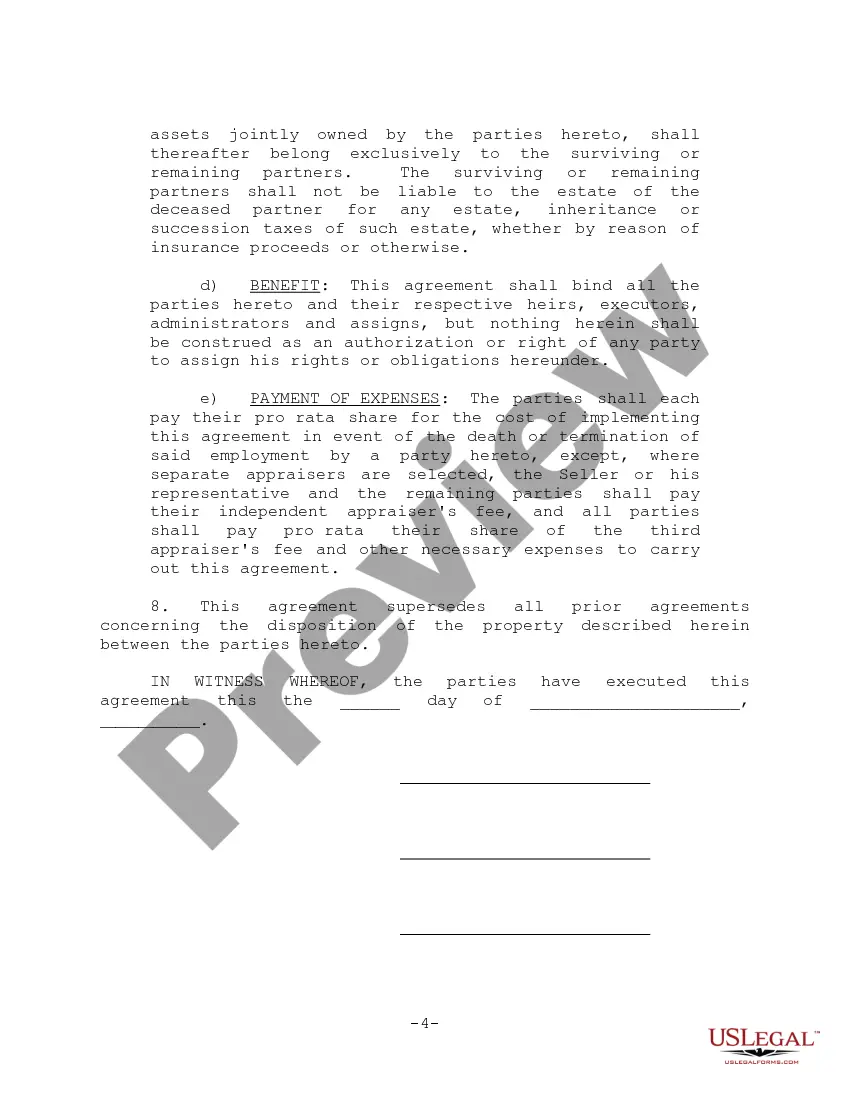

Rhode Island Partnership Agreement for Business is a legally binding contract that outlines the terms and conditions agreed upon by two or more individuals or entities who decide to form a partnership in the state of Rhode Island. This agreement stipulates the rights, responsibilities, and obligations of each partner involved in the business venture. Partnership agreements are essential for establishing clarity and preventing misunderstandings between partners regarding their roles, contributions, profit-sharing, decision-making authority, and resolution of disputes. By entering into a partnership agreement, the partners are effectively laying the foundation for a successful and harmonious business relationship. In Rhode Island, there are primarily two types of partnership agreements for businesses: general partnerships and limited partnerships. 1. General Partnership: This type of partnership involves all partners having equal authority and responsibility in managing the business. Each partner shares both the profits and losses, contributes to the decision-making process, and assumes unlimited personal liability for the partnership's debts and obligations. 2. Limited Partnership: A limited partnership consists of at least one general partner and one or more limited partners. The general partner holds the responsibility for managing the business and has unlimited personal liability for the partnership's obligations. On the other hand, limited partners have limited liability, meaning their personal assets are not at risk beyond their invested capital. Limited partners usually provide capital or resources to the business but do not participate in the day-to-day operations or decision-making process. Both general and limited partnership agreements need to address crucial aspects, including the duration of the partnership, the purpose of the partnership, the capital contributions by each partner, the profit and loss distribution, the decision-making process, the method of dispute resolution, and the procedures for partnership dissolution. In addition to these standard elements, a Rhode Island partnership agreement may also cover additional provisions such as non-compete clauses, management succession plans, buy-sell agreements, or restrictive covenants to safeguard the interests of the partners. It is crucial for partners to seek legal counsel while drafting and executing a partnership agreement to ensure compliance with Rhode Island partnership laws and to customize the agreement to meet the specific needs and objectives of the business. By establishing a clear and comprehensive Rhode Island Partnership Agreement for Business, partners can lay a solid foundation for their business venture, minimize potential conflicts, protect their individual interests, and pave a path towards long-term success and prosperity.

Rhode Island Partnership Agreement for Business

Description

How to fill out Rhode Island Partnership Agreement For Business?

You may devote hours on the Internet trying to find the legal record design that meets the state and federal requirements you will need. US Legal Forms provides a huge number of legal kinds which can be evaluated by experts. You can easily obtain or produce the Rhode Island Partnership Agreement for Business from the assistance.

If you already have a US Legal Forms account, you may log in and click on the Download button. After that, you may total, change, produce, or sign the Rhode Island Partnership Agreement for Business. Every single legal record design you acquire is your own permanently. To have yet another copy of the purchased develop, visit the My Forms tab and click on the related button.

Should you use the US Legal Forms web site for the first time, follow the straightforward recommendations beneath:

- Very first, make sure that you have selected the proper record design for the region/area that you pick. See the develop explanation to make sure you have picked the proper develop. If readily available, take advantage of the Review button to search through the record design also.

- In order to locate yet another version of the develop, take advantage of the Look for industry to obtain the design that meets your requirements and requirements.

- When you have identified the design you need, click Purchase now to proceed.

- Select the costs program you need, enter your accreditations, and sign up for your account on US Legal Forms.

- Total the deal. You may use your Visa or Mastercard or PayPal account to pay for the legal develop.

- Select the formatting of the record and obtain it for your device.

- Make changes for your record if possible. You may total, change and sign and produce Rhode Island Partnership Agreement for Business.

Download and produce a huge number of record themes using the US Legal Forms website, that provides the biggest variety of legal kinds. Use expert and condition-particular themes to take on your small business or person requires.