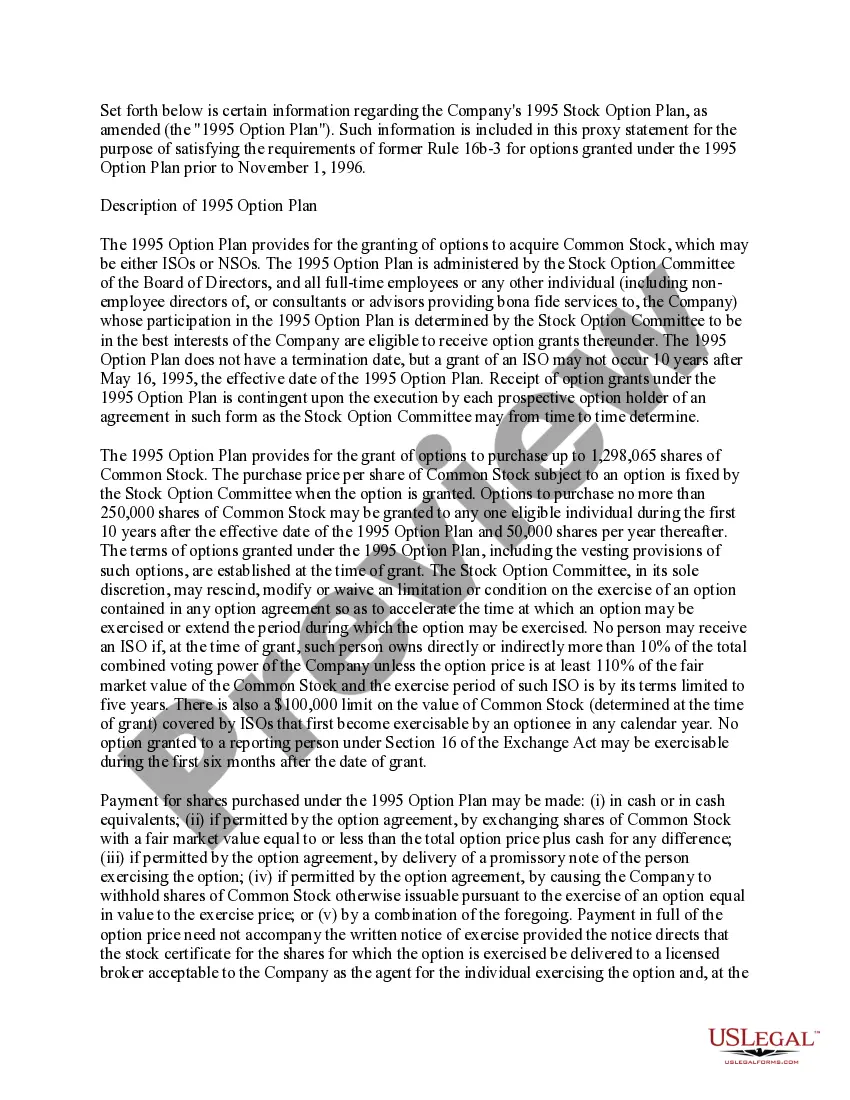

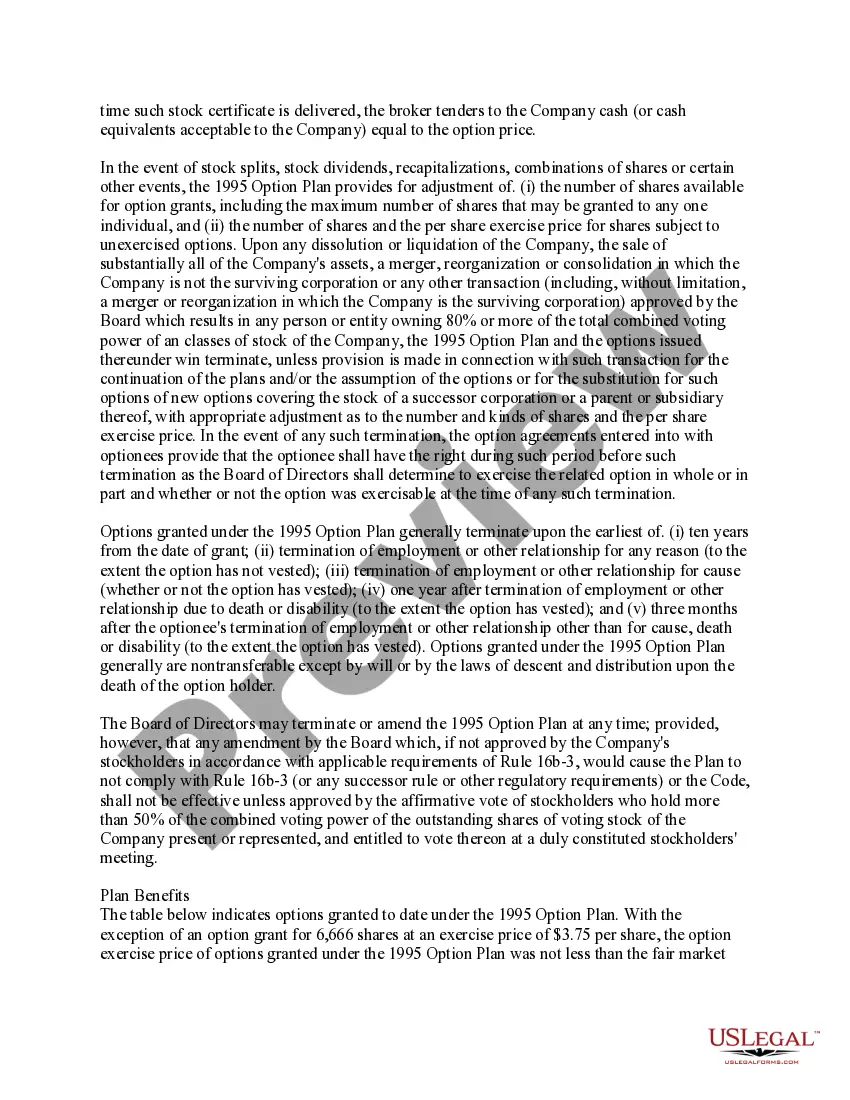

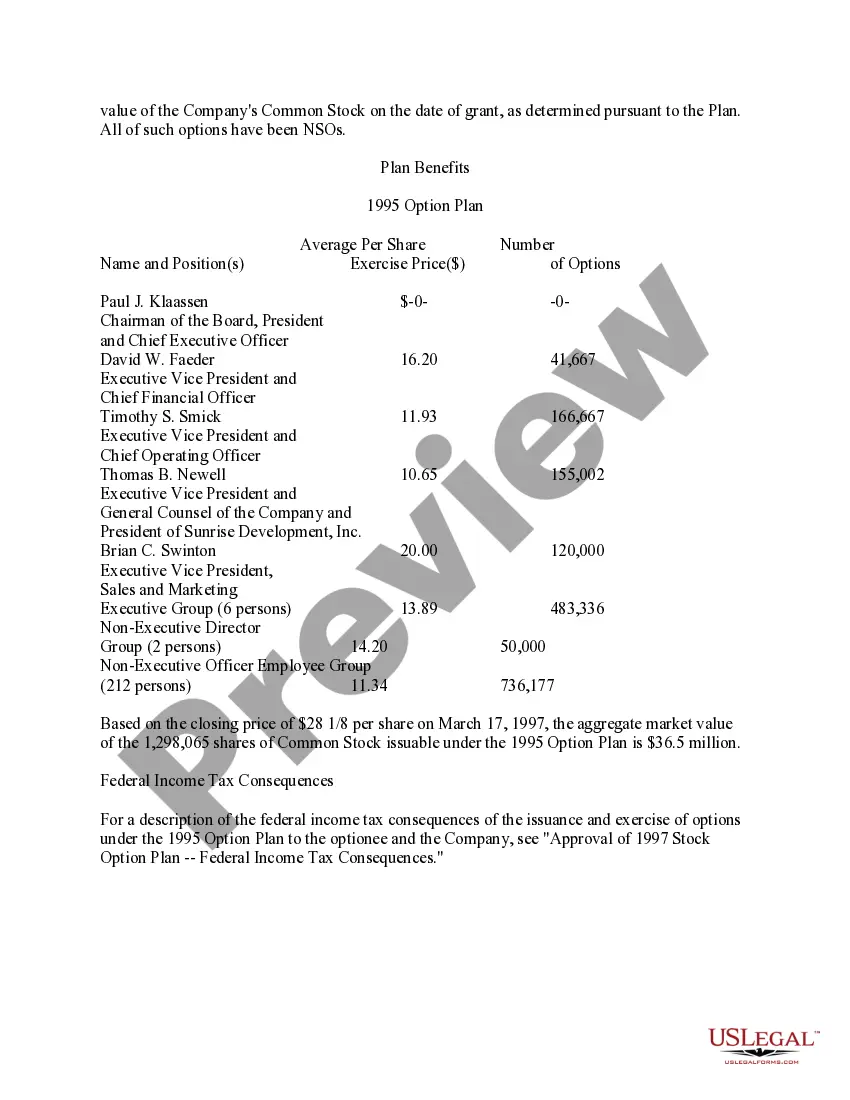

Rhode Island Approval of Stock Option Plan is a legal procedure involving the authorization and acceptance of a company's stock option plan by the state of Rhode Island. This plan gives a company the ability to grant stock options to its employees, allowing them to purchase company shares at a predetermined price within a specific timeframe. The process of obtaining Rhode Island Approval of Stock Option Plan involves several steps. Firstly, the company must draft a comprehensive stock option plan outlining the terms and conditions of the options being offered. This plan needs to be in compliance with both state and federal securities laws. Once the stock option plan is prepared, the company needs to submit an application to the Rhode Island Department of Business Regulation (DBR) or any other relevant regulatory body. The application typically includes the stock option plan, as well as supporting documents such as financial statements, shareholder agreements, and any other information deemed necessary. During the review process, the regulatory body assesses the stock option plan to ensure it adheres to state laws, protects the interests of employees, and promotes transparency. They may also scrutinize the financial stability of the company to determine its ability to fulfill stock option obligations. If the Rhode Island DBR approves the stock option plan, the company is then granted permission to implement it. Employees can be notified of the availability of stock options, and the company can commence granting options according to the plan's terms and conditions. Rhode Island Approval of Stock Option Plans may have variations depending on the type of business or industry. Some common types include: 1. Employee Stock Option Plan (ESOP): This plan is designed specifically for employees of a company, enabling them to acquire ownership in the company by purchasing stock options. 2. Incentive Stock Option Plan (ISO): These plans are usually offered to key employees, executives, or directors as a means to align their incentives with the company's performance. ISO plans often provide tax advantages to participants but must adhere to strict requirements laid out by the Internal Revenue Service (IRS). 3. Non-Qualified Stock Option Plan (NO): NO plans are typically offered to consultants, contractors, or other individuals who are not employees of the company. These plans do not qualify for the same tax benefits as ISO plans but offer greater flexibility in terms of design. 4. Restricted Stock Option Plan: This type of plan may be offered to employees or other individuals, granting them stock options subject to certain restrictions or conditions. The restrictions can include vesting periods or performance-based criteria that need to be met before exercising the options. It is crucial for companies to follow the proper legal procedures to obtain Rhode Island Approval of Stock Option Plan, as failing to do so can result in severe penalties and legal consequences. Employers should consult legal professionals or the Rhode Island DBR for specific guidelines and requirements pertaining to their stock option plans.

Rhode Island Approval of Stock Option Plan

Description

How to fill out Rhode Island Approval Of Stock Option Plan?

US Legal Forms - among the largest libraries of legal varieties in the USA - delivers an array of legal document themes it is possible to down load or produce. Making use of the internet site, you will get 1000s of varieties for organization and individual reasons, categorized by types, says, or key phrases.You will find the most recent types of varieties much like the Rhode Island Approval of Stock Option Plan in seconds.

If you have a monthly subscription, log in and down load Rhode Island Approval of Stock Option Plan from the US Legal Forms local library. The Down load button can look on each type you look at. You gain access to all previously saved varieties within the My Forms tab of the account.

If you want to use US Legal Forms the very first time, listed here are simple directions to obtain started out:

- Be sure to have selected the right type to your city/area. Go through the Preview button to check the form`s articles. Read the type outline to actually have selected the right type.

- If the type does not suit your demands, use the Look for industry on top of the screen to get the one that does.

- When you are satisfied with the shape, validate your decision by simply clicking the Acquire now button. Then, pick the costs prepare you favor and give your references to sign up to have an account.

- Process the deal. Use your credit card or PayPal account to finish the deal.

- Pick the file format and down load the shape on your own product.

- Make changes. Fill up, edit and produce and indicator the saved Rhode Island Approval of Stock Option Plan.

Each format you added to your bank account lacks an expiration particular date and is also your own property for a long time. So, in order to down load or produce yet another backup, just visit the My Forms segment and click in the type you need.

Gain access to the Rhode Island Approval of Stock Option Plan with US Legal Forms, probably the most extensive local library of legal document themes. Use 1000s of professional and status-distinct themes that meet your small business or individual needs and demands.