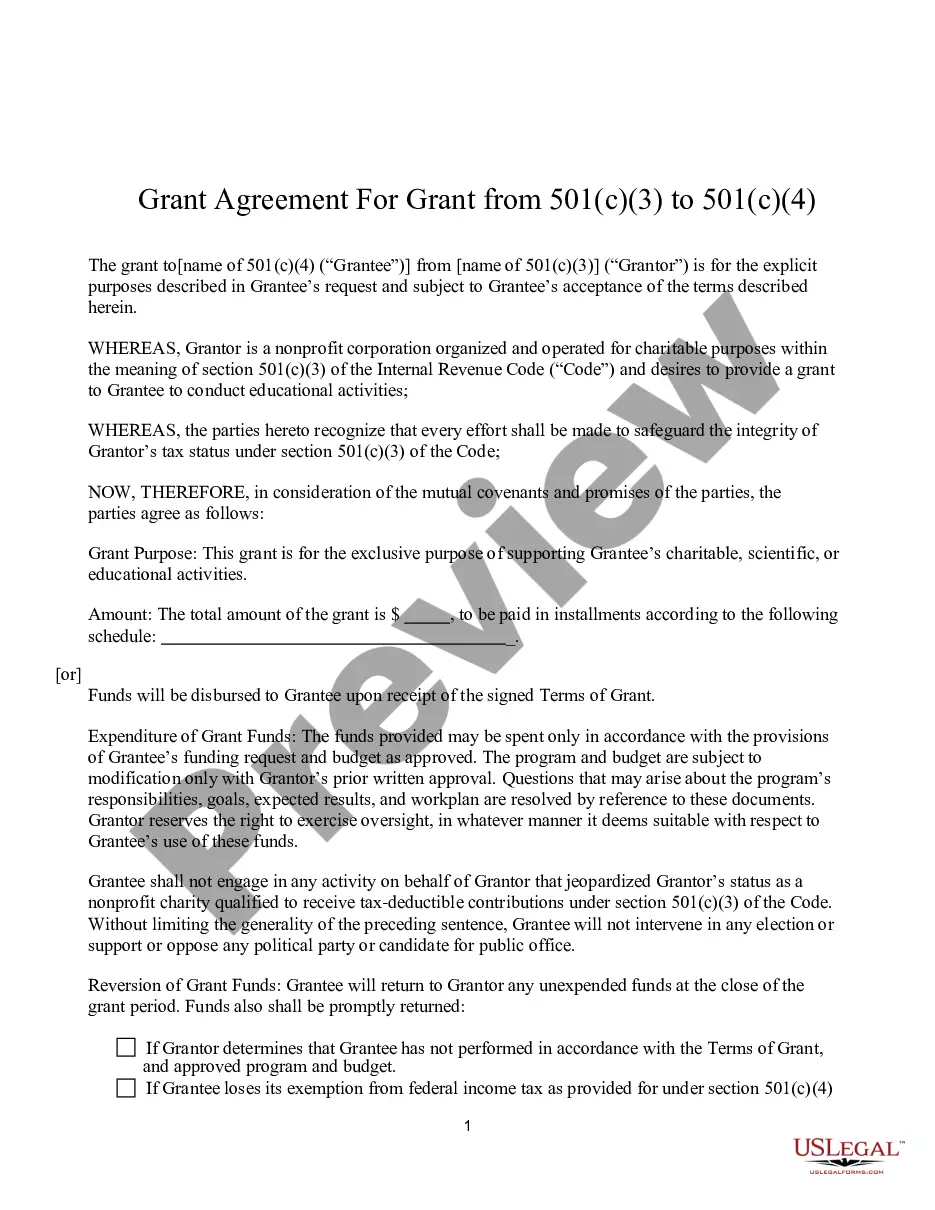

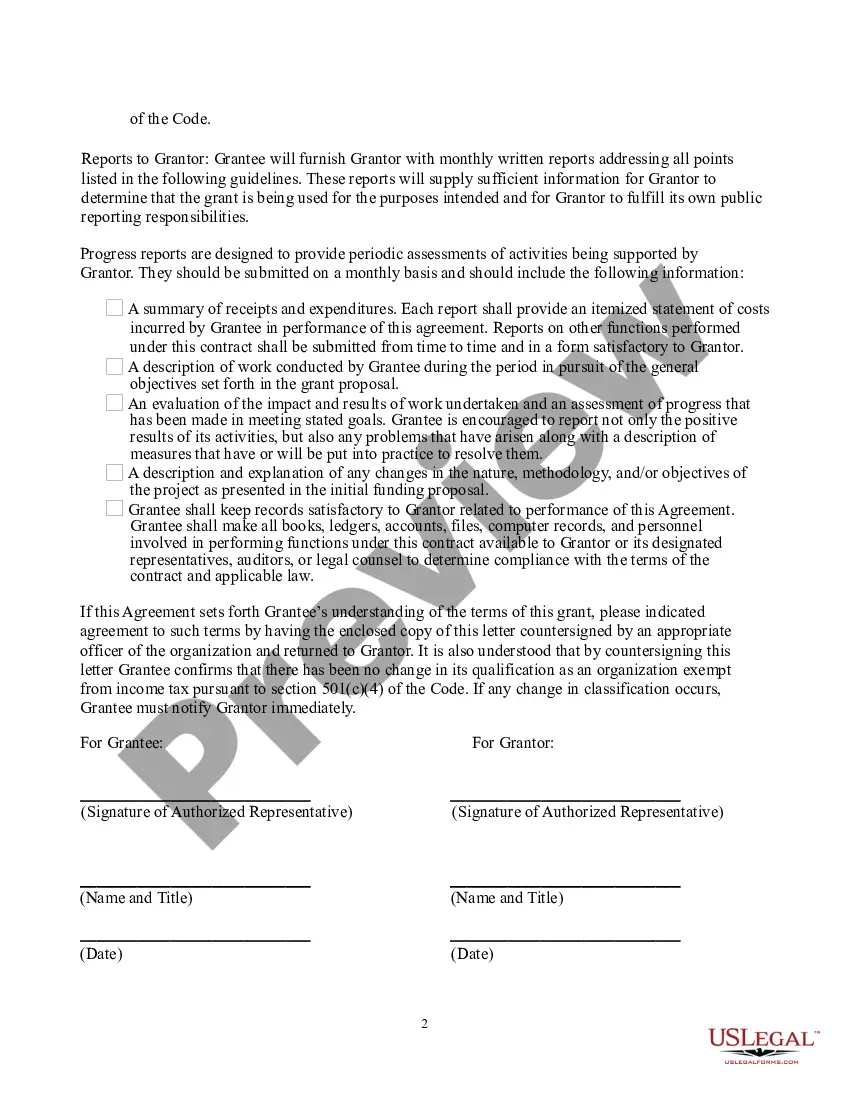

Rhode Island Grant Agreement from 501(c)(3) to 501(c)(4): A Comprehensive Overview Keywords: Rhode Island, Grant Agreement, 501(c)(3), 501(c)(4), non-profit, tax-exempt, transition, rules and regulations, types. Introduction: Rhode Island is home to numerous non-profit organizations that are committed to serving the community through their charitable work. These organizations often obtain tax-exempt status under section 501(c)(3) of the Internal Revenue Code (IRC). However, there may come a time when a 501(c)(3) organization decides to transition to a 501(c)(4) status, which serves different purposes and has different implications under the tax law. This transition typically involves the execution of a Rhode Island Grant Agreement to ensure compliance with state regulations and the seamless transition of the organization's activities. What is a 501(c)(3) organization? A 501(c)(3) organization is a tax-exempt, non-profit entity recognized by the Internal Revenue Service (IRS). This status is typically granted to organizations established for charitable, educational, religious, or scientific purposes. These organizations rely heavily on grants, donations, and contributions to sustain their operations and are subject to specific rules and regulations regarding their activities and spending. Understanding the transition to 501(c)(4): While 501(c)(3) organizations primarily focus on providing charitable services and promoting the public interest, 501(c)(4) organizations engage in social welfare activities. These activities often involve advocacy, lobbying, and political campaigns on behalf of specific causes. The transition from 501(c)(3) to 501(c)(4) allows organizations to broaden their scope of work and actively participate in political and legislative activities that influence public policies. Different types of Rhode Island Grant Agreements from 501(c)(3) to 501(c)(4): 1. Basic Transition Rhode Island Grant Agreement: The Basic Transition Rhode Island Grant Agreement outlines the key terms and conditions required for the conversion of a 501(c)(3) organization to a 501(c)(4) status. It typically includes clauses specifying the effective date of the transition, the obligations and commitments of the organization during and after the transition, and any necessary amendments to the organization's bylaws and articles of incorporation. 2. Reporting and Disclosure Rhode Island Grant Agreement: To ensure transparency and compliance with Rhode Island state regulations, the Reporting and Disclosure Rhode Island Grant Agreement outlines specific reporting and disclosure requirements that organizations must meet during and after the transition. This agreement aids in maintaining clear communication between the organization and the state, preventing any misunderstandings or violations. 3. Tax Implications Rhode Island Grant Agreement: The Tax Implications Rhode Island Grant Agreement highlights the tax-related consequences of transitioning from a 501(c)(3) to a 501(c)(4) organization. It covers topics such as the impact on existing tax-exempt status, changes in tax filings and reporting requirements, and potential effects on donor contributions and reducibility. This agreement ensures that the organization fully understands the financial implications and obligations associated with the transition. Conclusion: Transitioning from a 501(c)(3) to a 501(c)(4) organization in Rhode Island requires careful consideration and adherence to state regulations. The Rhode Island Grant Agreement serves as a crucial document to facilitate this transition, covering various aspects such as legal obligations, reporting requirements, and tax considerations. Consulting legal and tax professionals experienced in non-profit law is highly recommended navigating this complex process effectively.

Rhode Island Grant Agreement from 501(c)(3) to 501(c)(4)

Description

How to fill out Rhode Island Grant Agreement From 501(c)(3) To 501(c)(4)?

Are you presently in the position where you need to have documents for either organization or personal reasons virtually every time? There are a lot of authorized record layouts available on the Internet, but locating kinds you can trust is not effortless. US Legal Forms offers a large number of develop layouts, just like the Rhode Island Grant Agreement from 501(c)(3) to 501(c)(4), which can be written to fulfill state and federal demands.

Should you be previously informed about US Legal Forms website and possess a merchant account, basically log in. After that, you can down load the Rhode Island Grant Agreement from 501(c)(3) to 501(c)(4) design.

Unless you come with an account and would like to start using US Legal Forms, adopt these measures:

- Obtain the develop you will need and ensure it is for the right city/area.

- Make use of the Preview key to check the form.

- Browse the explanation to actually have selected the appropriate develop.

- If the develop is not what you are trying to find, utilize the Research field to obtain the develop that meets your requirements and demands.

- Once you get the right develop, click on Acquire now.

- Pick the rates program you need, complete the necessary information to make your money, and pay for your order utilizing your PayPal or credit card.

- Choose a hassle-free file format and down load your backup.

Find all of the record layouts you may have purchased in the My Forms food selection. You can obtain a extra backup of Rhode Island Grant Agreement from 501(c)(3) to 501(c)(4) any time, if required. Just click on the essential develop to down load or print out the record design.

Use US Legal Forms, the most considerable variety of authorized kinds, to save lots of efforts and avoid blunders. The support offers expertly manufactured authorized record layouts which you can use for a range of reasons. Generate a merchant account on US Legal Forms and commence making your daily life easier.

Form popularity

FAQ

How to Fill Out the Form W-9 for Nonprofits Step 1 ? Write your corporation name. ... Step 2 ? Enter your business name. ... Step 3 ? Know your entity type. ... Step 4 ? Your exempt payee code. ... Step 5 ? Give your street address. ... Step 6 ? Give your city, state, and zip code. ... Step 7 ? List account numbers.

Generally speaking, the purpose of Schedule G is to obtain information about whether a transaction creating a successor organization resulted in benefit to private shareholders or individuals associated with the predecessor organization.

Describe your nonprofit organization and make a case for your credibility. Explain why you can be trusted to steward the funds responsibly. Also share your organization's history, your success record, and why you're the right fit for the project.

Notify the IRS by writing a "statement of nonprofit conversion" that includes the reason for nonprofit termination, a certified copy of a liquidation plan, the fair market value of the organization and a list of all asset recipients if assets will be distributed.

Here are the common steps, in order, that are often included when writing a formal grant proposal: Include a cover letter. ... Include an executive summary. ... Describe a statement of need. ... List objectives and goals. ... Describe methods and strategies. ... Detail a plan of evaluation. ... Include a budget. ... Detail organizational information.

Key takeaways Understand the grant requirements. From the funding organization's goals to application deadlines ? it is essential to understand the grant requirements and guidelines thoroughly. Develop a compelling narrative. ... Demonstrate impact. ... Provide a detailed budget. ... Include supporting materials. ... Follow-up.

Grant writing tends to be hard because it is intricate and has a number of components to learn. If you come to grant writing with strong writing skills, knowledge of the grant writing process broadly, and a basic understanding of what grant funding is, you'll probably be able to learn grant writing quickly.

If you plan to write a grant proposal, you should familiarize yourself with the following parts: Introduction/Abstract/Executive Summary. ... Organizational Background. ... Problem Statement/Needs Assessment. ... Program Goals and Objectives. ... Methods and Activities. ... Evaluation Plan. ... Budget/Sustainability.