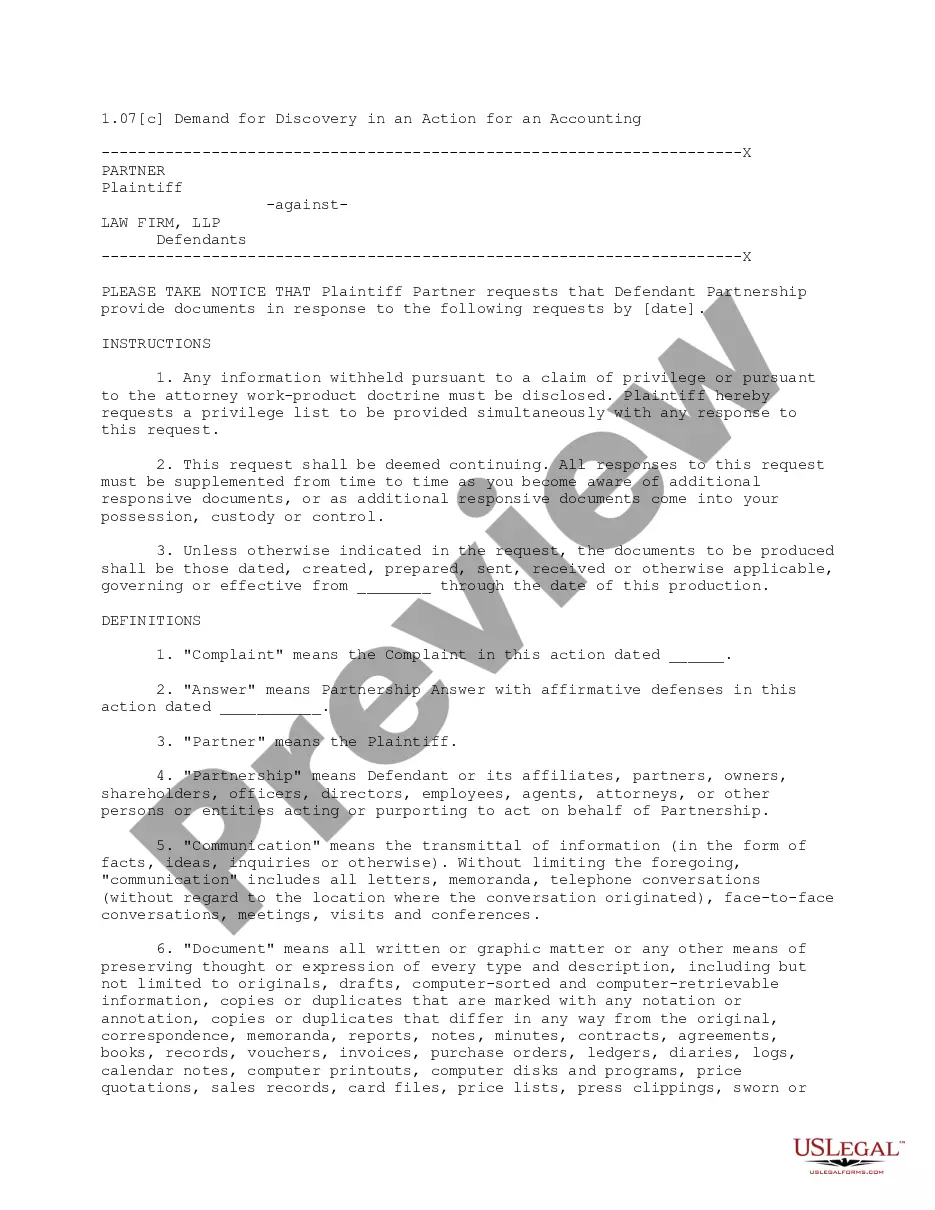

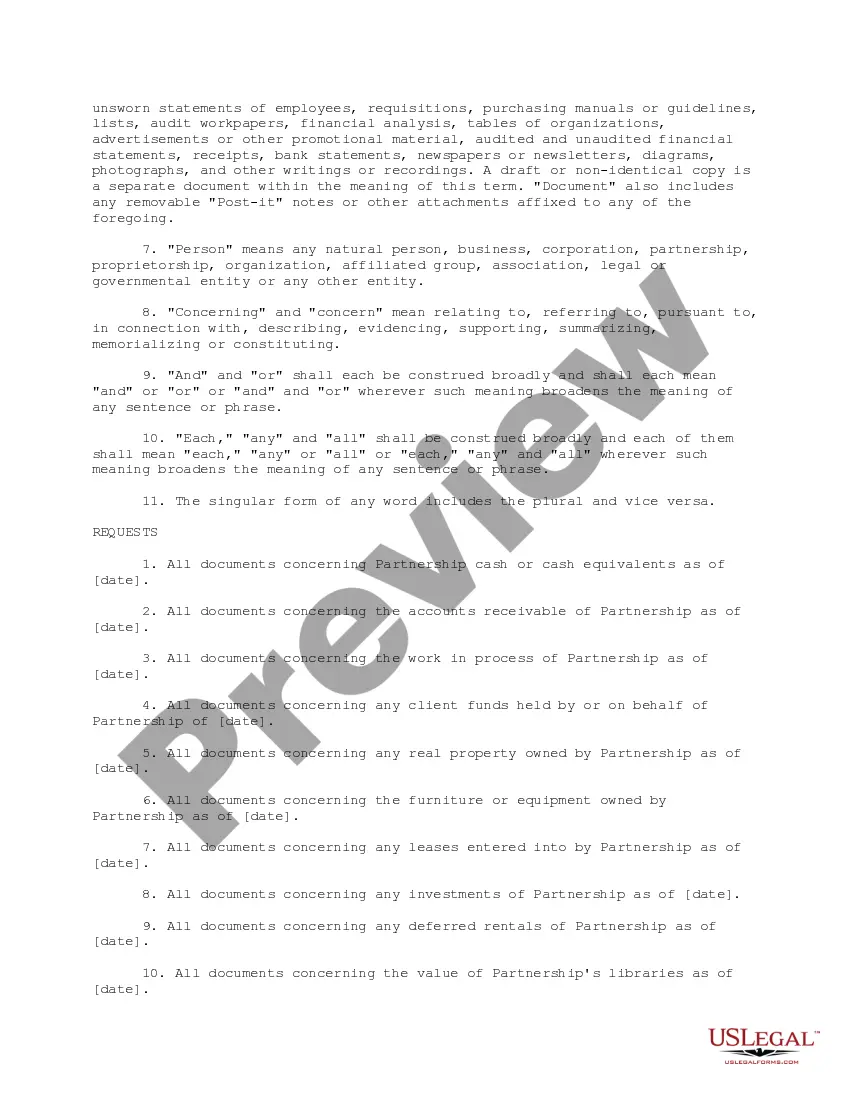

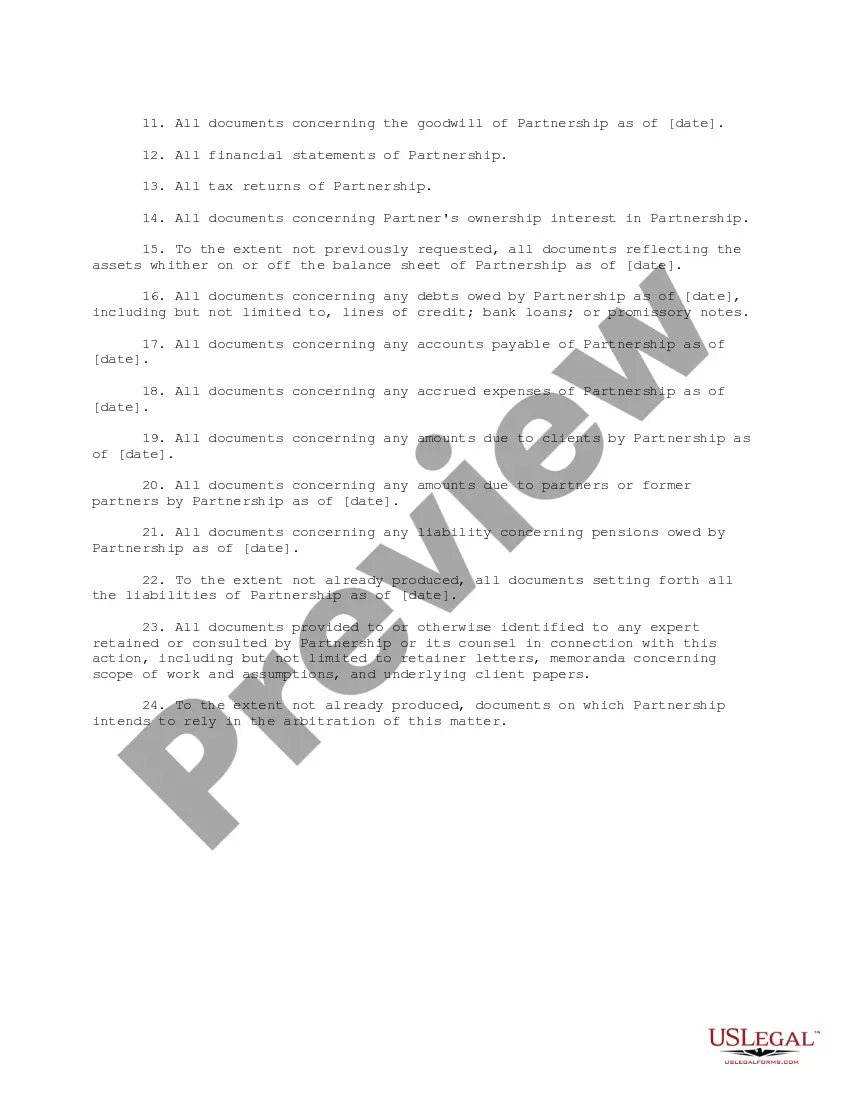

This document is the plaintiff's demand for discovery in a lawsuit filed by a former partner seeking an accounting of his former firm, when the partnership agreement did not provide for an accounting. It contains a request for production of documents.

Rhode Island Demand for Discovery in an Action for an Accounting is a legal process employed to obtain relevant information and evidence in a lawsuit that involves accounting matters. This demand aims to empower the requesting party with necessary documents and data to analyze and assess financial transactions, records, and operations. In Rhode Island, there are generally two types of demands for discovery in actions for an accounting: 1. Interrogatories: This type of discovery involves written questions that are sent to the opposing party, requiring them to provide detailed and specific answers under oath. These interrogatories focus on accounting-related matters, such as income, expenses, assets, liabilities, financial statements, and other relevant financial data related to the case. 2. Document Requests: Parties can also make demands for specific documents related to the accounting aspect of the case. These requests typically include financial records, bank statements, tax returns, invoices, contracts, ledgers, and any other relevant documents that can shed light on the financial transactions and activities at the heart of the dispute. In an action for an accounting, it is crucial to include relevant keywords to ensure effective discovery. Here are some essential keywords: 1. Accounting: Refers to the process of recording, summarizing, analyzing, and interpreting financial transactions and activities. 2. Demand for Discovery: Expresses the legal requirement for the opposing party to provide requested information and documents. 3. Interrogatories: Specific written questions posed to the opposing party, requiring them to provide sworn answers. 4. Document Requests: Formal demands for the production of relevant documents and records related to the accounting aspects of the case. 5. Financial Transactions: Refers to the monetary exchanges, deals, or activities that impact the financial position of the involved parties. 6. Financial Records: All documents created and maintained by a person or entity, such as receipts, invoices, ledgers, and other evidence of financial transactions. 7. Assets: All items of value owned or controlled by a person or entity, including cash, investments, property, and intellectual property. 8. Liabilities: Financial obligations or debts owed by a person or entity to another party. 9. Income: The money or value received by a person or entity, typically derived from business operations, investments, or other sources. 10. Expenses: The costs incurred by a person or entity during normal business operations, including salaries, rent, utilities, and other overhead costs. In conclusion, Rhode Island Demand for Discovery in an Action for an Accounting involves using interrogatories and document requests to obtain relevant financial information and documents from the opposing party. These demands enable a thorough investigation of the accounting aspects of a legal dispute, ensuring transparency and fairness in the resolution process.Rhode Island Demand for Discovery in an Action for an Accounting is a legal process employed to obtain relevant information and evidence in a lawsuit that involves accounting matters. This demand aims to empower the requesting party with necessary documents and data to analyze and assess financial transactions, records, and operations. In Rhode Island, there are generally two types of demands for discovery in actions for an accounting: 1. Interrogatories: This type of discovery involves written questions that are sent to the opposing party, requiring them to provide detailed and specific answers under oath. These interrogatories focus on accounting-related matters, such as income, expenses, assets, liabilities, financial statements, and other relevant financial data related to the case. 2. Document Requests: Parties can also make demands for specific documents related to the accounting aspect of the case. These requests typically include financial records, bank statements, tax returns, invoices, contracts, ledgers, and any other relevant documents that can shed light on the financial transactions and activities at the heart of the dispute. In an action for an accounting, it is crucial to include relevant keywords to ensure effective discovery. Here are some essential keywords: 1. Accounting: Refers to the process of recording, summarizing, analyzing, and interpreting financial transactions and activities. 2. Demand for Discovery: Expresses the legal requirement for the opposing party to provide requested information and documents. 3. Interrogatories: Specific written questions posed to the opposing party, requiring them to provide sworn answers. 4. Document Requests: Formal demands for the production of relevant documents and records related to the accounting aspects of the case. 5. Financial Transactions: Refers to the monetary exchanges, deals, or activities that impact the financial position of the involved parties. 6. Financial Records: All documents created and maintained by a person or entity, such as receipts, invoices, ledgers, and other evidence of financial transactions. 7. Assets: All items of value owned or controlled by a person or entity, including cash, investments, property, and intellectual property. 8. Liabilities: Financial obligations or debts owed by a person or entity to another party. 9. Income: The money or value received by a person or entity, typically derived from business operations, investments, or other sources. 10. Expenses: The costs incurred by a person or entity during normal business operations, including salaries, rent, utilities, and other overhead costs. In conclusion, Rhode Island Demand for Discovery in an Action for an Accounting involves using interrogatories and document requests to obtain relevant financial information and documents from the opposing party. These demands enable a thorough investigation of the accounting aspects of a legal dispute, ensuring transparency and fairness in the resolution process.