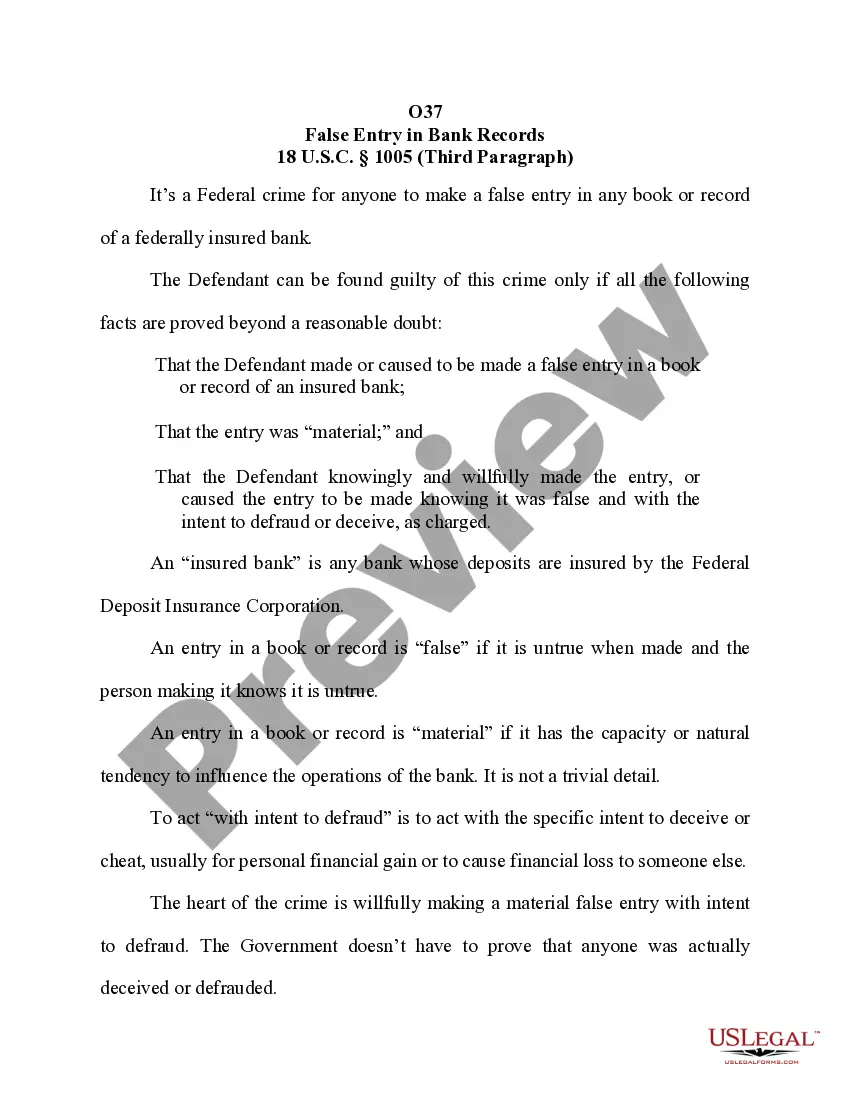

South Carolina False Entry in Financial Records is a form of accounting fraud wherein an individual or entity intentionally misrepresents or omits a transaction or financial statement to hide the truth of their financial situation. South Carolina False Entry in Financial Records typically involves the creation of fictitious entries, the alteration of existing entries, or the omission of relevant information. Types of South Carolina False Entry in Financial Records include: 1. Asset Misappropriation: This type of false entry involves the unauthorized use of an organization's assets for personal gain. Examples include stealing office supplies, embezzling funds, and forging company checks. 2. Fraudulent Financial Reporting: This type of false entry involves the intentional misrepresentation of financial information to make a company appear more profitable than it actually is. Examples include overstating revenue, understating expenses, and overvaluing assets. 3. Misrepresentation of Non-Financial Information: This type of false entry involves the misrepresentation of non-financial information in order to mislead investors and other stakeholders. Examples include falsifying customer orders and providing incorrect information on product warranties. 4. Concealment of Fraudulent Activity: This type of false entry involves the intentional concealing of fraudulent activity in order to evade detection. Examples include using offshore accounts to hide illegal transactions and creating fictitious companies to hide money laundering activities.

South Carolina FALSE ENTRY IN FINANCIAL RECORDS

Description

How to fill out South Carolina FALSE ENTRY IN FINANCIAL RECORDS?

Preparing official paperwork can be a real burden unless you have ready-to-use fillable templates. With the US Legal Forms online library of formal documentation, you can be confident in the blanks you obtain, as all of them correspond with federal and state laws and are verified by our experts. So if you need to prepare South Carolina FALSE ENTRY IN FINANCIAL RECORDS, our service is the best place to download it.

Obtaining your South Carolina FALSE ENTRY IN FINANCIAL RECORDS from our catalog is as easy as ABC. Previously registered users with a valid subscription need only sign in and click the Download button once they find the correct template. Afterwards, if they need to, users can use the same document from the My Forms tab of their profile. However, even if you are new to our service, signing up with a valid subscription will take only a few minutes. Here’s a quick guideline for you:

- Document compliance verification. You should carefully review the content of the form you want and check whether it satisfies your needs and complies with your state law regulations. Previewing your document and reviewing its general description will help you do just that.

- Alternative search (optional). If you find any inconsistencies, browse the library using the Search tab on the top of the page until you find an appropriate template, and click Buy Now when you see the one you need.

- Account creation and form purchase. Create an account with US Legal Forms. After account verification, log in and choose your most suitable subscription plan. Make a payment to continue (PayPal and credit card options are available).

- Template download and further usage. Select the file format for your South Carolina FALSE ENTRY IN FINANCIAL RECORDS and click Download to save it on your device. Print it to fill out your papers manually, or use a multi-featured online editor to prepare an electronic version faster and more effectively.

Haven’t you tried US Legal Forms yet? Subscribe to our service today to obtain any formal document quickly and easily any time you need to, and keep your paperwork in order!

Form popularity

FAQ

SECTION 39-5-20. Unfair methods of competition and unfair or deceptive acts or practices unlawful; application of federal act. (a) Unfair methods of competition and unfair or deceptive acts or practices in the conduct of any trade or commerce are hereby declared unlawful.

To criminally prosecute a bad check, South Carolina law states a check must be deposited within 10 days of receipt, the check cannot be postdated, that there was no agreement to hold the check, and a warrant must be obtained within 180 days from the date the check was received.

As laid out in South Carolina General Code Section 16-13-240, it is a crime to obtain a signature, money, or property from someone under false pretenses or misrepresentation of a fact with ?intent to cheat and defraud a person of that property.? Simply put, if you obtain money, property, or the title to property from

CHAPTER 11 - BANK DEPOSITS. SECTION 34-11-80. Stopping payment on check, draft or order with intent to defraud.

Terms Used In South Carolina Code 34-3-110 Corporation: A legal entity owned by the holders of shares of stock that have been issued, and that can own, receive, and transfer property, and carry on business in its own name. Mortgage: The written agreement pledging property to a creditor as collateral for a loan.

(a) It is unlawful for a person, with intent to defraud, in his own name or in any other capacity, to draw, make, utter, issue, or deliver to another a check, draft, or other written order on a bank or depository for the payment of money or its equivalent, whether given to pay rent, make a payment on a lease, obtain

A person who violates the provisions of this chapter, upon conviction, must be punished as follows: If the amount of the instrument is one thousand dollars or less, it must be tried exclusively in a magistrates court.

(A)(1) It is unlawful for a person to wilfully give false, misleading, or incomplete testimony under oath in any court of record, judicial, administrative, or regulatory proceeding in this State.