South Carolina Demand for Collateral by Creditor

Description

How to fill out Demand For Collateral By Creditor?

Are you in a situation where you often require documents for either business or personal purposes? There are numerous legal document templates accessible online, but finding reliable ones can be challenging.

US Legal Forms offers thousands of template options, like the South Carolina Demand for Collateral by Creditor, designed to meet both federal and state regulations.

If you are already familiar with the US Legal Forms website and possess an account, simply Log In. After that, you can download the South Carolina Demand for Collateral by Creditor template.

You can find all the document templates you have purchased in the My documents menu. You can acquire another copy of the South Carolina Demand for Collateral by Creditor at any time, if needed. Just select the required template to download or print the document.

Utilize US Legal Forms, the largest collection of legal templates, to save time and avoid errors. The service offers professionally crafted legal document templates that can be used for a variety of purposes. Create an account on US Legal Forms and start simplifying your life.

- Locate the template you need and confirm it is for your specific state/region.

- Utilize the Review button to inspect the template.

- Check the details to ensure that you have chosen the correct document.

- If the template does not meet your requirements, use the Search area to find one that does.

- Upon finding the suitable template, click Buy now.

- Select the pricing plan you prefer, complete the necessary information to create your account, and pay for your order using PayPal or a credit card.

- Choose a convenient file format and download your copy.

Form popularity

FAQ

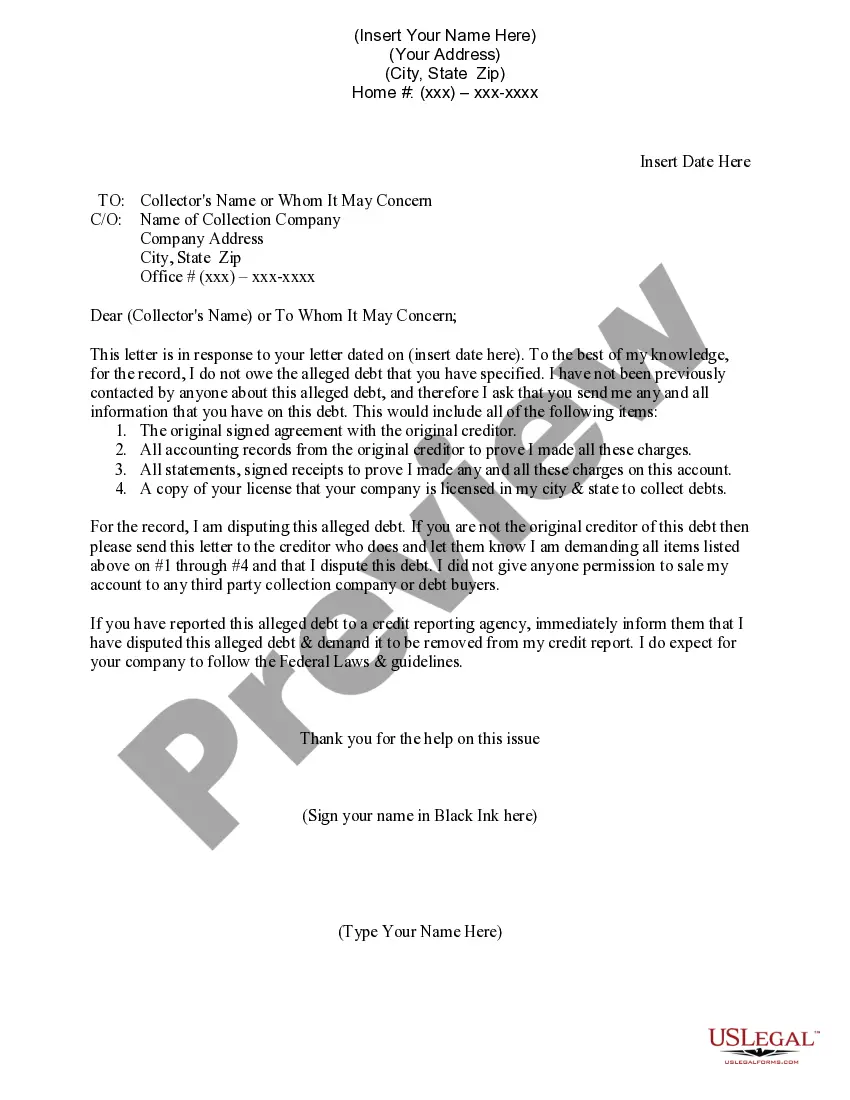

South Carolina state law governs debt collection practices, primarily through the Fair Debt Collection Practices Act. This law protects consumers from abusive practices by debt collectors, including misleading information and harassment. Understanding these laws, especially the specifics related to the South Carolina Demand for Collateral by Creditor, can empower you and safeguard your rights.

Yes, a creditor can demand payment for a debt, even if some time has passed. They may contact you to request payment or discuss your outstanding balance. It's essential to know your rights and what options you have if you receive such a demand. Familiarizing yourself with the terms associated with the South Carolina Demand for Collateral by Creditor can aid in this process.

Yes, a debt collector can attempt to collect on an old debt; however, this depends on the age of the debt and whether it falls within the statute of limitations. In South Carolina, if the debt is older than three years, a collector cannot pursue legal action against you. Staying informed about the rules, including the South Carolina Demand for Collateral by Creditor, can help you respond appropriately to collectors.

In South Carolina, a debt collector cannot legally collect on a 10-year-old debt if it has passed the statute of limitations of three years. Once this time frame has lapsed, you have legal protection against collection efforts through the courts. However, the collector might still contact you regarding the debt. It is wise to understand how the South Carolina Demand for Collateral by Creditor affects your situation.

A debt collector can legally pursue old debt in South Carolina for up to three years, based on the statute of limitations. After this period, the collector can no longer file a lawsuit to collect the debt. However, they may still contact you to request payment. Knowing the rules around the South Carolina Demand for Collateral by Creditor will help you navigate these communications.

In South Carolina, a debt becomes uncollectible after three years due to the statute of limitations. This means that creditors cannot take legal action to collect the debt after this period. However, keep in mind that the creditor may still attempt to contact you regarding the debt. Understanding your rights in relation to the South Carolina Demand for Collateral by Creditor can help you make informed decisions.

Several states are known to be debtor-friendly, providing protections that can help individuals manage debts more easily. States like Florida and Texas have laws that offer significant exemptions and shield certain assets from creditors. If you are dealing with a South Carolina Demand for Collateral by Creditor, knowing the protections available in different states can enhance your strategy. Exploring solutions through platforms like uslegalforms can empower you with necessary information.

South Carolina is not a non-garnishment state; creditors can seek wage garnishment under certain conditions. However, there are specific regulations and limits regarding how much can be garnished. Understanding these laws can be crucial, especially during a South Carolina Demand for Collateral by Creditor. Consulting with a legal expert can guide you through the processes involved.

South Carolina is often considered a business-friendly state due to its favorable tax environment and regulatory framework. Many businesses thrive here because of the supportive local government and various incentives. When managing debts, businesses may encounter situations involving a South Carolina Demand for Collateral by Creditor. Utilizing resources like uslegalforms can provide clarity on legal obligations.

The UCC 1 in South Carolina is a legal form that creditors use to file a financing statement, thus perfecting their security interest. This filing notifies others about the creditor's claim to certain collateral. If there's a South Carolina Demand for Collateral by Creditor, this form plays a key role in establishing rights. Understanding its importance can help protect your assets effectively.