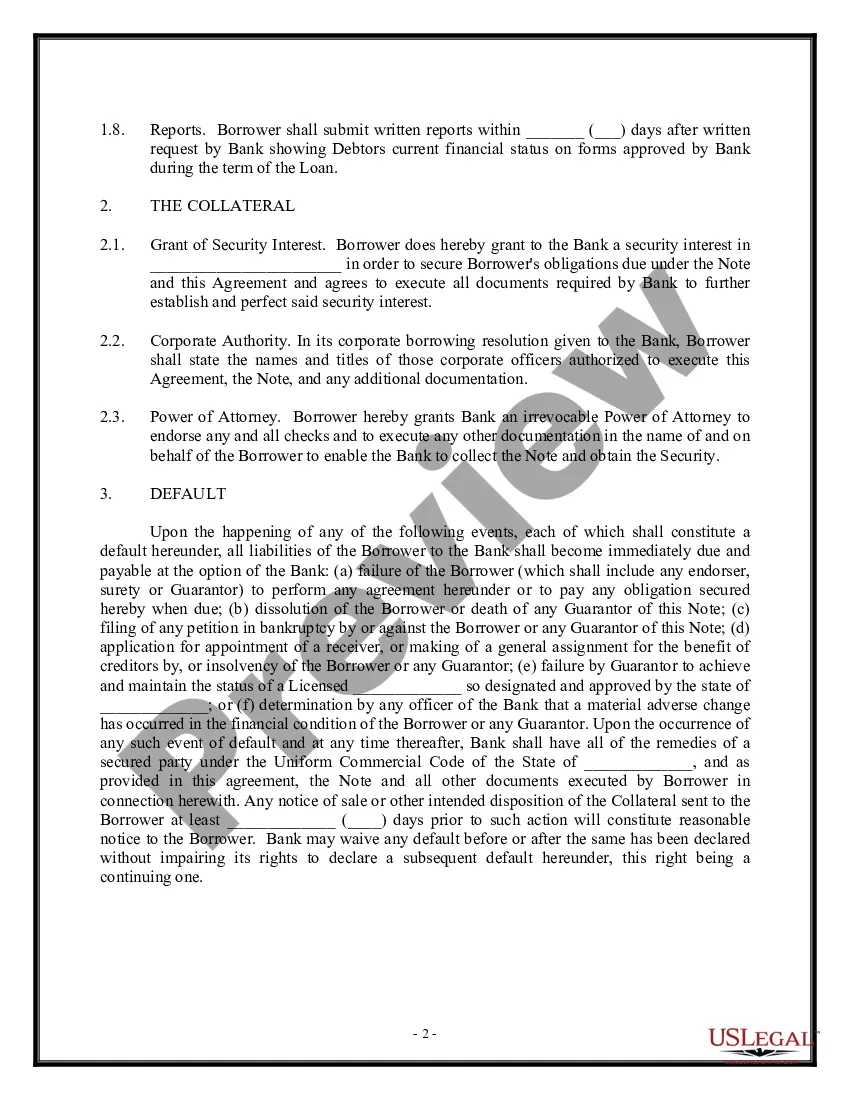

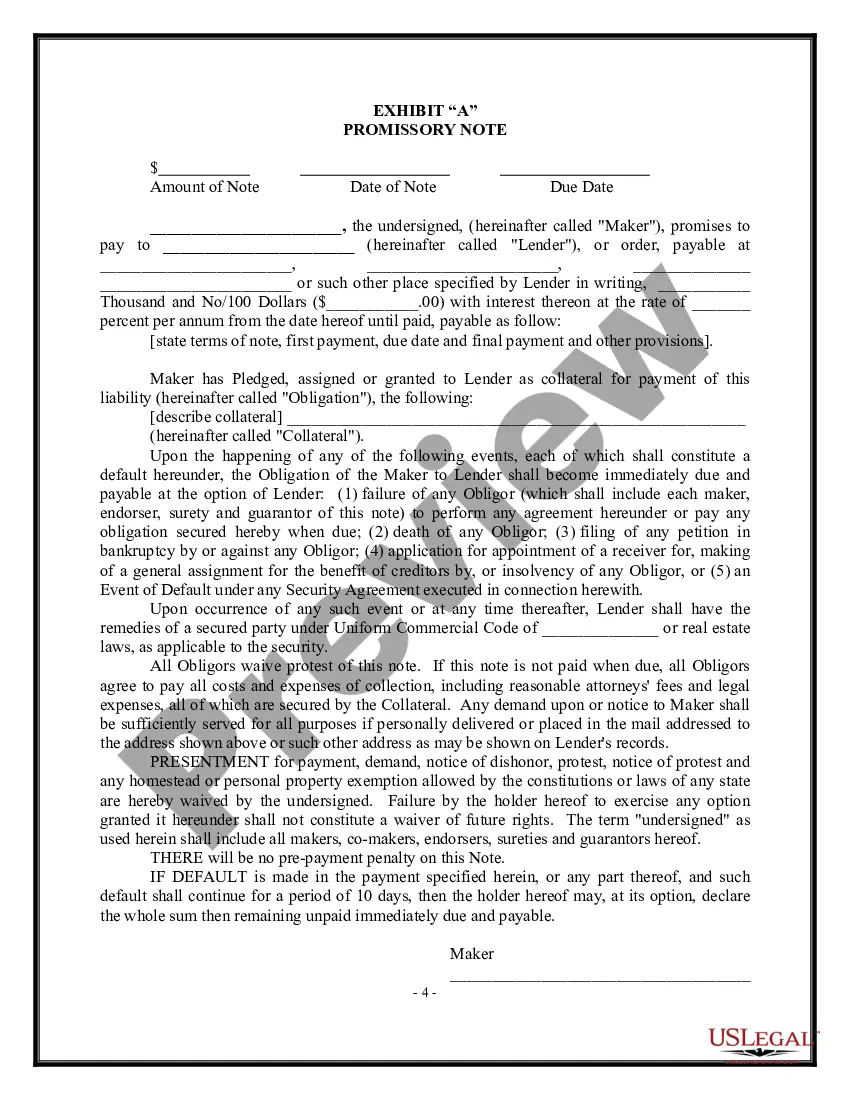

A South Carolina Loan Agreement — Short Form is a legal document that outlines the terms and conditions of a loan between two parties in the state of South Carolina. This agreement serves as a legally binding contract that protects both the lender and the borrower and ensures that all terms of the loan are clearly defined and agreed upon. The South Carolina Loan Agreement — Short Form is designed to be concise and straightforward, making it easy for both parties to understand and navigate. It typically includes key information such as the names and addresses of the lender and borrower, the loan amount, the interest rate, and the repayment terms. This agreement may also include provisions on late payments, penalties for default, and any additional fees or charges associated with the loan. One type of South Carolina Loan Agreement — Short Form is a personal loan agreement. This agreement is commonly used when an individual lends money to another individual, such as a friend or family member. It allows both parties to establish clear terms for repayment, ensuring that expectations are understood and met. Another type of South Carolina Loan Agreement — Short Form is a business loan agreement. This agreement is used when a business or organization seeks financing from another party, such as a bank or investor. It outlines the loan terms, including the repayment schedule, interest rate, and any collateral or guarantees required. A South Carolina Loan Agreement — Short Form can also be used for other types of loans, such as auto loans, student loans, or mortgage loans. Each of these agreements will have specific provisions and terms relevant to the nature of the loan. In conclusion, a South Carolina Loan Agreement — Short Form is a vital legal document used to establish the terms and conditions of a loan in the state of South Carolina. It ensures that both parties are protected and provides clear guidelines for repayment. Whether it is a personal loan, business loan, auto loan, student loan, or mortgage loan, having a well-drafted loan agreement is essential for all parties involved.

South Carolina Loan Agreement - Short Form

Description

How to fill out South Carolina Loan Agreement - Short Form?

It is possible to invest time on-line attempting to find the legitimate papers format which fits the federal and state requirements you require. US Legal Forms offers a huge number of legitimate types which can be analyzed by specialists. It is simple to acquire or print out the South Carolina Loan Agreement - Short Form from the services.

If you have a US Legal Forms accounts, you are able to log in and then click the Acquire button. Next, you are able to total, change, print out, or indication the South Carolina Loan Agreement - Short Form. Every legitimate papers format you acquire is your own forever. To obtain yet another version associated with a acquired develop, go to the My Forms tab and then click the corresponding button.

Should you use the US Legal Forms website initially, follow the easy guidelines beneath:

- Initial, make certain you have chosen the correct papers format for the area/city of your choice. Browse the develop description to make sure you have selected the right develop. If accessible, make use of the Preview button to search from the papers format too.

- If you would like discover yet another version of the develop, make use of the Lookup discipline to get the format that suits you and requirements.

- After you have discovered the format you would like, just click Acquire now to proceed.

- Pick the rates program you would like, enter your accreditations, and register for a free account on US Legal Forms.

- Complete the financial transaction. You may use your Visa or Mastercard or PayPal accounts to purchase the legitimate develop.

- Pick the file format of the papers and acquire it in your system.

- Make adjustments in your papers if needed. It is possible to total, change and indication and print out South Carolina Loan Agreement - Short Form.

Acquire and print out a huge number of papers web templates using the US Legal Forms website, that offers the greatest assortment of legitimate types. Use skilled and status-specific web templates to take on your company or person requirements.