- passing of title;

- made with the intent to pass title;

- without receiving money or value in consideration for the passing of title.

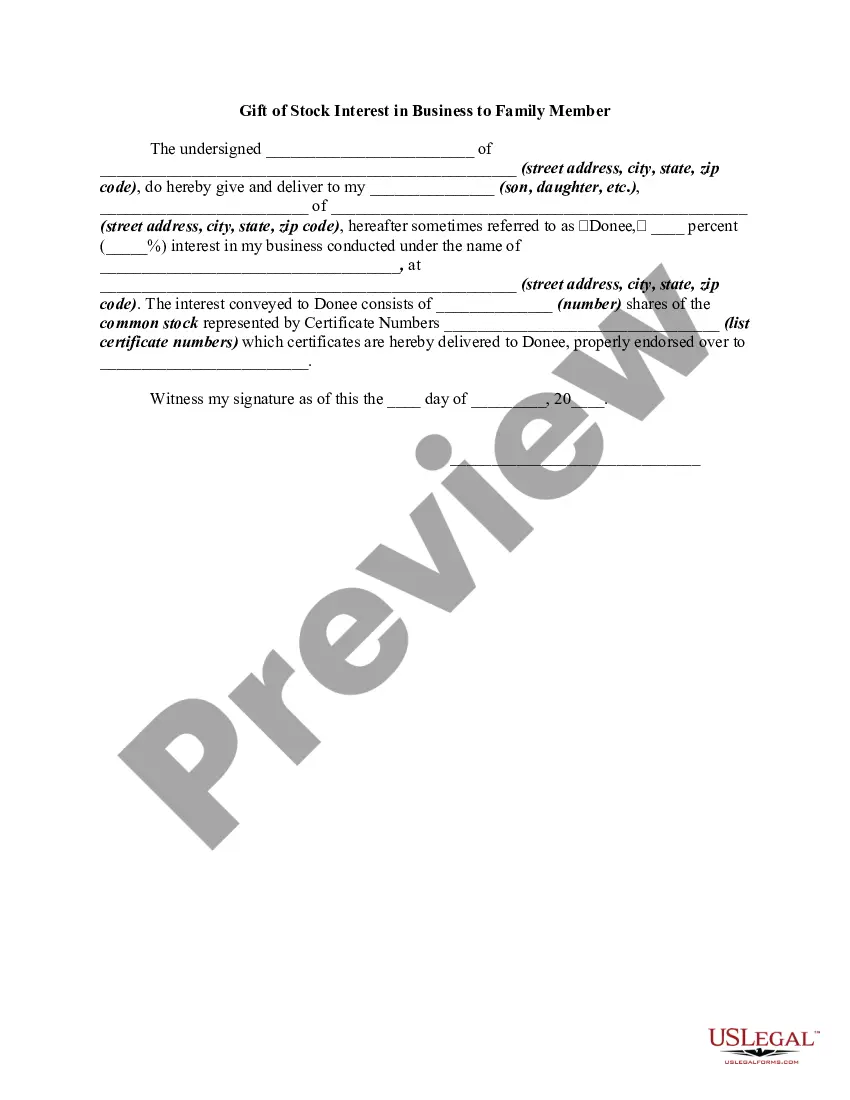

The South Carolina Gift of Stock Interest in Business to Family Member refers to the process of transferring ownership and control of a business to a family member through the exchange of stocks or shares as a gift. This transaction allows the current business owner to transfer assets while retaining ownership of the company. The main purpose of this gift is to ensure a smooth transition of ownership, typically within a family, without the need for a sale or extensive legal procedures. It enables the business owner to pass on their business interests to a family member while minimizing taxes and potential conflicts. There are several types of South Carolina Gift of Stock Interest in Business to Family Member: 1. South Carolina Gift of Minority Interest in Business: This type of gift involves transferring a minority stake in the business, typically less than 50% of the total ownership. The donor retains control and majority ownership while passing on some ownership rights and potential benefits to the family member. 2. South Carolina Gift of Majority Interest in Business: In this case, the business owner transfers a majority stake, more than 50% ownership, to a family member. The recipient gains control over the business, making critical decisions and enjoying the associated benefits. 3. South Carolina Gift of Controlling Interest in Business: This type of gift involves transferring a controlling interest of 50% or more in the business to a family member. The recipient acquires the power to make critical decisions, control voting rights, and potentially manage the day-to-day operations of the business. When executing a South Carolina Gift of Stock Interest in Business to a Family Member, it is crucial to consult with a qualified attorney or financial advisor well-versed in the legal and tax implications. The Internal Revenue Service (IRS) has specific regulations and restrictions regarding gifting stocks and shares, including the need to comply with relevant gift tax rules. Overall, a South Carolina Gift of Stock Interest in Business to a Family Member provides a structured and tax-efficient means for business owners to pass on ownership to their chosen family members while protecting their legacy and ensuring the continuity of the business.