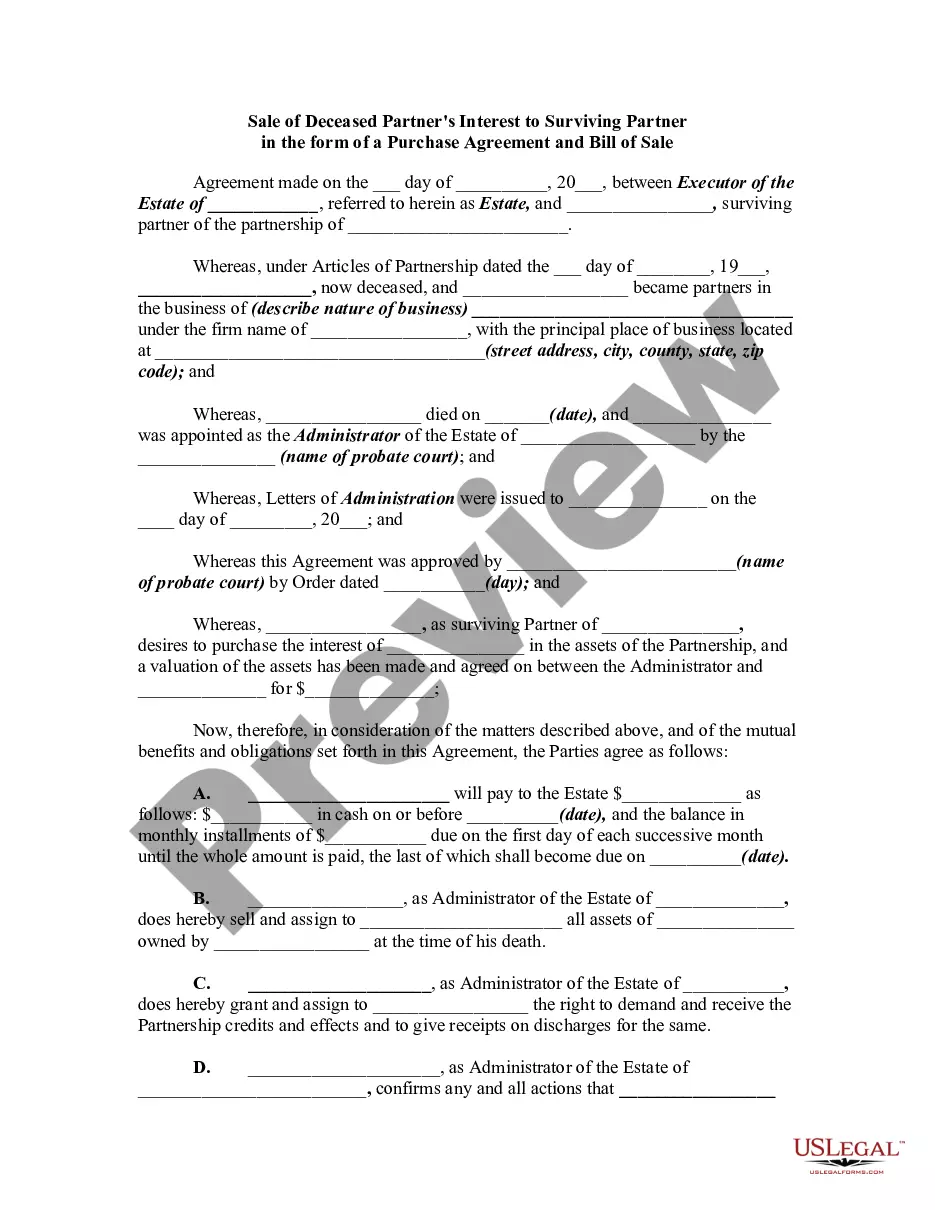

In South Carolina, when a partner in a business passes away, it is important to address the transfer of their interest to the surviving partner through a formal Sale of Deceased Partner's Interest to Surviving Partner. This transaction is typically documented through a Purchase Agreement and a Bill of Sale, providing legal clarity and ensuring a smooth transition. Let's explore the various aspects involved in this process: 1. What is a Purchase Agreement and Bill of Sale? A Purchase Agreement and Bill of Sale are legal documents used to formalize the sale of a deceased partner's interest in a business to the surviving partner. These documents outline the terms and conditions of the sale, ensuring the transfer is properly executed. 2. Key Elements to Include in the Purchase Agreement and Bill of Sale: a. Identifying Information: The agreement should include the legal names and addresses of both the deceased partner's estate and the surviving partner. b. Partnership Details: Specify the details of the partnership, such as the partnership name, type, and the date the partnership was established. c. Deceased Partner's Assets: Provide a comprehensive list of assets that were part of the deceased partner's interest, including equipment, property, intellectual property, or any other relevant business assets. d. Purchase Price: Clearly state the agreed purchase price for the deceased partner's interest, along with the method of payment. e. Terms and Conditions: Define any special conditions, warranties, or representations associated with the purchase, including any applicable non-compete clauses, indemnification clauses, or dispute resolution provisions. f. Responsibilities and Liabilities: Clearly outline the specific responsibilities and liabilities transferred to the surviving partner, as well as any remaining liabilities that will be retained by the deceased partner's estate. g. Signatures and Notarization: Both parties should sign the agreement, and it should be notarized to ensure its validity. 3. Types of South Carolina Sale of Deceased Partner's Interest to Surviving Partner: a. Voluntary Sale: This type occurs if the surviving partner and the deceased partner's estate come to a mutual agreement for the transfer of the deceased partner's interest. b. Forced Sale: This type of sale might occur if the partnership agreement stipulates that the surviving partner has the right or obligation to purchase the deceased partner's interest upon their death, overriding the wishes of the estate. 4. Importance of Legal Assistance: Given the complexities involved in drafting a comprehensive Purchase Agreement and Bill of Sale, it is highly recommended consulting with an experienced attorney who specializes in business and partnership law. They will provide invaluable guidance, ensuring that the agreement complies with South Carolina state laws and protects the rights and interests of both parties. Remember, each situation may require unique considerations and additional provisions. Therefore, seeking professional legal advice tailored explicitly to your circumstances is crucial.

South Carolina Sale of Deceased Partner's Interest to Surviving Partner in the form of a Purchase Agreement and Bill of Sale

Description

How to fill out South Carolina Sale Of Deceased Partner's Interest To Surviving Partner In The Form Of A Purchase Agreement And Bill Of Sale?

Finding the right legitimate papers web template can be a have a problem. Naturally, there are tons of templates available on the Internet, but how will you obtain the legitimate kind you need? Take advantage of the US Legal Forms internet site. The services provides thousands of templates, such as the South Carolina Sale of Deceased Partner's Interest to Surviving Partner in the form of a Purchase Agreement and Bill of Sale, that can be used for organization and private requirements. Each of the types are inspected by experts and fulfill state and federal requirements.

When you are already listed, log in in your account and then click the Obtain option to have the South Carolina Sale of Deceased Partner's Interest to Surviving Partner in the form of a Purchase Agreement and Bill of Sale. Use your account to appear throughout the legitimate types you have bought in the past. Visit the My Forms tab of your respective account and have another copy of the papers you need.

When you are a new consumer of US Legal Forms, listed here are simple guidelines so that you can adhere to:

- Initial, ensure you have selected the proper kind for your city/state. You may look over the shape using the Review option and look at the shape outline to ensure this is basically the right one for you.

- In case the kind will not fulfill your requirements, utilize the Seach discipline to discover the appropriate kind.

- When you are certain the shape is suitable, click on the Purchase now option to have the kind.

- Select the costs plan you want and enter in the essential information and facts. Create your account and pay money for an order using your PayPal account or Visa or Mastercard.

- Choose the document structure and down load the legitimate papers web template in your product.

- Comprehensive, revise and produce and sign the acquired South Carolina Sale of Deceased Partner's Interest to Surviving Partner in the form of a Purchase Agreement and Bill of Sale.

US Legal Forms will be the largest collection of legitimate types in which you can see different papers templates. Take advantage of the service to down load professionally-made files that adhere to express requirements.

Form popularity

FAQ

Filing Will and Probatings - The South Carolina ( SC ) Probate Code of Laws requires that the Last Will and Testament be delivered to the Probate Court within 30 days of the decedent's death.

?Heirs' property is land owned ?in common? (known as tenants in common) by all of the heirs, regardless of whether they live on the land; pay the taxes or have never set foot on the land.

If you die survived by a spouse and children, your spouse gets 50% of your estate and your children get and divide 50% of your estate in equal shares. If you are unmarried and are survived by children, your children receive and divide 100% of your estate.

If you have a spouse and no children, your spouse will inherit your entire estate. If you have a spouse and children, your spouse gets half and the remaining estate is split equally amongst the children. If you have no spouse or children, your parents would receive your estate.

South Carolina does not recognize transfer-on-death (TOD) deeds.

If you leave a spouse and no children, your spouse takes all. If you leave no spouse, but children, then your children take your property. Generally, if a child of yours does not survive you their children take the share your child would have taken if they had survived you.

South Carolina Code §62-2-803 states that anyone who ?feloniously and intentionally kills the decedent? is not entitled to any benefits under the decedent's estate, whether the killer is named in the victim's Will or would be an heir to the estate if no Will existed.

Creditors must ?present? claims arising before the decedent's death within the earlier of one year after the decedent's death or eight months after the date of the first publication of the notice to creditors. S.C. Code Ann. § 62?3?803.