In real estate, a short sale occurs when a bank or mortgage lender agrees to discount a loan balance due to an economic hardship on the part of the mortgagor (i.e., the seller). Circumstances determine whether or not banks will discount a loan balance. These circumstances are usually related to the current real estate market climate and the individual borrower's financial situation. A short sale typically is executed to prevent a home foreclosure. Often a bank will choose to allow a short sale if they believe that it will result in a smaller financial loss than foreclosing.

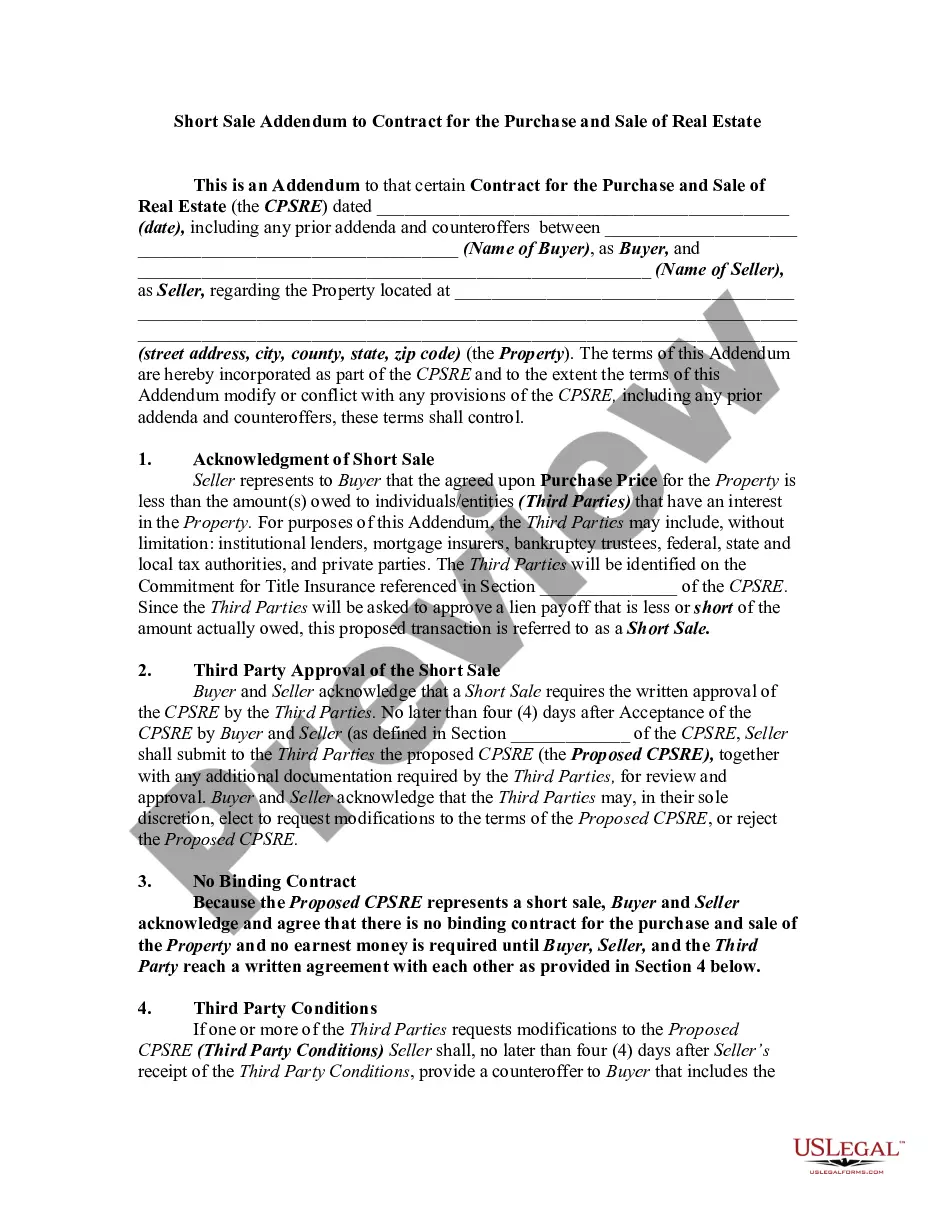

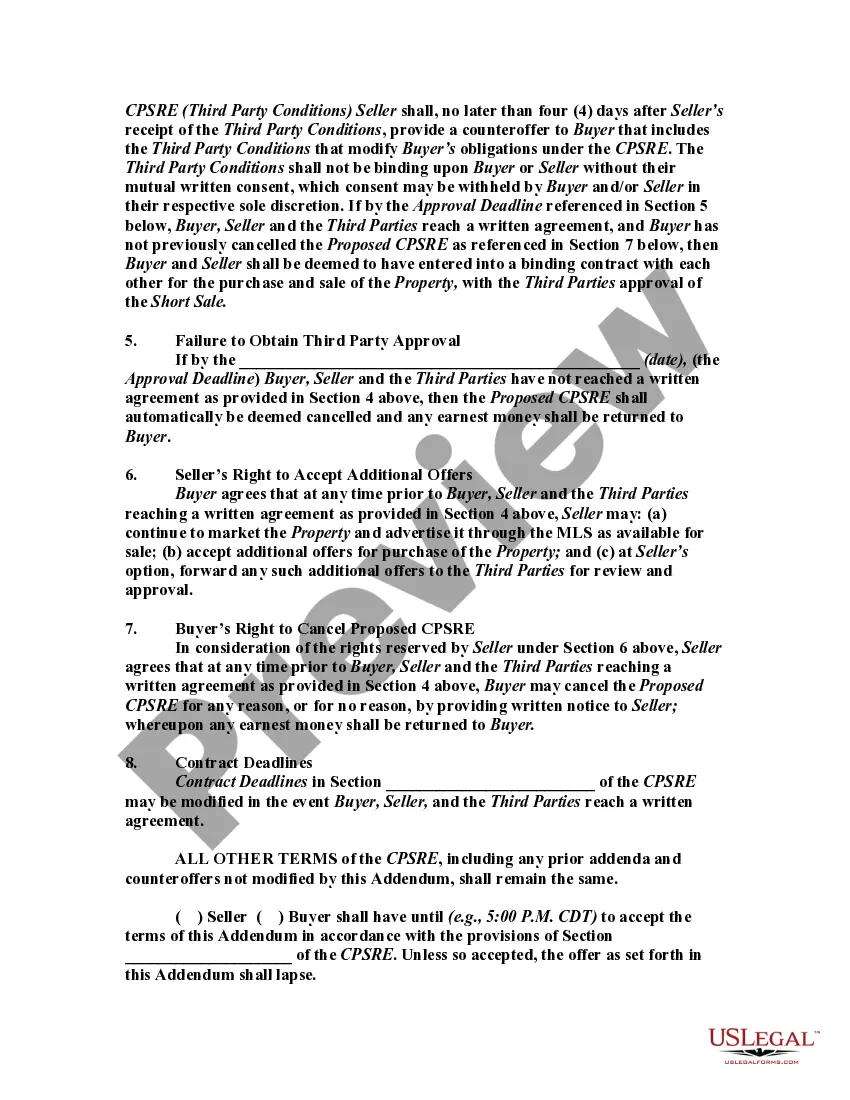

This form is a sample of an Addendum to a standard real estate sales contract in order to incorporate the short sales provisions. This form is a generic example that may be referred to when preparing such a form for your particular state. It is for illustrative purposes only. Local laws should be consulted to determine any specific requirements for such a form in a particular jurisdiction.

The South Carolina Short Sale Addendum to Contract for the Price, Purchase and Sale of Real Estate is a crucial document that specifies the terms and conditions associated with a short sale transaction in South Carolina. This addendum is used when a property owner is facing financial distress and is unable to pay off their mortgage. It allows them to sell the property for less than the outstanding loan amount, with the approval of the lender. There are various types of South Carolina Short Sale Addendums available, tailored to specific scenarios and considerations. Some common types include: 1. Traditional Short Sale Addendum: This addendum is used for a typical short sale scenario where the property owner is in financial hardship and the lender agrees to accept less than the full loan amount as payment. 2. FHA Short Sale Addendum: This addendum is specific to properties financed by the Federal Housing Administration (FHA). It incorporates additional requirements and guidelines mandated by the FHA for short sales. 3. VA Short Sale Addendum: Designed for properties with mortgages guaranteed by the Department of Veterans Affairs (VA), this addendum includes provisions unique to VA loans and outlines specific procedures for obtaining the VA's approval for a short sale. 4. Conventional Short Sale Addendum: This addendum caters to properties with conventional loans, which are not backed by any government agency. It addresses the specific requirements set forth by the loan service or investor. 5. Investor-Specific Short Sale Addendum: Depending on the loan service or investor involved in the transaction, there may be addendums tailored to their specific requirements, ensuring compliance with their guidelines and procedures. The South Carolina Short Sale Addendum to Contract for the Price, Purchase and Sale of Real Estate outlines crucial details such as the purchase price, contingency periods, necessary approvals, and the allocation of costs between the buyer and seller. It also specifies the responsibilities of both parties, including the requirement for the seller to provide necessary documentation to support the short sale process. Given the sensitive nature of short sale transactions, it is essential to consult with a qualified real estate attorney or professional to ensure compliance with South Carolina laws and regulations. Through the use of a comprehensive South Carolina Short Sale Addendum, buyers and sellers can protect their interests and facilitate a smooth and legally compliant short sale transaction.The South Carolina Short Sale Addendum to Contract for the Price, Purchase and Sale of Real Estate is a crucial document that specifies the terms and conditions associated with a short sale transaction in South Carolina. This addendum is used when a property owner is facing financial distress and is unable to pay off their mortgage. It allows them to sell the property for less than the outstanding loan amount, with the approval of the lender. There are various types of South Carolina Short Sale Addendums available, tailored to specific scenarios and considerations. Some common types include: 1. Traditional Short Sale Addendum: This addendum is used for a typical short sale scenario where the property owner is in financial hardship and the lender agrees to accept less than the full loan amount as payment. 2. FHA Short Sale Addendum: This addendum is specific to properties financed by the Federal Housing Administration (FHA). It incorporates additional requirements and guidelines mandated by the FHA for short sales. 3. VA Short Sale Addendum: Designed for properties with mortgages guaranteed by the Department of Veterans Affairs (VA), this addendum includes provisions unique to VA loans and outlines specific procedures for obtaining the VA's approval for a short sale. 4. Conventional Short Sale Addendum: This addendum caters to properties with conventional loans, which are not backed by any government agency. It addresses the specific requirements set forth by the loan service or investor. 5. Investor-Specific Short Sale Addendum: Depending on the loan service or investor involved in the transaction, there may be addendums tailored to their specific requirements, ensuring compliance with their guidelines and procedures. The South Carolina Short Sale Addendum to Contract for the Price, Purchase and Sale of Real Estate outlines crucial details such as the purchase price, contingency periods, necessary approvals, and the allocation of costs between the buyer and seller. It also specifies the responsibilities of both parties, including the requirement for the seller to provide necessary documentation to support the short sale process. Given the sensitive nature of short sale transactions, it is essential to consult with a qualified real estate attorney or professional to ensure compliance with South Carolina laws and regulations. Through the use of a comprehensive South Carolina Short Sale Addendum, buyers and sellers can protect their interests and facilitate a smooth and legally compliant short sale transaction.