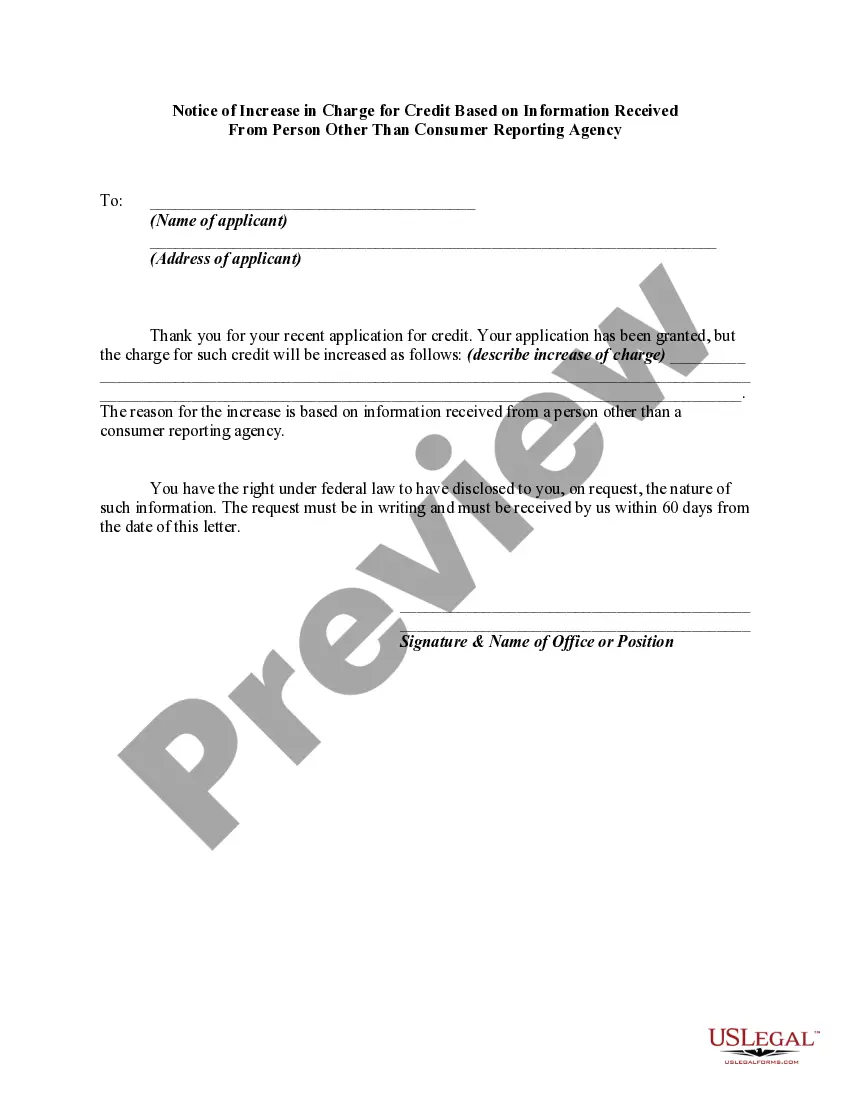

Whenever credit for personal, family, or household purposes involving a consumer is denied or the charge for the credit is increased either wholly or partly because of information obtained from a person other than a credit reporting agency bearing on the consumer's creditworthiness, credit standing, credit capacity, character, general reputation, personal characteristics, or mode of living, certain requirements must be met. The user of such information, when the adverse action is communicated to the consumer, must clearly and accurately disclose the consumer's right to make a written request for disclosure of the information. If such a request is made and is received within 60 days after the consumer learned of the adverse action, the user, within a reasonable period of time, must disclose to the consumer the nature of the information.

South Carolina Notice of Increase in charge of Credit Based on Information Received From Person Other Than Consumer Reporting Agency is a legal document used to notify individuals in South Carolina about changes in their credit charges based on information received from a source other than a consumer reporting agency. This notice is an important communication between the credit issuer and the consumer, ensuring transparency in pricing adjustments related to their credit account. One type of South Carolina Notice of Increase in charge of Credit Based on Information Received From Person Other Than Consumer Reporting Agency is related to changes in interest rates. Credit issuers have the right to adjust interest rates based on various factors, such as changes in the market or the borrower's credit score. The notice communicates the new interest rate to the consumer, along with the effective date of the change. Another type of South Carolina Notice of Increase in charge of Credit Based on Information Received From Person Other Than Consumer Reporting Agency pertains to fees and charges associated with the credit account. These can include annual fees, late payment fees, or over-limit fees. When the credit issuer decides to modify any of these charges, they must provide a written notice to the consumer, specifying the updated fees or charges, and explaining the reasons for the increase. It is crucial to note that South Carolina law requires credit issuers to provide this notice within a specific timeframe before the changes take effect. The notice must reach the consumer at least 45 days before the increase in charges occurs. This time frame allows consumers to evaluate their options, make necessary adjustments to their finances, or even consider alternatives if they find the increased charges unfavorable. The South Carolina Notice of Increase in charge of Credit Based on Information Received From Person Other Than Consumer Reporting Agency must include certain key details to comply with legal requirements. These details typically involve the consumer's name, account number, and contact information. Additionally, the notice should clearly state the current and new charges being applied, along with an explanation of the change and any potential impacts on the overall cost of the credit. In conclusion, the South Carolina Notice of Increase in charge of Credit Based on Information Received From Person Other Than Consumer Reporting Agency is a legal document that ensures transparency and communication between credit issuers and consumers regarding changes in credit charges. By providing advance notice, credit issuers allow consumers the opportunity to assess the impact of these changes and make informed decisions about their credit accounts.South Carolina Notice of Increase in charge of Credit Based on Information Received From Person Other Than Consumer Reporting Agency is a legal document used to notify individuals in South Carolina about changes in their credit charges based on information received from a source other than a consumer reporting agency. This notice is an important communication between the credit issuer and the consumer, ensuring transparency in pricing adjustments related to their credit account. One type of South Carolina Notice of Increase in charge of Credit Based on Information Received From Person Other Than Consumer Reporting Agency is related to changes in interest rates. Credit issuers have the right to adjust interest rates based on various factors, such as changes in the market or the borrower's credit score. The notice communicates the new interest rate to the consumer, along with the effective date of the change. Another type of South Carolina Notice of Increase in charge of Credit Based on Information Received From Person Other Than Consumer Reporting Agency pertains to fees and charges associated with the credit account. These can include annual fees, late payment fees, or over-limit fees. When the credit issuer decides to modify any of these charges, they must provide a written notice to the consumer, specifying the updated fees or charges, and explaining the reasons for the increase. It is crucial to note that South Carolina law requires credit issuers to provide this notice within a specific timeframe before the changes take effect. The notice must reach the consumer at least 45 days before the increase in charges occurs. This time frame allows consumers to evaluate their options, make necessary adjustments to their finances, or even consider alternatives if they find the increased charges unfavorable. The South Carolina Notice of Increase in charge of Credit Based on Information Received From Person Other Than Consumer Reporting Agency must include certain key details to comply with legal requirements. These details typically involve the consumer's name, account number, and contact information. Additionally, the notice should clearly state the current and new charges being applied, along with an explanation of the change and any potential impacts on the overall cost of the credit. In conclusion, the South Carolina Notice of Increase in charge of Credit Based on Information Received From Person Other Than Consumer Reporting Agency is a legal document that ensures transparency and communication between credit issuers and consumers regarding changes in credit charges. By providing advance notice, credit issuers allow consumers the opportunity to assess the impact of these changes and make informed decisions about their credit accounts.