A secured transaction is created when a buyer or borrower (debtor) grants a seller or lender (creditor or secured party) a security interest in personal property (collateral). A security interest allows a creditor to repossess and sell the collateral if a debtor fails to pay a secured debt.

The Truth-in-Lending Act (TILA) is part of the Federal Consumer Credit Protection Act. The purpose of the TILA is to make full disclosure to debtors of what they are being charged for the credit they are receiving. The Act merely asks lenders to be honest to the debtors and not cover up what they are paying for the credit. Regulation Z is a federal regulation prepared by the Federal Reserve Board to carry out the details of the Act. TILA applies to consumer credit transactions. Consumer credit is credit for personal or household use and not commercial use or business purposes.

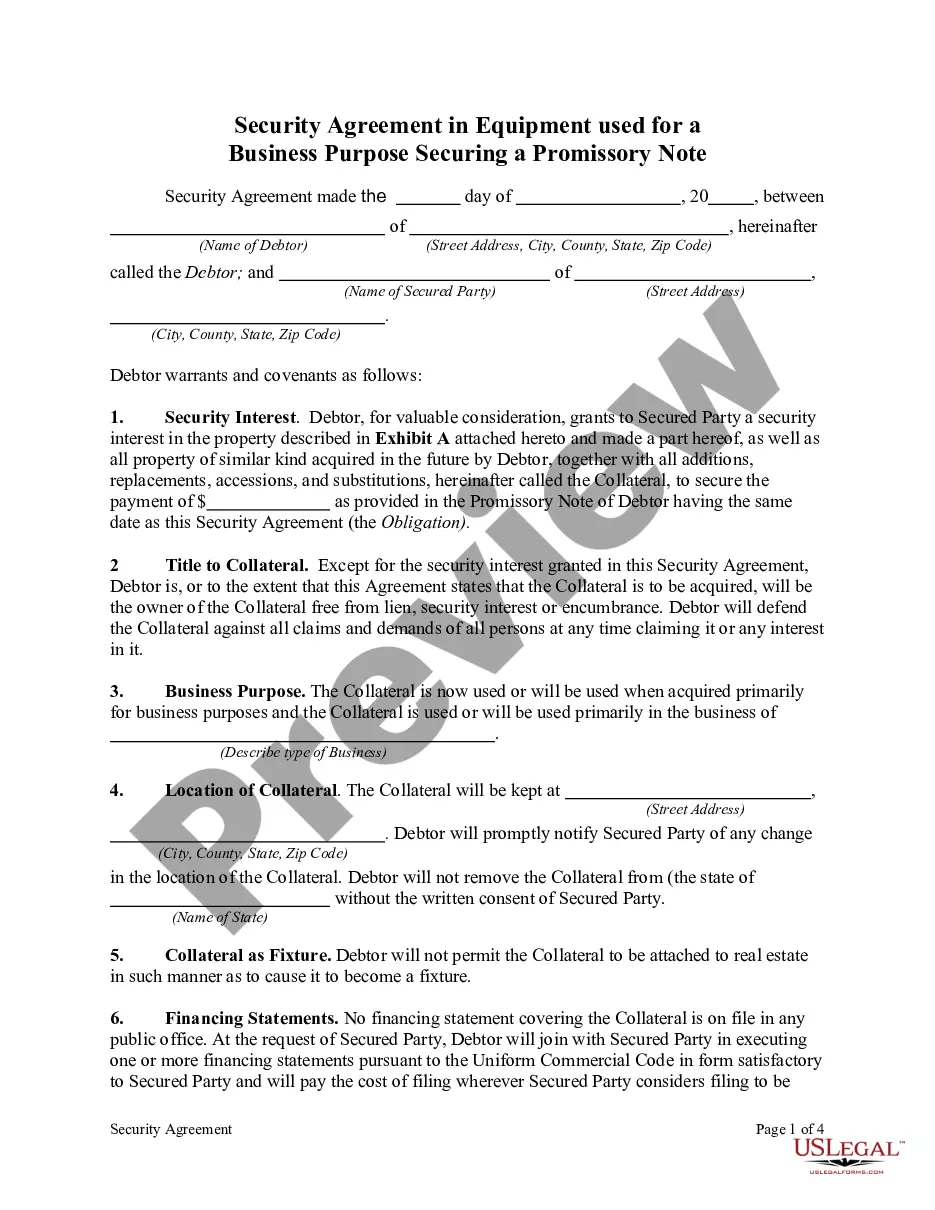

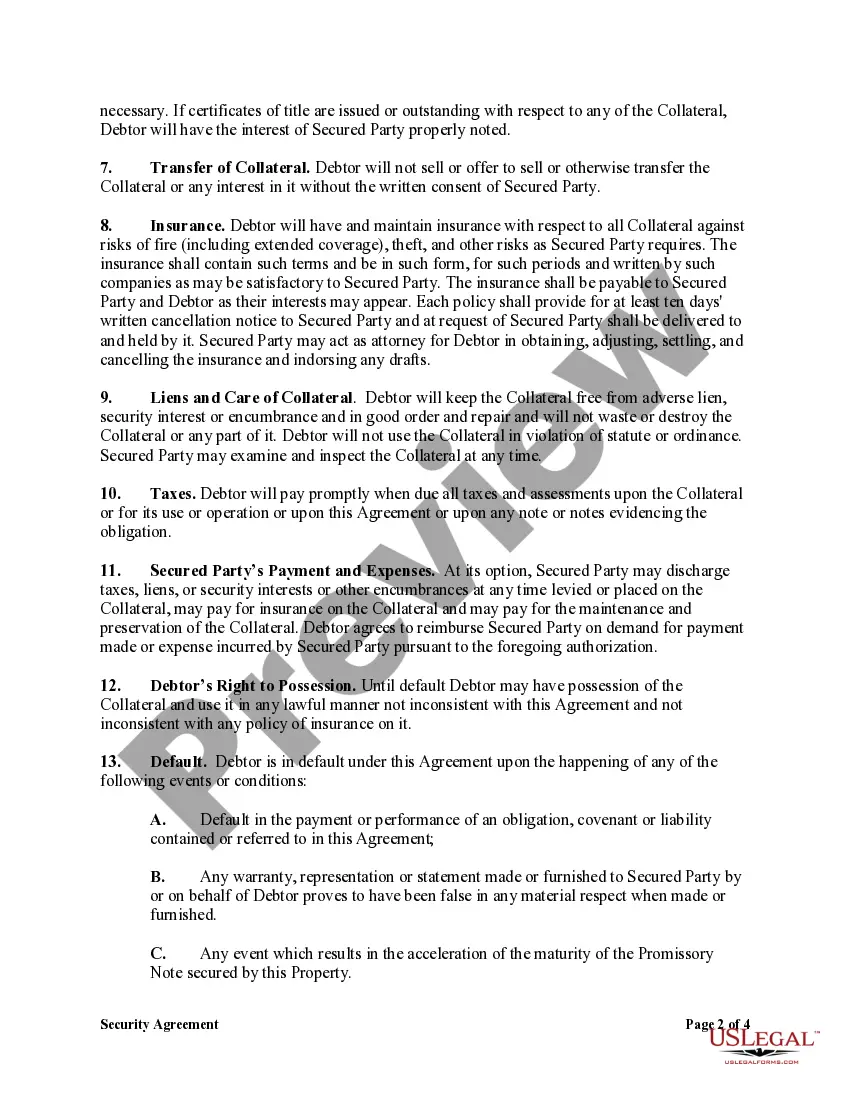

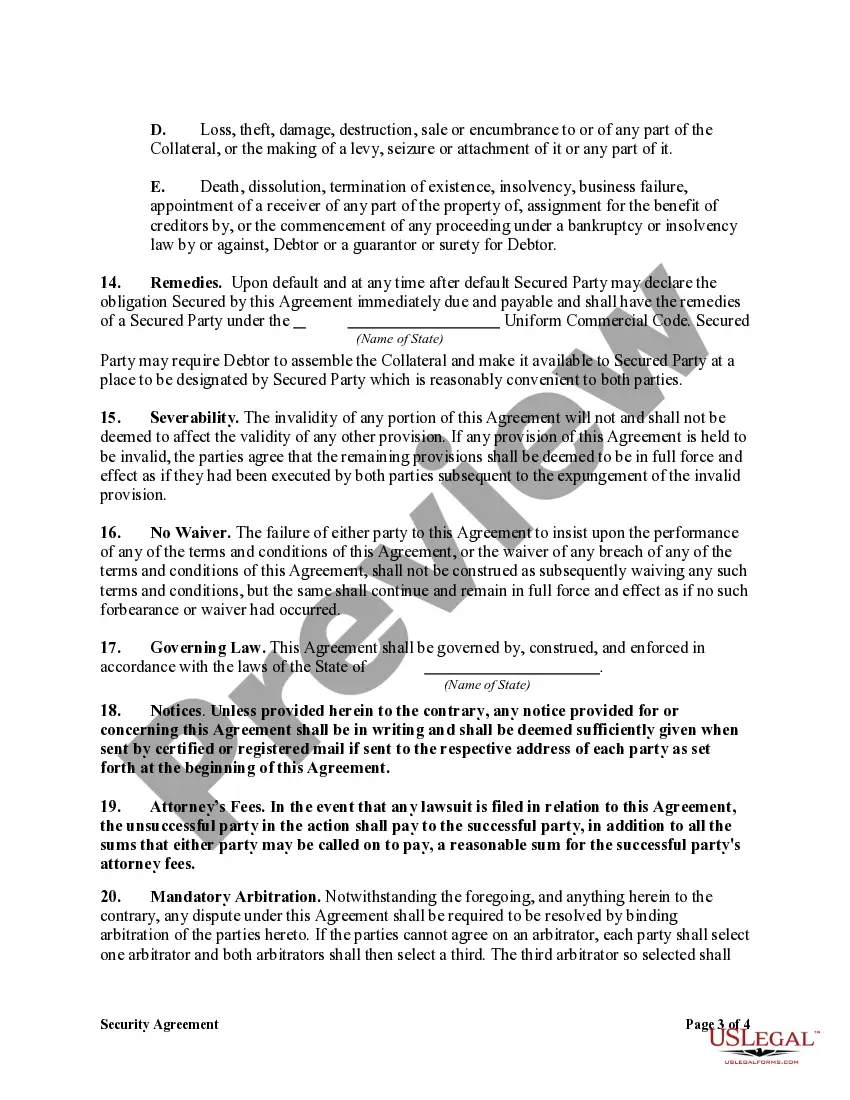

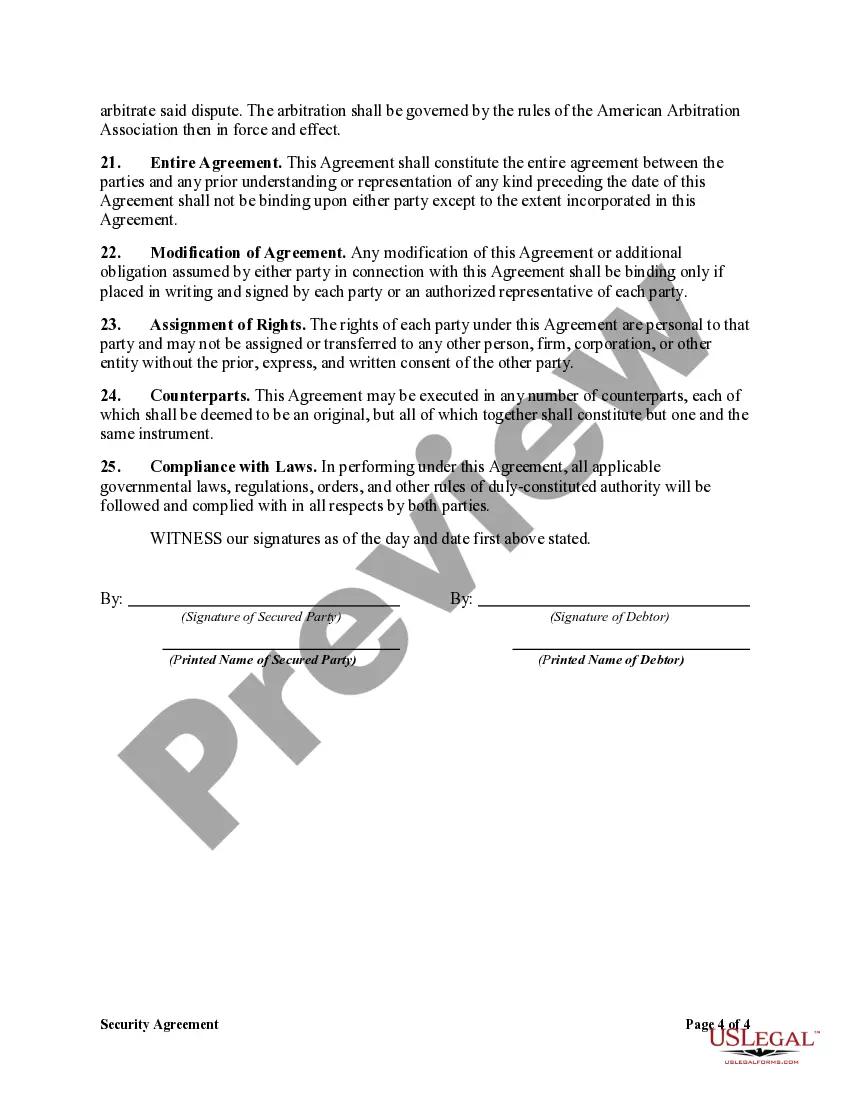

A South Carolina Security Agreement in Equipment for Business Purposes — Securing Promissory Note is a legal document that provides security for a promissory note used in commercial transactions. This agreement outlines the terms and conditions under which the equipment purchased through the promissory note serves as collateral for the loan. In South Carolina, there are several types of security agreements that can be used to secure promissory notes for business purposes. These agreements may vary depending on the specific needs and circumstances of the parties involved. Some common variations include: 1. General Security Agreement: This is a comprehensive security agreement that covers all types of collateral, including equipment, inventory, and accounts receivable. It provides a broad scope of protection for the lender. 2. Specific Equipment Security Agreement: This type of agreement is tailored to secure a specific piece or type of equipment used in the business transaction. It details the specific equipment covered by the agreement and the obligations of the borrower. 3. Floating Lien Agreement: A floating lien agreement is used when the collateral is subject to change or rotation, such as inventory. It allows the lender to maintain a security interest in the equipment that is constantly changing. 4. Purchase Money Security Agreement: This type of agreement is used when the equipment being financed by the promissory note is also being purchased using the loan. It states that the collateral for the loan is the equipment itself and provides security for both parties involved. A South Carolina Security Agreement in Equipment for Business Purposes — Securing Promissory Note is an essential legal document that helps protect both the lender and the borrower in commercial transactions. It ensures that the lender has recourse in case of default by the borrower and provides the borrower with the necessary financing to acquire the equipment needed for their business operations. To draft a valid and enforceable security agreement, it is advisable to seek the assistance of a qualified attorney experienced in South Carolina commercial law. They can guide you through the process, ensuring that all necessary provisions are included and that the agreement complies with the applicable state laws and regulations.A South Carolina Security Agreement in Equipment for Business Purposes — Securing Promissory Note is a legal document that provides security for a promissory note used in commercial transactions. This agreement outlines the terms and conditions under which the equipment purchased through the promissory note serves as collateral for the loan. In South Carolina, there are several types of security agreements that can be used to secure promissory notes for business purposes. These agreements may vary depending on the specific needs and circumstances of the parties involved. Some common variations include: 1. General Security Agreement: This is a comprehensive security agreement that covers all types of collateral, including equipment, inventory, and accounts receivable. It provides a broad scope of protection for the lender. 2. Specific Equipment Security Agreement: This type of agreement is tailored to secure a specific piece or type of equipment used in the business transaction. It details the specific equipment covered by the agreement and the obligations of the borrower. 3. Floating Lien Agreement: A floating lien agreement is used when the collateral is subject to change or rotation, such as inventory. It allows the lender to maintain a security interest in the equipment that is constantly changing. 4. Purchase Money Security Agreement: This type of agreement is used when the equipment being financed by the promissory note is also being purchased using the loan. It states that the collateral for the loan is the equipment itself and provides security for both parties involved. A South Carolina Security Agreement in Equipment for Business Purposes — Securing Promissory Note is an essential legal document that helps protect both the lender and the borrower in commercial transactions. It ensures that the lender has recourse in case of default by the borrower and provides the borrower with the necessary financing to acquire the equipment needed for their business operations. To draft a valid and enforceable security agreement, it is advisable to seek the assistance of a qualified attorney experienced in South Carolina commercial law. They can guide you through the process, ensuring that all necessary provisions are included and that the agreement complies with the applicable state laws and regulations.