South Carolina Corporate Asset Purchase Agreement

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Corporate Asset Purchase Agreement?

Selecting the finest certified document template can be rather challenging.

Clearly, there are many designs accessible online, but how can you find the certified form you require.

Utilize the US Legal Forms website. The platform offers a vast array of designs, such as the South Carolina Corporate Asset Purchase Agreement, which can be utilized for both business and personal purposes.

If the form does not fulfill your requirements, use the Search field to find the correct form. Once you are confident that the form meets your needs, click the Purchase now button to acquire the form. Choose the pricing plan you prefer and enter the necessary information. Create your account and complete the order using your PayPal account or credit card. Select the document format and download the certified document template to your device. Complete, revise, print, and sign the obtained South Carolina Corporate Asset Purchase Agreement. US Legal Forms is the largest collection of certified forms where you can find numerous document templates. Utilize the service to obtain properly crafted documents that comply with state regulations.

- All the documents are verified by experts and comply with state and federal regulations.

- If you are already registered, Log In to your account and click on the Obtain button to download the South Carolina Corporate Asset Purchase Agreement.

- Use your account to search through the certified documents you may have previously ordered.

- Visit the My documents section of your account to download another copy of the document you need.

- If you are a new user of US Legal Forms, here are straightforward steps you should follow.

- First, make sure you select the correct form for your city/county. You can review the form using the Preview button and examine the form's outline to ensure it is suitable for you.

Form popularity

FAQ

Absolutely, if you registered your S Corporation in South Carolina, you must file an annual report. This ensures that your corporation remains compliant with state regulations. Regular filings demonstrate your commitment to maintaining good standing. Using platforms like US Legal Forms can help streamline this process for you.

Yes, South Carolina mandates that corporations file an annual report. This report is essential for keeping the state's records up-to-date and confirms that the corporation is still active. Ignoring this requirement could lead to administrative dissolution. To simplify this process, you can utilize US Legal Forms for filing assistance.

Yes, in South Carolina, annual reports are typically required for corporations. These reports serve to provide the state with updated information about the company, including its address and registered agent. Failing to file can result in penalties or even dissolution. It is advisable to consult resources like US Legal Forms to ensure compliance with these requirements.

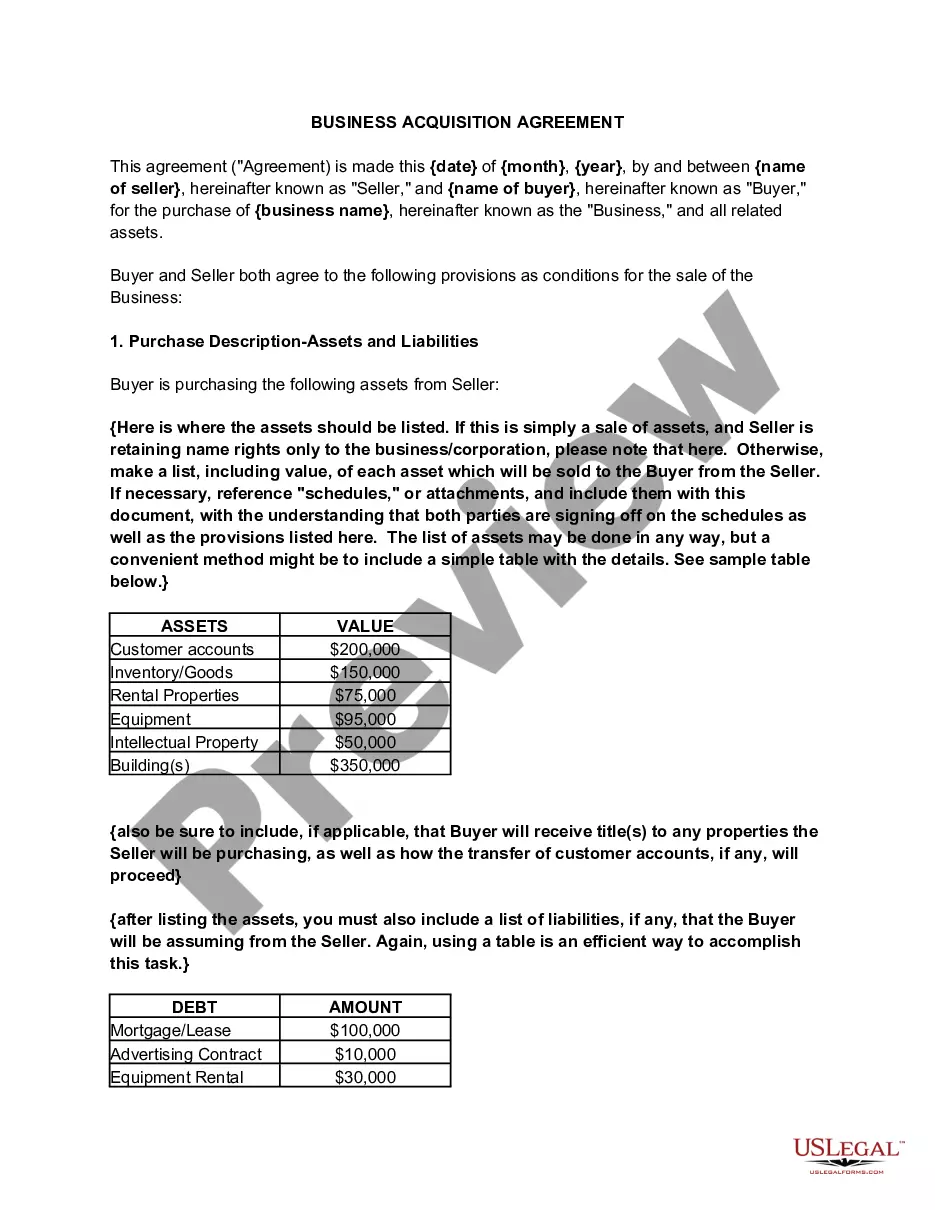

An asset purchase involves the purchase of the selling company's assets -- including facilities, vehicles, equipment, and stock or inventory. A stock purchase involves the purchase of the selling company's stock only.

Simply put, Recitals are used to explain those matters of fact which are necessary to make a proposed transaction intelligible. Recitals are like a quick start guide to an APA, acquisition contract, or merger agreement.

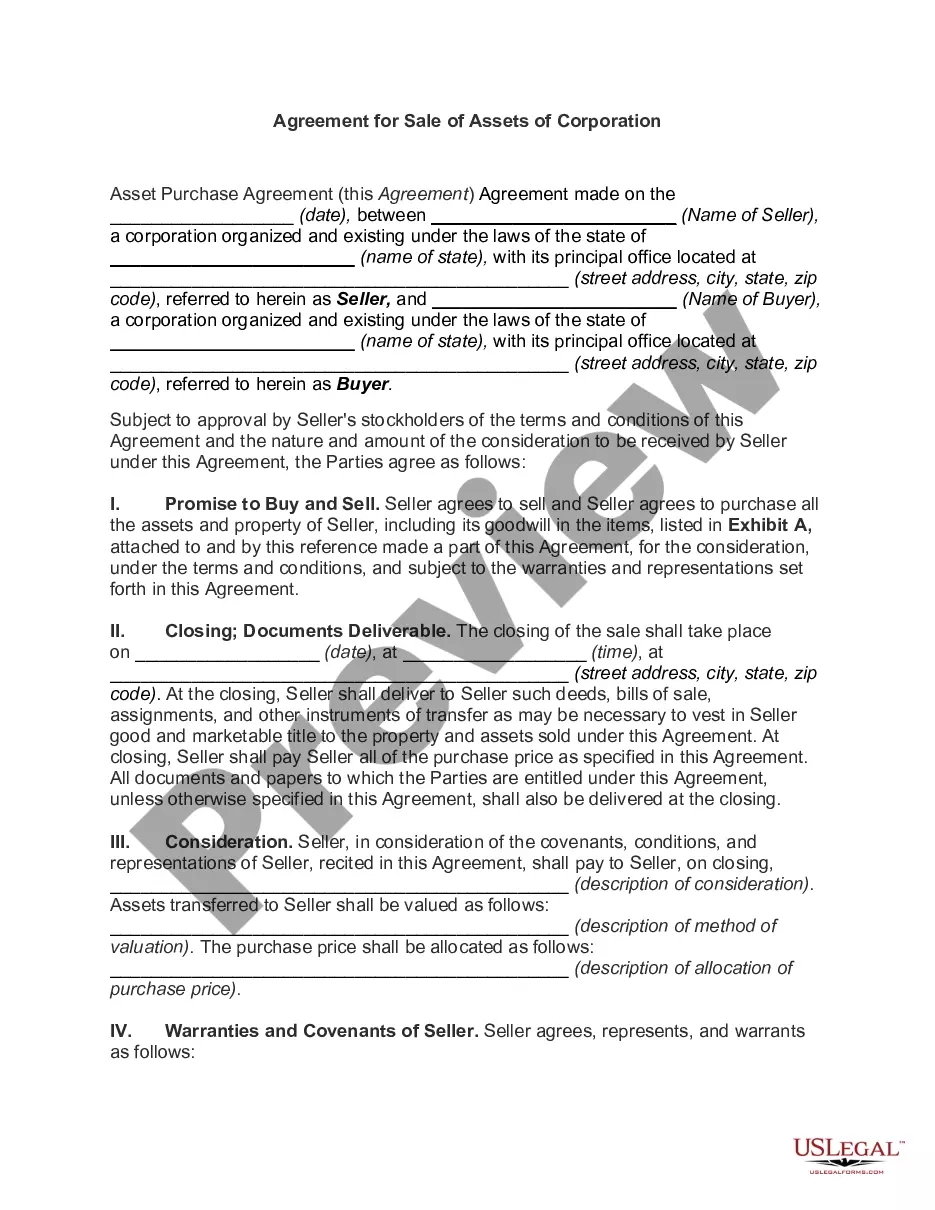

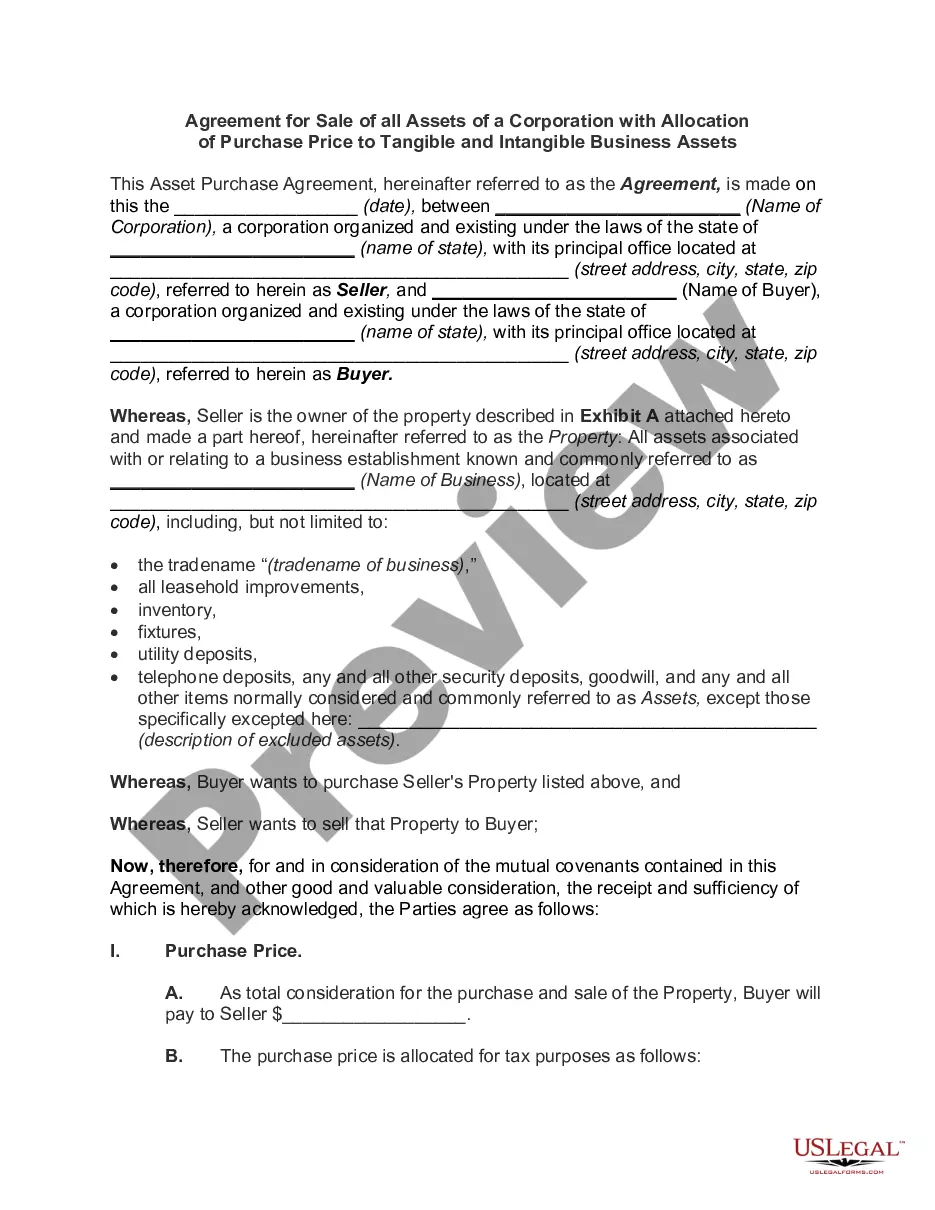

An asset purchase agreement is an agreement between a buyer and a seller to purchase property, like business assets or real property, either on their own or as part of a merger-acquisition.

The asset purchase agreement is often drafted up towards the end of the negotiation stage, so that the parties can have a final record of their agreement. The document essentially operates as a contract, creating legally binding duties on each of the parties involved.

An asset purchase involves just the assets of a company. In either format, determining what is being acquired is critical. This article focuses on some of the important categories of assets to consider in a business purchase: real estate, personal property, and intellectual property.

Parts of an Asset Purchase AgreementRecitals. The opening paragraph of an asset purchase agreement includes the buyer and seller's name and address as well as the date of signing.Definitions.Purchase Price and Allocation.Closing Terms.Warranties.Covenants.Indemnification.Governance.More items...

Provisions of an APA may include payment of purchase price, monthly installments, liens and encumbrances on the assets, condition precedent for the closing, etc. An APA differs from a stock purchase agreement (SPA) under which company shares, title to assets, and title to liabilities are also sold.