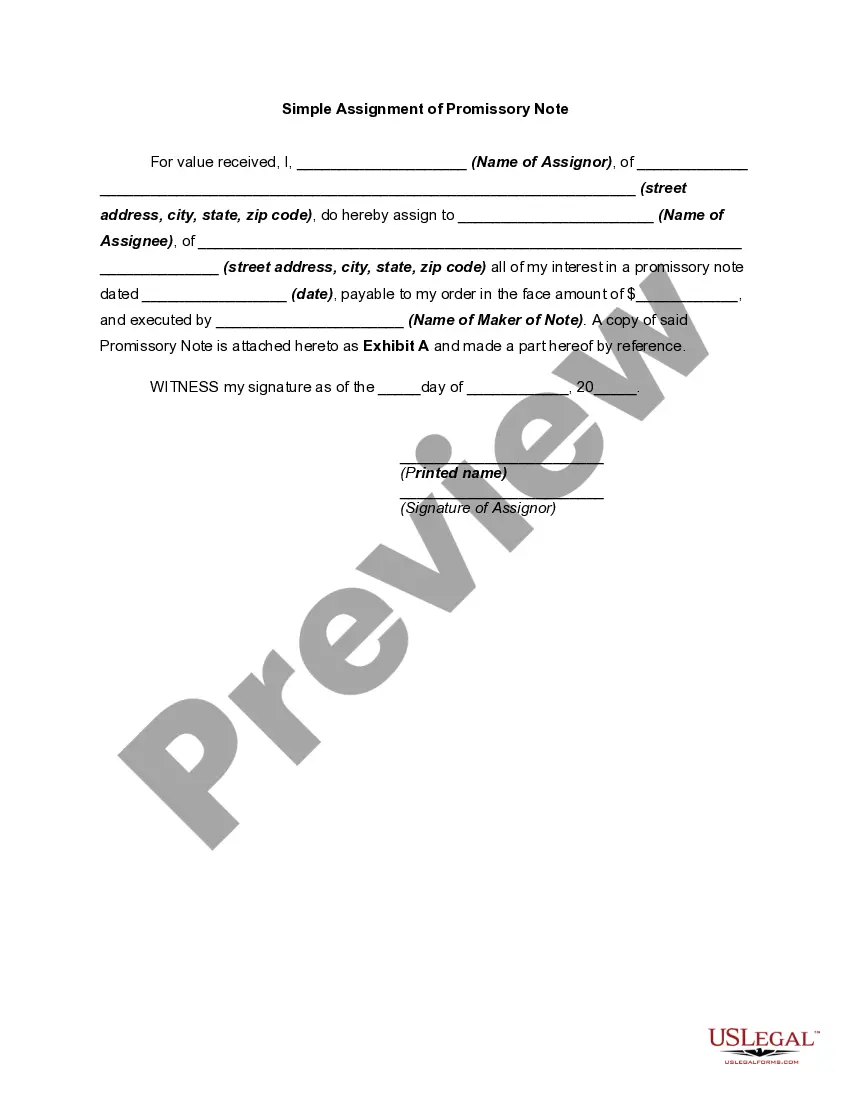

The South Carolina Simple Promissory Note for Family Loan is a legal document that outlines the terms and conditions of a loan between family members in South Carolina. It is a written agreement that solidifies the borrower's promise to repay the loaned amount to the lender, along with any accrued interest, within an agreed-upon time frame. This promissory note serves as evidence of the loan transaction and protects the rights of both the borrower and the lender. It establishes clear expectations and terms, such as the loan amount, repayment schedule, interest rate (if applicable), and any late fees or penalties. By creating this formal agreement, it helps maintain the financial relationship between family members by ensuring all parties have a clear understanding of their obligations. There are several types of South Carolina Simple Promissory Notes for Family Loan, each catering to specific loan arrangements or scenarios. Some of these variations include: 1. South Carolina Secured Promissory Note: This type of note includes collateral to secure the loan, typically a valuable asset belonging to the borrower, such as a property or vehicle. In case of default, the lender has the right to claim the collateral in order to recover the outstanding amount. 2. South Carolina Unsecured Promissory Note: Unlike a secured promissory note, an unsecured note does not require any collateral. It solely relies on the borrower's personal guarantee and creditworthiness for repayment. As there is no specific property offered as collateral, unsecured loans generally have higher interest rates to compensate for the increased risk taken by the lender. 3. South Carolina Demand Promissory Note: This type of note allows the lender to demand repayment of the loan at any time, without specifying a specific repayment schedule. However, a reasonable notice period is typically provided to the borrower before demanding full repayment. 4. South Carolina Installment Promissory Note: This note establishes a fixed repayment schedule, with predetermined monthly, quarterly, or yearly installments. It outlines the precise amounts and due dates for each installment, providing clarity and structure to the repayment process. 5. South Carolina Forgivable Promissory Note: This note describes a loan agreement that includes a clause stating that the loan will be forgiven under certain circumstances, such as the borrower meeting specific conditions or remaining in good standing for a specified period. Forgivable promissory notes are often used in employee incentive programs or educational loan agreements. It is crucial for all parties involved in a family loan transaction to carefully consider their specific circumstances and requirements when choosing the type of promissory note to utilize. Consulting with a legal professional can help ensure compliance with South Carolina's loan regulations and prepare a customized document that covers the necessary details for a successful family loan.

South Carolina Simple Promissory Note for Family Loan

Description

How to fill out South Carolina Simple Promissory Note For Family Loan?

Discovering the right authorized record template can be a battle. Obviously, there are tons of web templates accessible on the Internet, but how do you find the authorized type you will need? Use the US Legal Forms internet site. The support gives thousands of web templates, including the South Carolina Simple Promissory Note for Family Loan, which you can use for enterprise and private needs. All the varieties are examined by experts and satisfy federal and state needs.

If you are presently signed up, log in to the accounts and click the Obtain option to find the South Carolina Simple Promissory Note for Family Loan. Make use of your accounts to search with the authorized varieties you possess ordered in the past. Go to the My Forms tab of your own accounts and obtain yet another duplicate in the record you will need.

If you are a fresh customer of US Legal Forms, listed here are basic guidelines that you should follow:

- Initially, make certain you have selected the appropriate type for your metropolis/area. You can look over the form making use of the Review option and look at the form outline to make certain it is the right one for you.

- In case the type does not satisfy your expectations, take advantage of the Seach discipline to get the proper type.

- Once you are certain that the form would work, select the Purchase now option to find the type.

- Pick the costs prepare you want and enter in the necessary information. Design your accounts and buy an order making use of your PayPal accounts or bank card.

- Pick the file format and down load the authorized record template to the product.

- Total, edit and print out and sign the received South Carolina Simple Promissory Note for Family Loan.

US Legal Forms may be the biggest local library of authorized varieties in which you will find different record web templates. Use the service to down load professionally-produced paperwork that follow express needs.