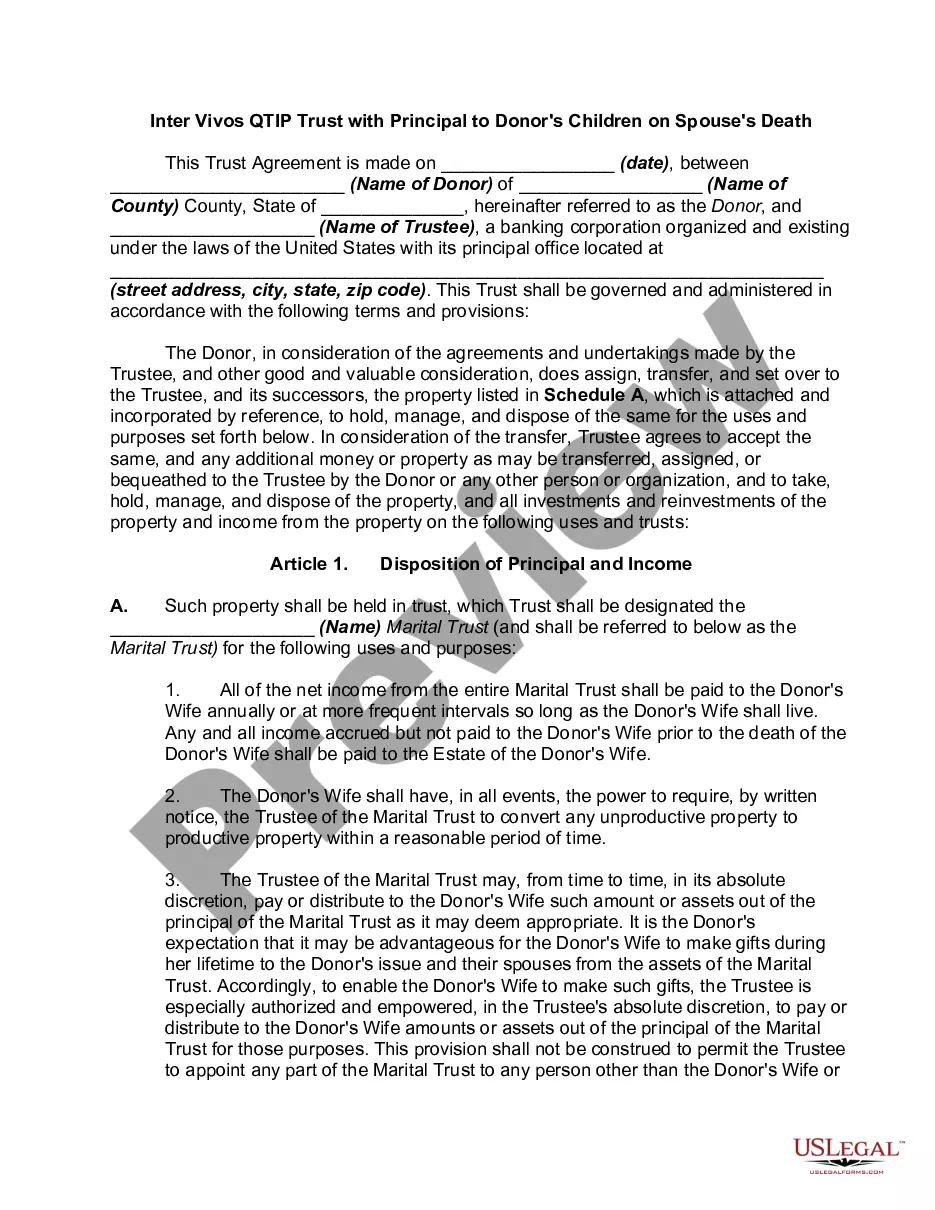

A trust is a fiduciary relationship in which one party holds legal title to another's property for the benefit of a party who holds equitable title to the property. An inter vivos trust is a trust that becomes effective during the lifetime of the person creating the trust (the settler or trustor).

A qualified terminable interest property trust, often referred to as a "QTIP" trust, allows a bequest to a spouse in trust that, after a proper election by the beneficiary spouse, qualifies for the unlimited marital deduction:

" if the beneficiary spouse is entitled to all of the income from the trust property,

" if the income is payable annually or at more frequent intervals, and

" if no person, including the beneficiary spouse, has the power to appoint any part of the qualifying property to any person other than the beneficiary spouse during the beneficiary spouse's lifetime.

In order that the property transferred to a surviving spouse by means of an inter vivos marital deduction trust qualify for the marital deduction, the property must be includible in the trustor's gross estate for federal estate tax purpose.

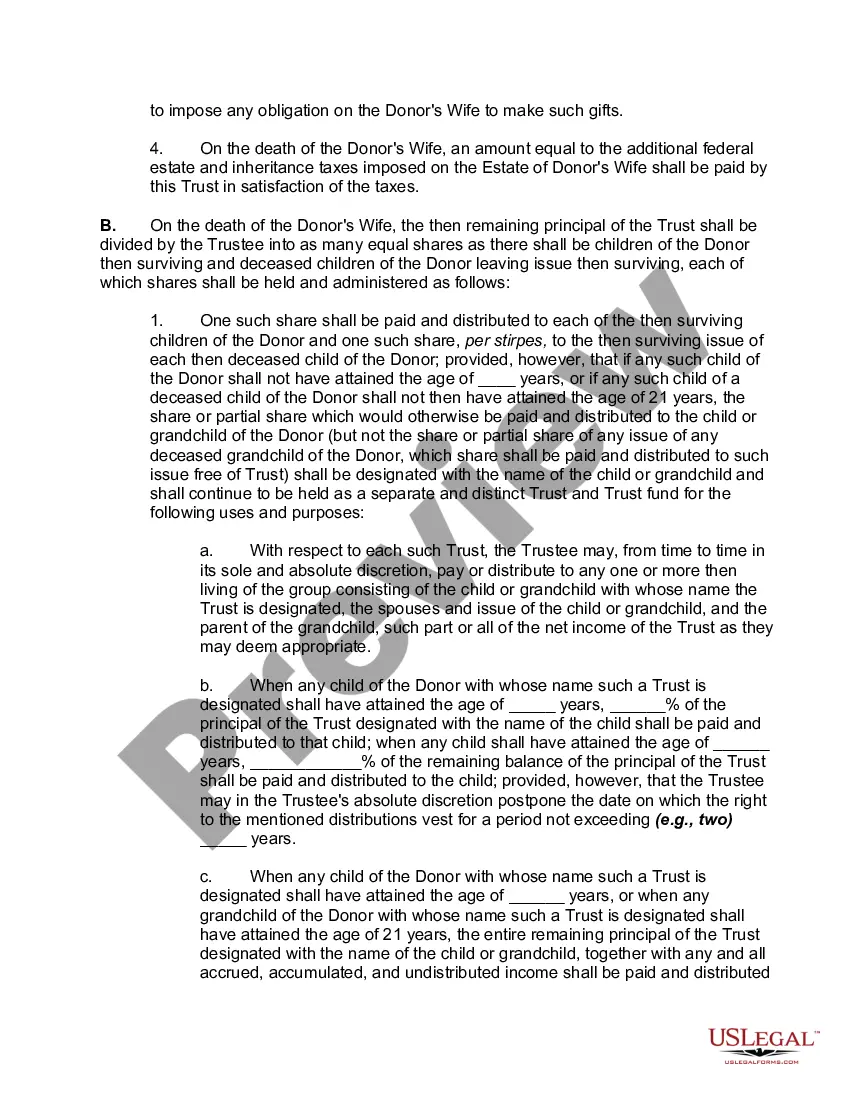

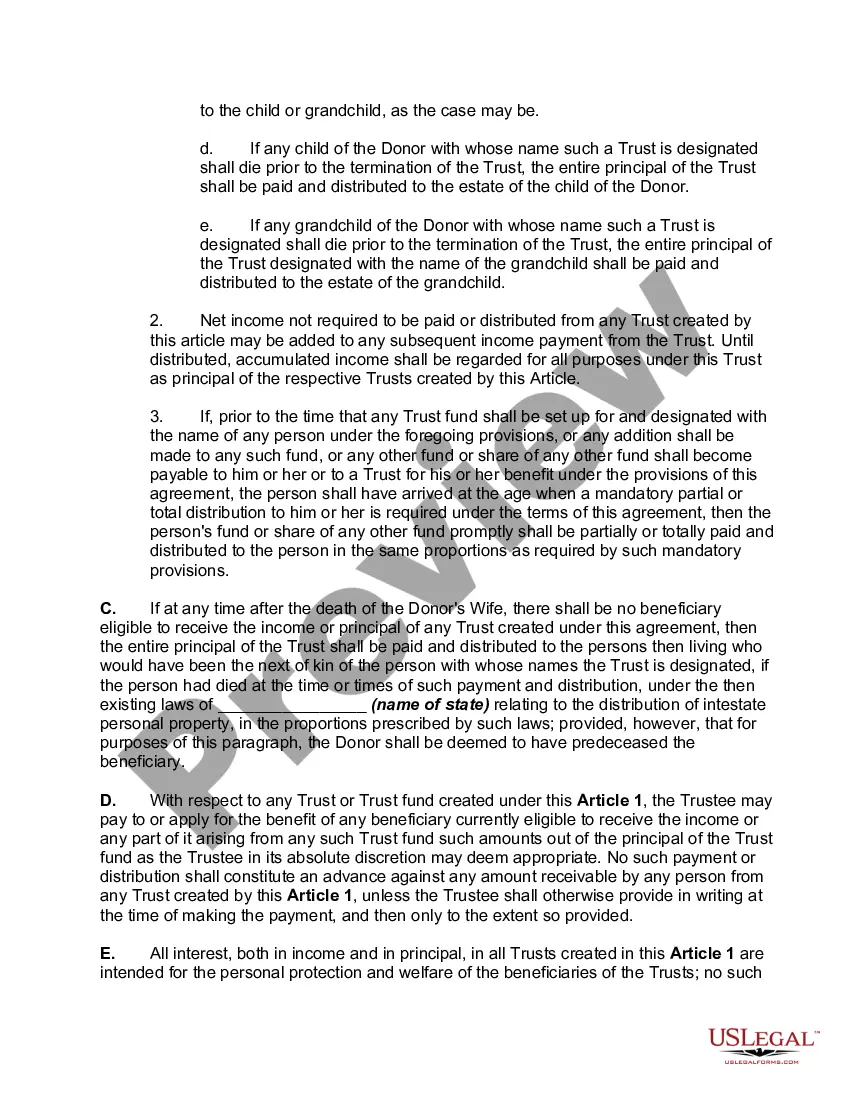

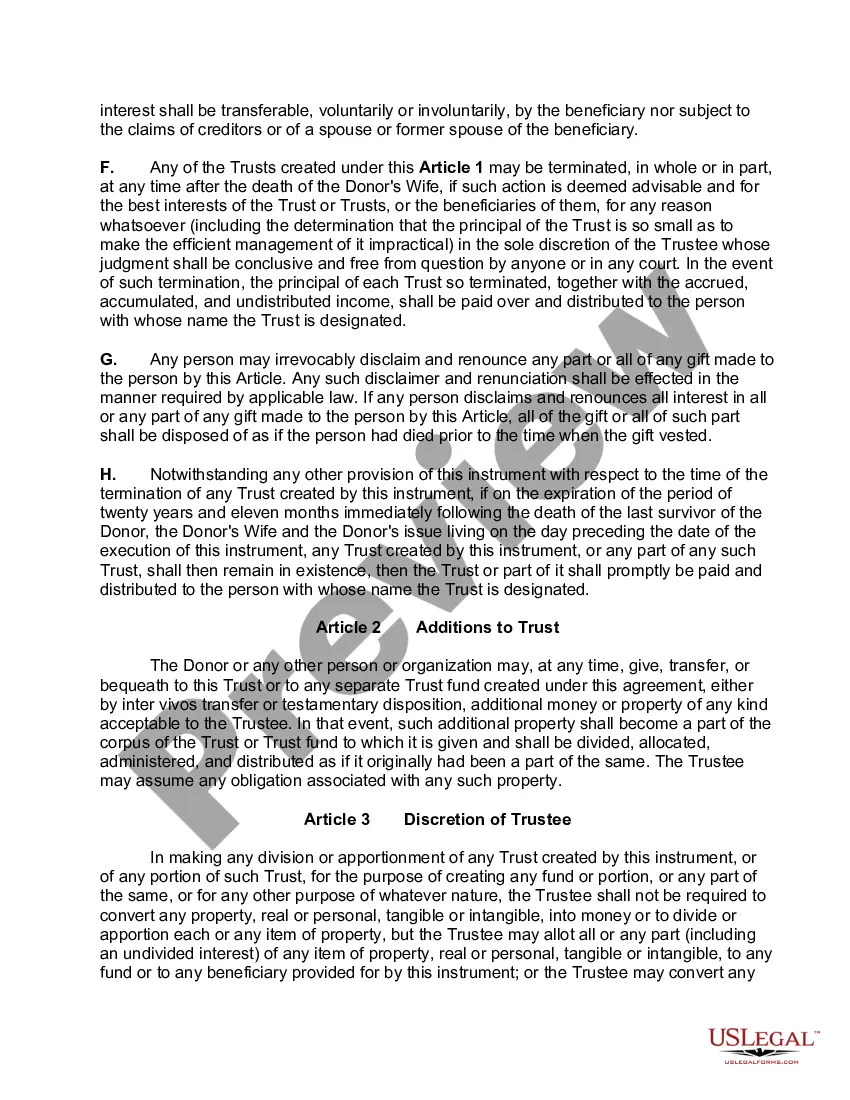

A South Carolina Inter Vivos TIP Trust with Principal to Donor's Children on Spouse's Death is a specific type of trust designed to provide financial security and estate planning benefits for married couples in South Carolina. TIP stands for "qualified terminable interest property," which refers to assets that will pass from one spouse to the other upon death while qualifying for a marital deduction on federal estate tax returns. This trust is established during the lifetime of the donor (also known as the granter). The donor can transfer assets, typically cash, real estate, or stocks, into the trust while still retaining control over the assets and receiving income generated by them. The trust is irrevocable, meaning that once the assets are transferred, the donor cannot revoke or change provisions of the trust without the consent of the beneficiaries and the court. Upon the death of the donor's spouse, the trust is structured to ensure that the surviving spouse receives income generated by the trust assets for the remainder of their life. The surviving spouse does not have direct control over the trust assets but can benefit from the income they produce. This allows the assets to be effectively utilized for the surviving spouse's needs while preserving the trust's principal to be passed on to the donor's children after the surviving spouse's death. The South Carolina Inter Vivos TIP Trust with Principal to Donor's Children on Spouse's Death helps protect the rights and financial interests of both the surviving spouse and the donor's children. It ensures that the surviving spouse is taken care of during their lifetime while also safeguarding the ultimate inheritance of the trust assets for the donor's children. Different types of South Carolina Inter Vivos TIP Trusts with Principal to Donor's Children on Spouse's Death may include variations in the distribution of trust income, principal, or the specific terms and conditions outlined in the trust agreement. Some variations may allow for discretionary distributions to the surviving spouse, while others may specify certain uses for the trust's principal. Trust agreements can also include provisions for contingent beneficiaries, such as grandchildren or charitable organizations. In summary, a South Carolina Inter Vivos TIP Trust with Principal to Donor's Children on Spouse's Death is a specialized estate planning tool that offers flexibility in managing assets, ensuring financial security for the surviving spouse, and providing for the ultimate distribution of the trust assets to the donor's children.A South Carolina Inter Vivos TIP Trust with Principal to Donor's Children on Spouse's Death is a specific type of trust designed to provide financial security and estate planning benefits for married couples in South Carolina. TIP stands for "qualified terminable interest property," which refers to assets that will pass from one spouse to the other upon death while qualifying for a marital deduction on federal estate tax returns. This trust is established during the lifetime of the donor (also known as the granter). The donor can transfer assets, typically cash, real estate, or stocks, into the trust while still retaining control over the assets and receiving income generated by them. The trust is irrevocable, meaning that once the assets are transferred, the donor cannot revoke or change provisions of the trust without the consent of the beneficiaries and the court. Upon the death of the donor's spouse, the trust is structured to ensure that the surviving spouse receives income generated by the trust assets for the remainder of their life. The surviving spouse does not have direct control over the trust assets but can benefit from the income they produce. This allows the assets to be effectively utilized for the surviving spouse's needs while preserving the trust's principal to be passed on to the donor's children after the surviving spouse's death. The South Carolina Inter Vivos TIP Trust with Principal to Donor's Children on Spouse's Death helps protect the rights and financial interests of both the surviving spouse and the donor's children. It ensures that the surviving spouse is taken care of during their lifetime while also safeguarding the ultimate inheritance of the trust assets for the donor's children. Different types of South Carolina Inter Vivos TIP Trusts with Principal to Donor's Children on Spouse's Death may include variations in the distribution of trust income, principal, or the specific terms and conditions outlined in the trust agreement. Some variations may allow for discretionary distributions to the surviving spouse, while others may specify certain uses for the trust's principal. Trust agreements can also include provisions for contingent beneficiaries, such as grandchildren or charitable organizations. In summary, a South Carolina Inter Vivos TIP Trust with Principal to Donor's Children on Spouse's Death is a specialized estate planning tool that offers flexibility in managing assets, ensuring financial security for the surviving spouse, and providing for the ultimate distribution of the trust assets to the donor's children.