South Carolina Agreement to Purchase Note and Mortgage

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Agreement To Purchase Note And Mortgage?

You are able to commit time on the web attempting to find the legitimate file format that suits the state and federal specifications you require. US Legal Forms offers 1000s of legitimate kinds which can be evaluated by professionals. You can actually download or print out the South Carolina Agreement to Purchase Note and Mortgage from our support.

If you already possess a US Legal Forms profile, you are able to log in and then click the Download button. After that, you are able to total, revise, print out, or sign the South Carolina Agreement to Purchase Note and Mortgage. Each and every legitimate file format you get is your own property for a long time. To have another copy for any bought kind, go to the My Forms tab and then click the corresponding button.

If you are using the US Legal Forms internet site for the first time, stick to the easy recommendations under:

- Initial, ensure that you have selected the right file format to the state/area of your choice. See the kind explanation to ensure you have selected the correct kind. If readily available, utilize the Review button to search throughout the file format too.

- In order to locate another model of your kind, utilize the Search area to find the format that fits your needs and specifications.

- When you have discovered the format you need, just click Acquire now to carry on.

- Choose the costs strategy you need, type your credentials, and sign up for a merchant account on US Legal Forms.

- Comprehensive the financial transaction. You can utilize your charge card or PayPal profile to purchase the legitimate kind.

- Choose the file format of your file and download it to the product.

- Make adjustments to the file if necessary. You are able to total, revise and sign and print out South Carolina Agreement to Purchase Note and Mortgage.

Download and print out 1000s of file web templates using the US Legal Forms website, that offers the greatest assortment of legitimate kinds. Use professional and state-particular web templates to handle your company or personal requirements.

Form popularity

FAQ

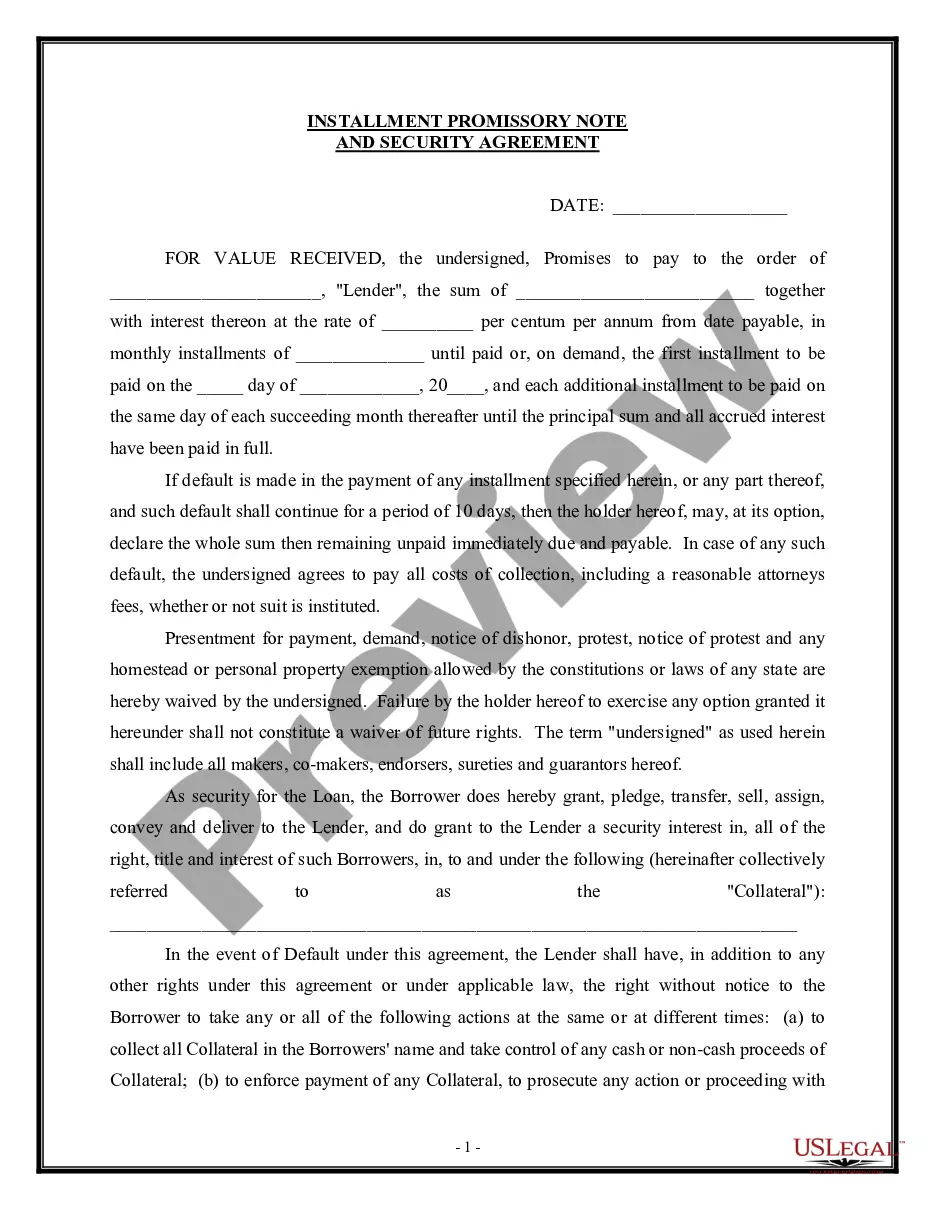

Although it is legally enforceable, a promissory note is less formal than a loan agreement and is suitable where smaller sums of money are involved. However, its terms - which can include a specific date of repayment, interest rate and repayment schedule - are more certain than those of an IOU.

Secured: A secured promissory note is common in traditional mortgages. It means the borrower backs their loan with collateral. For a mortgage, the collateral is the property. If the borrower fails to pay back their loan, the lender has a legal claim over the asset and, in extreme cases, may foreclose on the property.

A promissory note is generally sufficient if the amount of money is relatively small and there is a great deal of trust between the lender and the borrower (or debtor). In contrast, a loan agreement is more appropriate if the two parties do not know one another well and have substantial debt.

A promissory note is a written agreement containing the details of the mortgage loan, whereas a mortgage is a loan that is secured by real property. A promissory note is often referred to as a mortgage, but they are separate contracts.

So, as a rule of thumb, if someone is on the Deed, they must be on the Mortgage. But just because they are on the Mortgage, doesn't mean they are on the Note.

A loan note can offer greater flexibility than a simple loan agreement, while still being legally actionable should it need to be upheld in court. They are also much easier to enforce than an informal IOU because the legal terms of the agreement are much more clearly defined.

A borrower usually must sign a promissory note along with the mortgage. The promissory note gives legal protections to the lender if the borrower defaults on the debt and provides clarification to the borrower so that they understand their repayment obligations.

Promissory Note Vs. Mortgage. A promissory note is a document between the lender and the borrower in which the borrower promises to pay back the lender, it is a separate contract from the mortgage. The mortgage is a legal document that ties or "secures" a piece of real estate to an obligation to repay money.