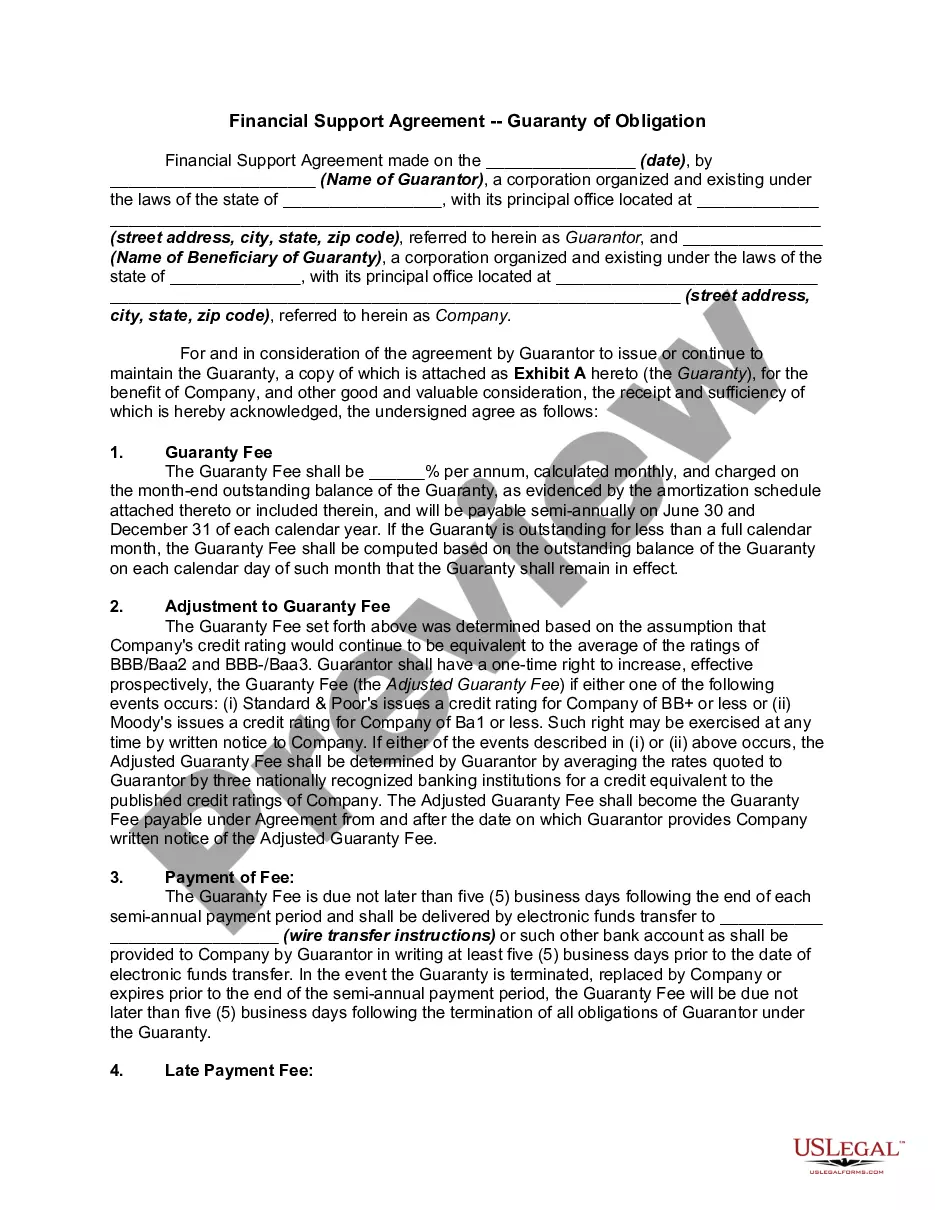

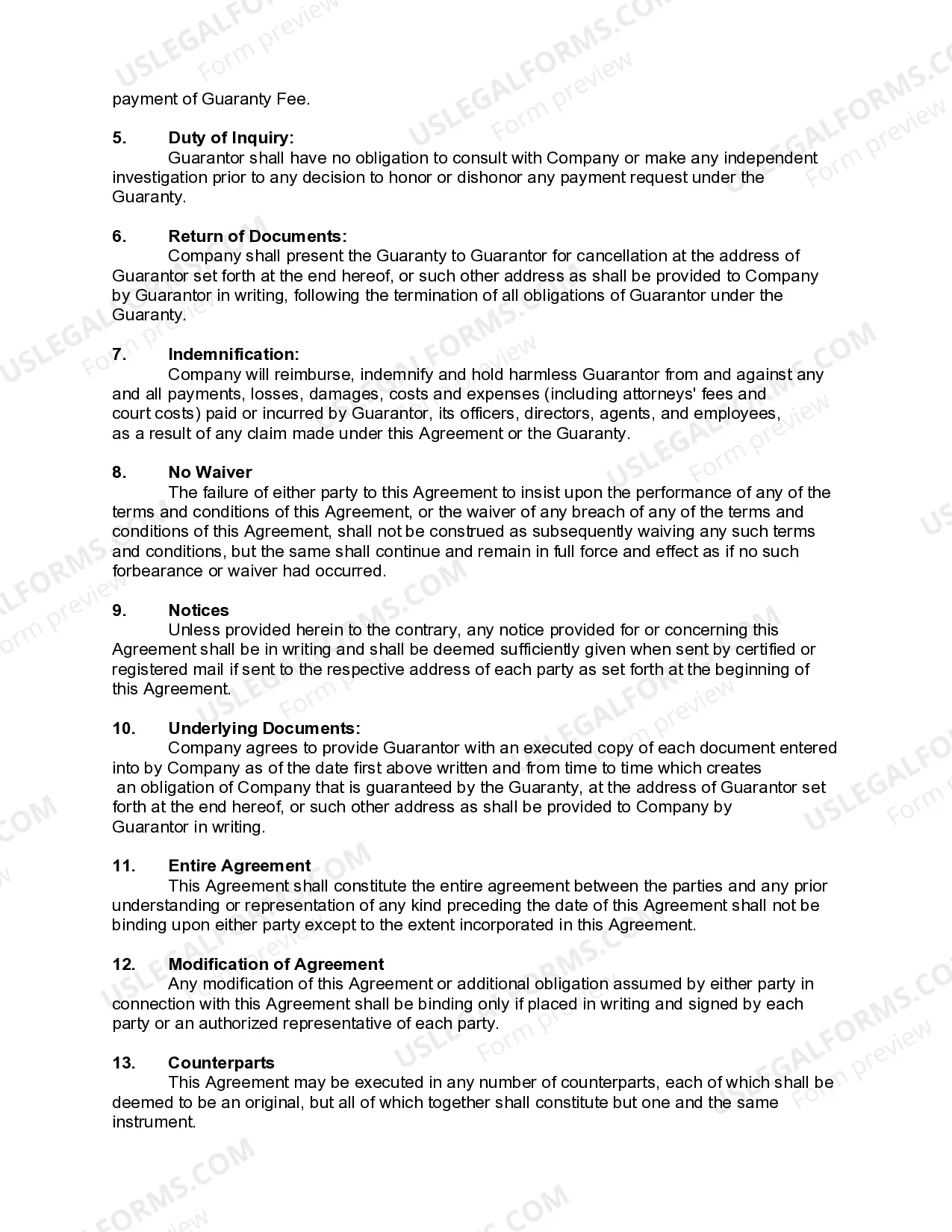

In this agreement, one corporation (the Guarantor) is providing financial assistance to another Corporation (the Corporation) by guaranteeing certain indebtedness for the Company in exchange for a guaranty fee.

This form is a generic example that may be referred to when preparing such a form for your particular state. It is for illustrative purposes only. Local laws should be consulted to determine any specific requirements for such a form in a particular jurisdiction.

A South Carolina Financial Support Agreement — Guaranty of Obligation is a legally binding contract signed between two parties, typically a lender and a guarantor, to provide financial support and ensure the repayment of an obligation. Keywords: South Carolina, Financial Support Agreement, Guaranty of Obligation, contract, lender, guarantor, financial support, repayment. This agreement acts as a form of security for the lender, guaranteeing that the obligations outlined in another contractual arrangement will be fulfilled. The guarantor agrees to become legally liable for the debts or financial obligations of the borrower in case of default or non-payment. There are several types of South Carolina Financial Support Agreements — Guaranty of Obligation, depending on the nature and purpose of the agreement: 1. Personal Guaranty: This type of agreement involves an individual acting as the guarantor, personally guaranteeing the obligations of a borrower. The guarantor's personal assets may be used to cover any outstanding debt if the borrower defaults. 2. Corporate Guaranty: In this case, a company or corporation assumes the role of the guarantor, agreeing to be responsible for the borrower's obligations. This type of agreement is commonly used when a business entity seeks financial assistance from a lender. 3. Limited Guaranty: A limited guaranty restricts the guarantor's liability to a specific amount or set of conditions. The guarantor is only responsible for a portion of the obligation, such as a fixed sum or a predetermined percentage. This type of agreement helps mitigate risk for the guarantor. 4. Continuing Guaranty: A continuing guaranty is an agreement that extends beyond a single transaction or obligation. It provides ongoing support to the borrower for multiple debts or future obligations. The guarantor's liability remains in effect until the agreement is terminated or the borrowing relationship is concluded. 5. Absolute Guaranty: An absolute guaranty places the guarantor in a position of unconditional responsibility for the borrower's obligations. Irrespective of any defenses or disputes the borrower may have, the guarantor is obliged to fulfill the financial obligations as outlined. It is important for all parties involved to carefully review and understand the terms and conditions of a South Carolina Financial Support Agreement — Guaranty of Obligation before signing. Seeking legal counsel is advised to ensure compliance and protection of the rights and responsibilities of both the lender and guarantor.