This form is a type of asset-financing arrangement in which a company uses its receivables (money owed by customers) as collateral in a financing agreement. The company receives an amount that is equal to a reduced value of the receivables pledged. The age of the receivables have a large effect on the amount a company will receive. The older the receivables, the less the company can expect.

This type of financing helps companies free up capital that is stuck in accounts receivables. Accounts receivable financing transfers the default risk associated with the accounts receivables to the financing company. This transfer of risk can help the company using the financing to shift focus from trying to collect receivables to current business activities.

This form is a generic example that may be referred to when preparing such a form for your particular state. It is for illustrative purposes only. Local laws should be consulted to determine any specific requirements for such a form in a particular jurisdiction.

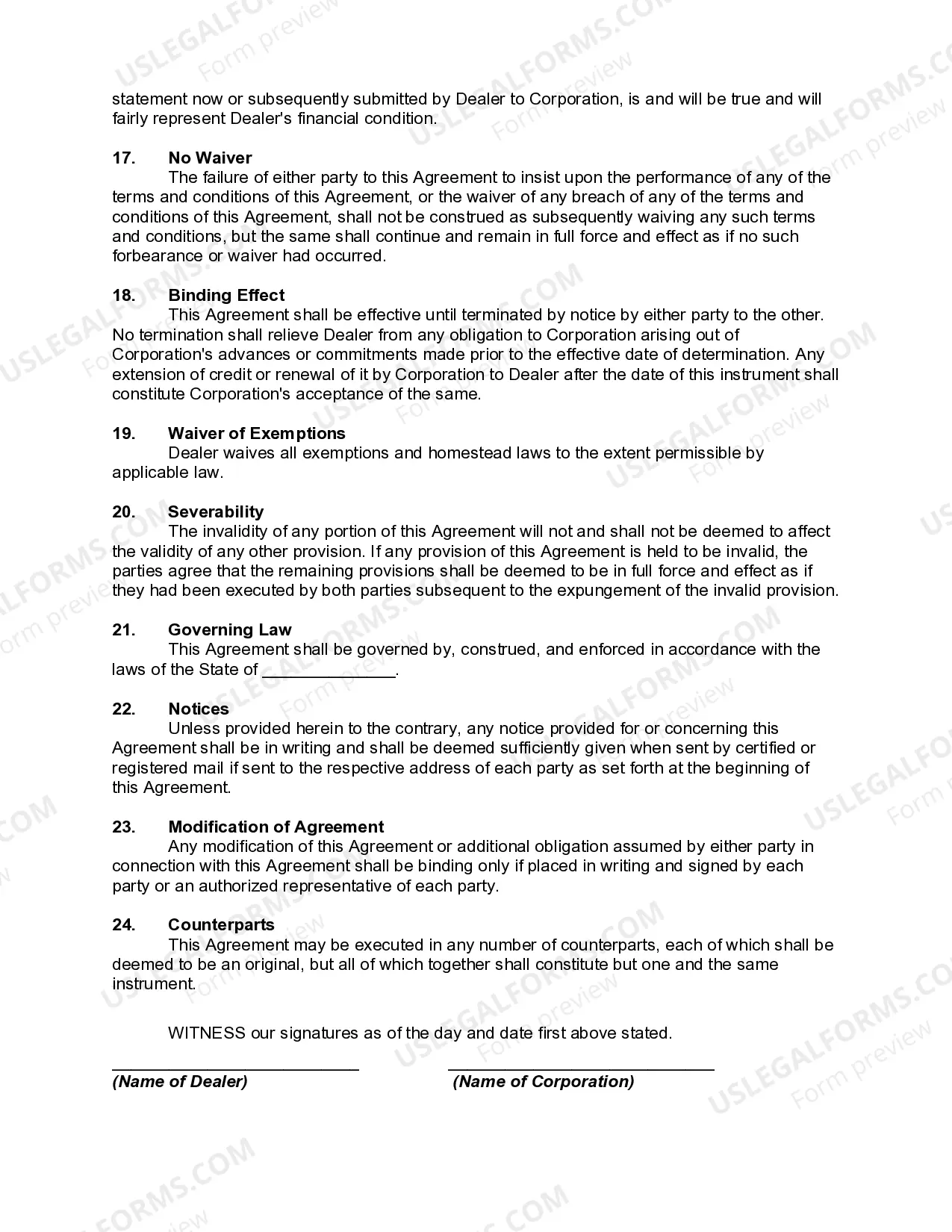

A South Carolina Financing Agreement between a Dealer and a Credit Corporation for Wholesale Financing with Security interest in Accounts and General Intangibles is a legally binding contract that outlines the terms and conditions for the dealer to obtain financing from the credit corporation for the purpose of purchasing and selling goods on a wholesale basis. This type of financing agreement is commonly used in the automotive industry, where dealerships need funds to purchase inventory from manufacturers and sell them to customers. It allows dealers to access capital quickly and efficiently, enabling them to expand their inventory and meet customer demand without having to tie up their own working capital. The agreement typically includes detailed provisions regarding the financing terms, including the amount and duration of the financing, interest rates, repayment schedule, and any fees or charges associated with the financing. It also establishes a security interest in the dealer's accounts and general intangibles, which serves as collateral for the credit corporation in case of default. Under this agreement, the dealer grants the credit corporation a security interest in its accounts, which refers to the money owed to the dealer by its customers for the products sold. Additionally, general intangibles refer to any other intangible assets owned by the dealer, such as intellectual property rights or contracts. By establishing a security interest, the credit corporation can claim the accounts and general intangibles in the event of default, providing a way for them to recoup their investment. This security interest is commonly created through the execution of a UCC-1 financing statement, which is filed with the appropriate state government agency to provide notice to other parties of the credit corporation's claim. Different types of South Carolina Financing Agreements between Dealer and Credit Corporation for Wholesale Financing with Security interest in Accounts and General Intangibles may include variations in terms and conditions to cater to specific needs or requirements of the parties involved. Some specific types may include: 1. Floor Plan Financing Agreement: This type of agreement is specifically designed for dealerships that require financing to purchase and maintain a floor plan inventory of vehicles. The credit corporation provides funding to cover the dealer's inventory expenses, and the dealer repays the borrowed amount as the vehicles are sold. 2. Equipment Financing Agreement: This agreement focuses on financing the purchase of specific equipment or machinery required by the dealer. It may include provisions for maintenance, leasing, or upgrading of the equipment during the financing period. 3. Inventory Financing Agreement: This type of agreement is tailored for dealerships looking to finance their entire inventory rather than specific items. It enables the dealer to obtain funding for a broad range of products and covers the cost of purchasing, storing, and selling the inventory. In conclusion, a South Carolina Financing Agreement between a Dealer and a Credit Corporation for Wholesale Financing with Security interest in Accounts and General Intangibles is a vital tool that enables dealerships to access capital for purchasing inventory and expanding their operations. It ensures that both parties are protected through clear terms and conditions and establishes a security interest in the dealer's accounts and general intangibles. Different types of agreements may exist to meet specific financing requirements of dealerships in South Carolina.A South Carolina Financing Agreement between a Dealer and a Credit Corporation for Wholesale Financing with Security interest in Accounts and General Intangibles is a legally binding contract that outlines the terms and conditions for the dealer to obtain financing from the credit corporation for the purpose of purchasing and selling goods on a wholesale basis. This type of financing agreement is commonly used in the automotive industry, where dealerships need funds to purchase inventory from manufacturers and sell them to customers. It allows dealers to access capital quickly and efficiently, enabling them to expand their inventory and meet customer demand without having to tie up their own working capital. The agreement typically includes detailed provisions regarding the financing terms, including the amount and duration of the financing, interest rates, repayment schedule, and any fees or charges associated with the financing. It also establishes a security interest in the dealer's accounts and general intangibles, which serves as collateral for the credit corporation in case of default. Under this agreement, the dealer grants the credit corporation a security interest in its accounts, which refers to the money owed to the dealer by its customers for the products sold. Additionally, general intangibles refer to any other intangible assets owned by the dealer, such as intellectual property rights or contracts. By establishing a security interest, the credit corporation can claim the accounts and general intangibles in the event of default, providing a way for them to recoup their investment. This security interest is commonly created through the execution of a UCC-1 financing statement, which is filed with the appropriate state government agency to provide notice to other parties of the credit corporation's claim. Different types of South Carolina Financing Agreements between Dealer and Credit Corporation for Wholesale Financing with Security interest in Accounts and General Intangibles may include variations in terms and conditions to cater to specific needs or requirements of the parties involved. Some specific types may include: 1. Floor Plan Financing Agreement: This type of agreement is specifically designed for dealerships that require financing to purchase and maintain a floor plan inventory of vehicles. The credit corporation provides funding to cover the dealer's inventory expenses, and the dealer repays the borrowed amount as the vehicles are sold. 2. Equipment Financing Agreement: This agreement focuses on financing the purchase of specific equipment or machinery required by the dealer. It may include provisions for maintenance, leasing, or upgrading of the equipment during the financing period. 3. Inventory Financing Agreement: This type of agreement is tailored for dealerships looking to finance their entire inventory rather than specific items. It enables the dealer to obtain funding for a broad range of products and covers the cost of purchasing, storing, and selling the inventory. In conclusion, a South Carolina Financing Agreement between a Dealer and a Credit Corporation for Wholesale Financing with Security interest in Accounts and General Intangibles is a vital tool that enables dealerships to access capital for purchasing inventory and expanding their operations. It ensures that both parties are protected through clear terms and conditions and establishes a security interest in the dealer's accounts and general intangibles. Different types of agreements may exist to meet specific financing requirements of dealerships in South Carolina.