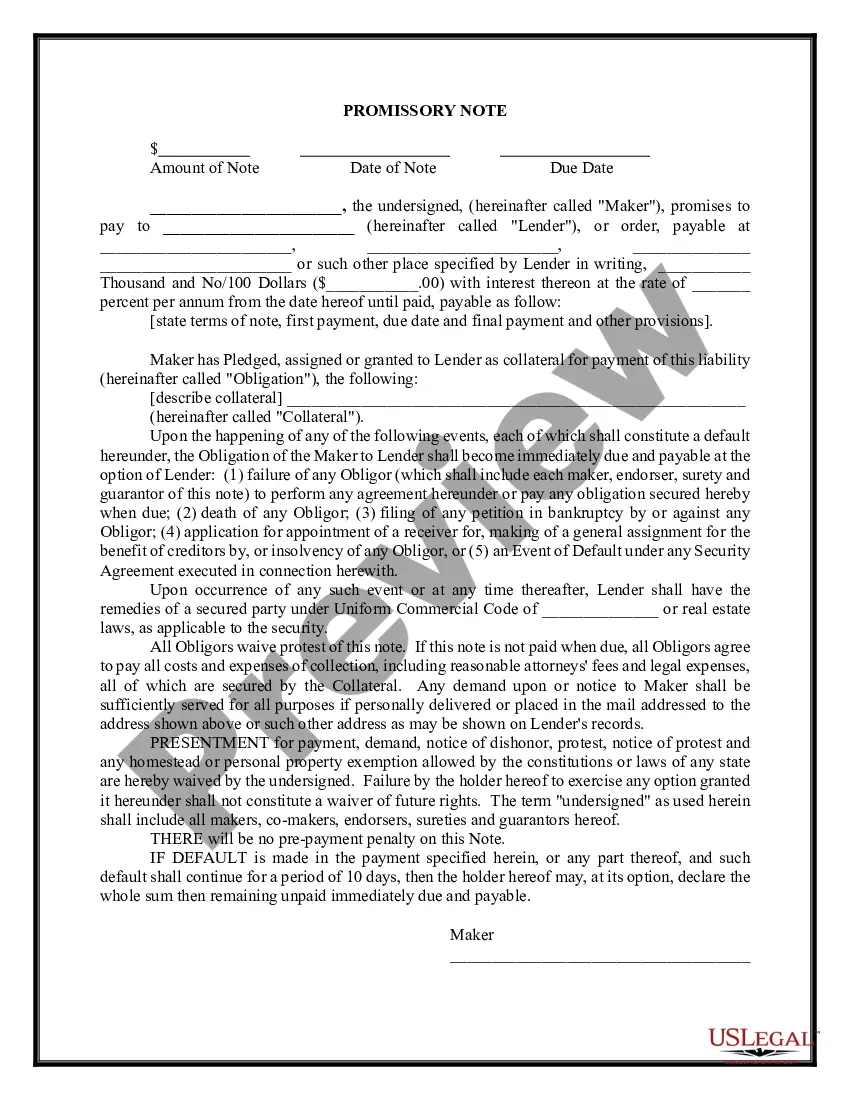

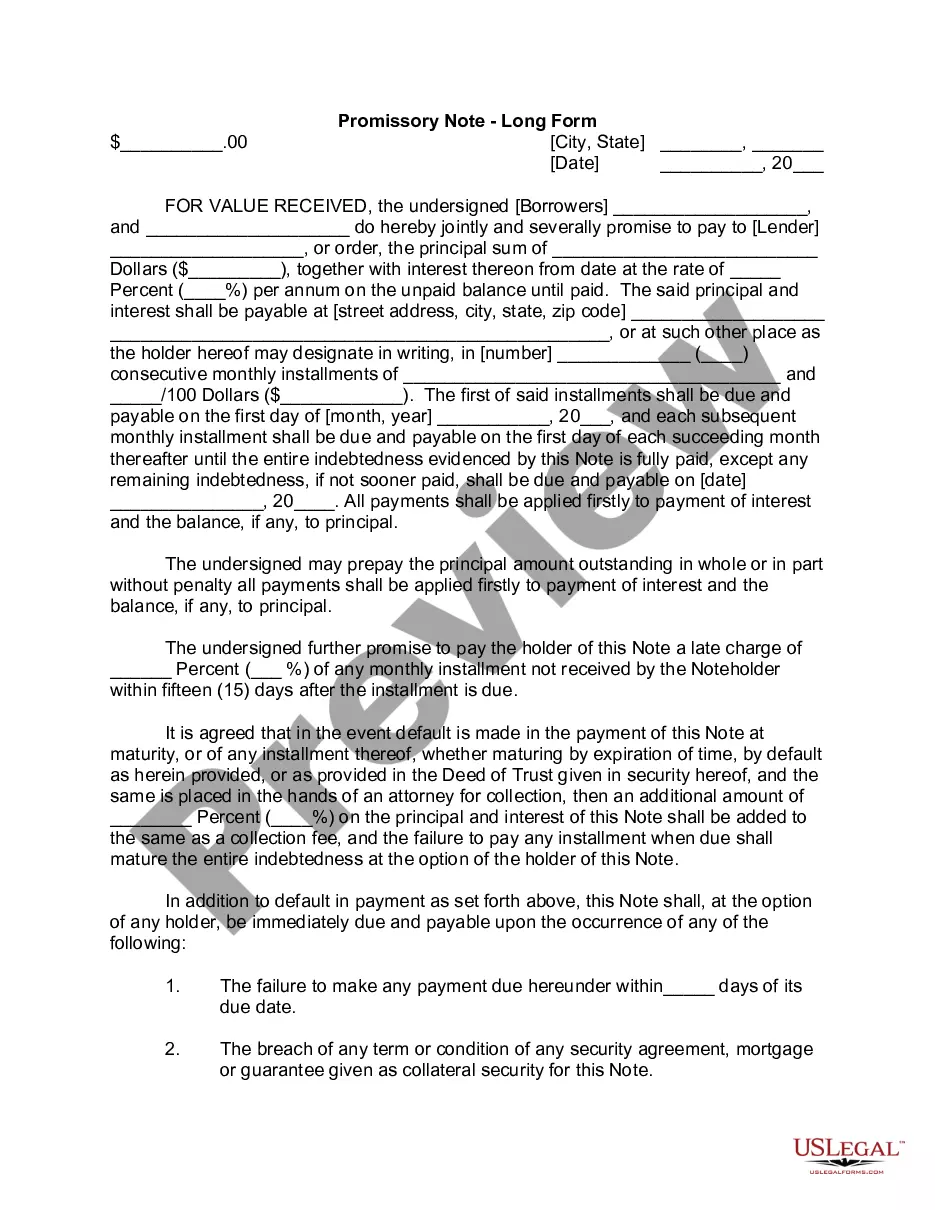

A promissory note is a written promise to pay a debt. An unconditional promise to pay on demand or at a fixed or determined future time a particular sum of money to or to the order of a specified person or to the bearer.

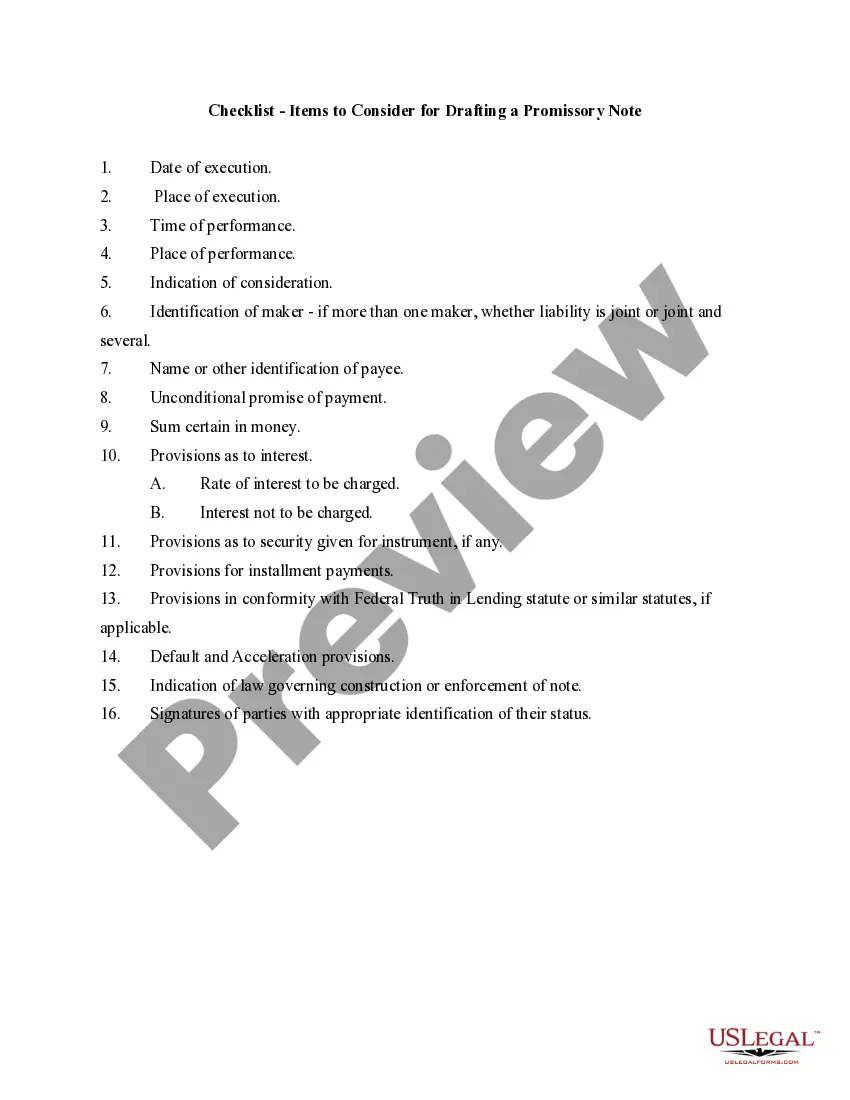

South Carolina Checklist - Items to Consider for Drafting a Promissory Note

Category:

State:

Multi-State

Control #:

US-03060BG

Format:

Word;

Rich Text

Instant download

Description

How to fill out Checklist - Items To Consider For Drafting A Promissory Note?

US Legal Forms - one of the largest collections of legal documents in the United States - provides a variety of legal template documents that you can download or print.

By using the website, you can access thousands of forms for business and personal purposes, organized by categories, states, or keywords.

You can find the latest versions of forms like the South Carolina Checklist - Items to Consider for Drafting a Promissory Note in just seconds.

Review the form description to make sure you have chosen the right one.

If the form does not meet your needs, use the Search field at the top of the screen to find one that does.

- If you already have an account, Log In and download the South Carolina Checklist - Items to Consider for Drafting a Promissory Note from your US Legal Forms account.

- The Download button will appear on each form you view.

- You can access all previously saved forms in the My documents section of your profile.

- If you are using US Legal Forms for the first time, here are simple steps to get started.

- Ensure you have selected the correct form for your specific city/county.

- Preview the form to review its contents.

Form popularity

FAQ

A required element of a valid promissory note is the promise to repay the specified amount. This key component ensures that both parties understand their obligations under the agreement. To assist you in identifying all required elements, our South Carolina Checklist - Items to Consider for Drafting a Promissory Note serves as a useful guide.

Yes, consideration is necessary for a promissory note to be legally enforceable. This means that something of value must be exchanged between the borrower and lender. By following the South Carolina Checklist - Items to Consider for Drafting a Promissory Note, you can ensure that you include adequate consideration, making your note valid and binding.

To ensure a promissory note is valid, it must meet certain requirements. It should involve a clear agreement between the borrower and lender, specifying the amount and terms. Importantly, the note must be signed by the maker to indicate acceptance. For a deeper understanding, check the South Carolina Checklist - Items to Consider for Drafting a Promissory Note and ensure you meet all legal standards.

A promissory note is a legal document that includes several essential elements. First, it must clearly state the amount owed, known as the principal. Second, it should include the interest rate and payment terms. Lastly, both the lender and borrower should sign the document. For more details, consult the South Carolina Checklist - Items to Consider for Drafting a Promissory Note.

Examples of promissory notes range from personal loans between friends to formal agreements for mortgages and student loans. Each type may vary based on the specific terms agreed upon by the parties involved. Reviewing the South Carolina Checklist - Items to Consider for Drafting a Promissory Note can guide you through creating a suitable promissory note for your specific needs.

A promissory note should include the names of all parties involved, the principal amount borrowed, the interest rate, and the repayment schedule. Also, specify the consequences of late payments and default conditions. Using the South Carolina Checklist - Items to Consider for Drafting a Promissory Note will help you create a comprehensive document that protects both parties.

Certain essential elements must always be present in a promissory note to make it enforceable. These include the names and addresses of both parties, the amount owed, the interest rate, and the repayment schedule. Additionally, including a maturity date clarifies when payment is due. Utilize the South Carolina Checklist - Items to Consider for Drafting a Promissory Note to ensure you include everything necessary.

To ensure your promissory note meets legal standards in South Carolina, it must include key elements such as the borrower’s and lender’s details, the principal amount, interest rate, and repayment terms. It is also helpful to specify whether collateral backs the note. To assist you, the South Carolina Checklist - Items to Consider for Drafting a Promissory Note provides handy guidelines on forming your document correctly.

In South Carolina, a promissory note does not legally require notarization to be valid. However, having a notary public witness the signing can strengthen the document’s enforceability in court. This is particularly useful if you ever need to prove the note’s authenticity down the line. For a comprehensive understanding, refer to the South Carolina Checklist - Items to Consider for Drafting a Promissory Note.