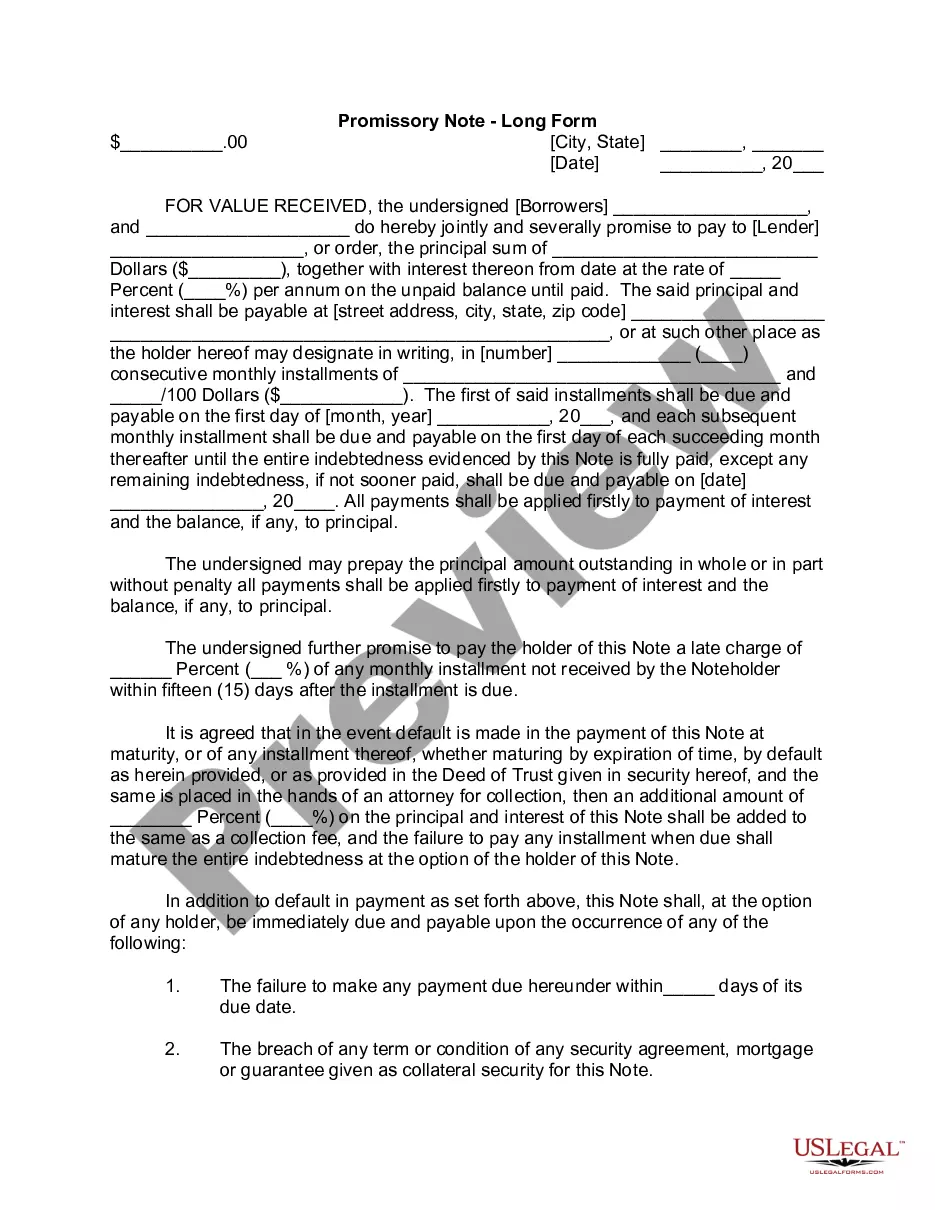

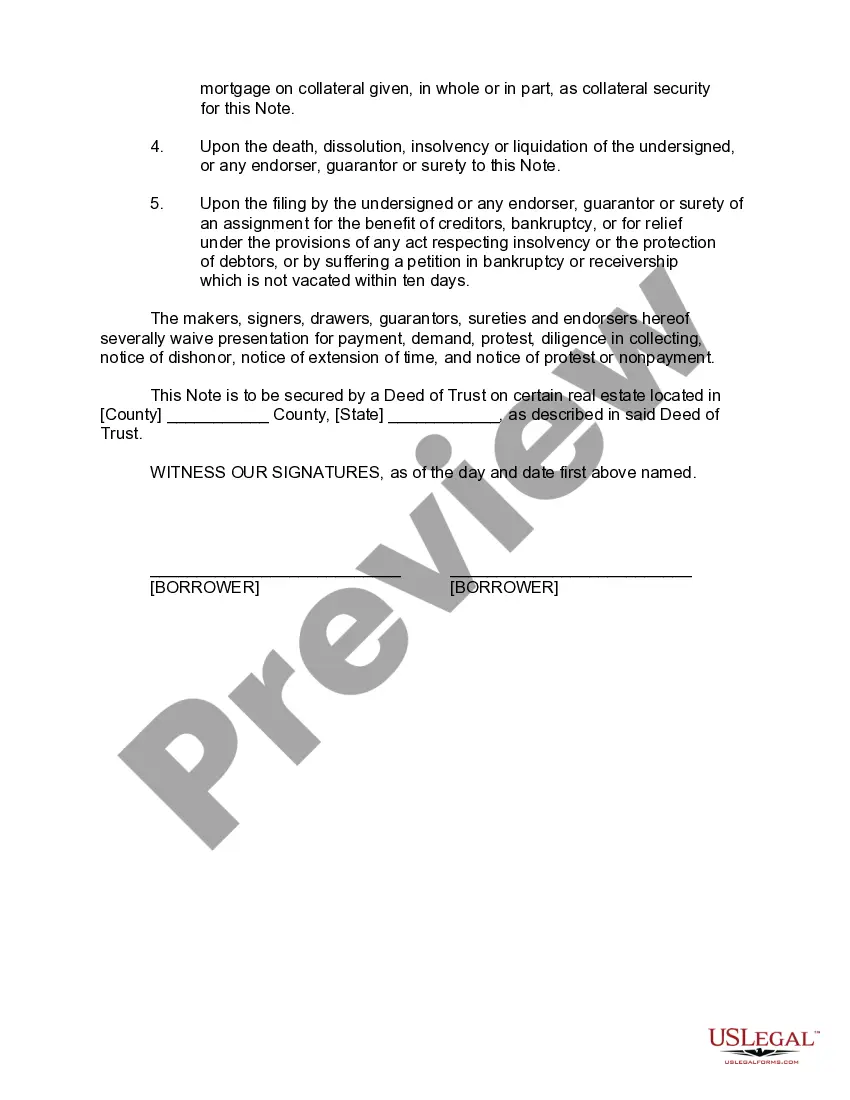

A South Carolina Promissory Note — Long Form is a legally binding document that outlines the terms and conditions of a loan agreement between a lender and a borrower. It serves as evidence of the debt and specifies the repayment terms, including the principal amount, interest rate, repayment schedule, and any additional fees or penalties. In South Carolina, there are various types of Promissory Notes available, each suited for different purposes and situations. Some common types include: 1. Traditional Promissory Note: This is the most common type of Promissory Note used for general personal or business loans. It outlines the terms of the loan, including the amount borrowed, interest rate, repayment schedule, and any collateral involved. 2. Secured Promissory Note: This type of note includes an additional level of security for the lender, as it requires the borrower to pledge collateral in case of default. The collateral can be any valuable asset, such as real estate, vehicles, or investments, which the lender can seize to recover the debt. 3. Unsecured Promissory Note: Unlike a secured note, this type of promissory note doesn't require collateral from the borrower. Therefore, it poses a greater risk to lenders, but it is commonly used for smaller loans or when the borrower doesn't have sufficient assets to pledge as collateral. 4. Demand Promissory Note: This note allows the lender to demand immediate repayment of the full loan amount at any time without providing a specific repayment schedule. It provides flexibility to lenders when they require immediate access to the funds. 5. Installment Promissory Note: This type of note specifies a fixed repayment schedule, usually in monthly installments, until the debt is fully repaid. It outlines the principal amount, interest rate, duration of the repayment period, and the amount due for each installment. 6. Balloon Promissory Note: A balloon note is structured so that the borrower makes lower monthly payments for a specific period, and a large lump sum payment (the balloon payment) becomes due at the end of the term. This type of note is often used for real estate loans or when refinancing existing loans. When preparing a South Carolina Promissory Note — Long Form, it is essential to include all the necessary details accurately and clearly. Both parties (lender and borrower) should review the document carefully to ensure everyone's rights and obligations are properly documented and protected. It is crucial to consult with a legal professional to draft a Promissory Note tailored to the specific needs of the parties involved and compliant with South Carolina's laws and regulations.

South Carolina Promissory Note - Long Form

Description

How to fill out South Carolina Promissory Note - Long Form?

If you wish to comprehensive, acquire, or print authorized papers themes, use US Legal Forms, the most important collection of authorized kinds, that can be found online. Use the site`s simple and easy practical search to find the documents you need. Various themes for business and individual reasons are sorted by types and states, or keywords and phrases. Use US Legal Forms to find the South Carolina Promissory Note - Long Form in a few clicks.

In case you are already a US Legal Forms buyer, log in for your accounts and click the Acquire switch to obtain the South Carolina Promissory Note - Long Form. You can even accessibility kinds you in the past downloaded from the My Forms tab of your own accounts.

Should you use US Legal Forms for the first time, refer to the instructions beneath:

- Step 1. Be sure you have selected the form to the correct city/country.

- Step 2. Make use of the Review solution to look over the form`s content material. Never overlook to read the information.

- Step 3. In case you are not satisfied with all the kind, use the Lookup area on top of the display to locate other models of your authorized kind web template.

- Step 4. Upon having found the form you need, click the Acquire now switch. Opt for the costs prepare you prefer and put your credentials to sign up for the accounts.

- Step 5. Method the financial transaction. You should use your charge card or PayPal accounts to finish the financial transaction.

- Step 6. Pick the format of your authorized kind and acquire it on your device.

- Step 7. Total, change and print or signal the South Carolina Promissory Note - Long Form.

Each authorized papers web template you get is the one you have permanently. You might have acces to every single kind you downloaded with your acccount. Go through the My Forms area and select a kind to print or acquire once again.

Compete and acquire, and print the South Carolina Promissory Note - Long Form with US Legal Forms. There are thousands of specialist and condition-specific kinds you may use to your business or individual requires.