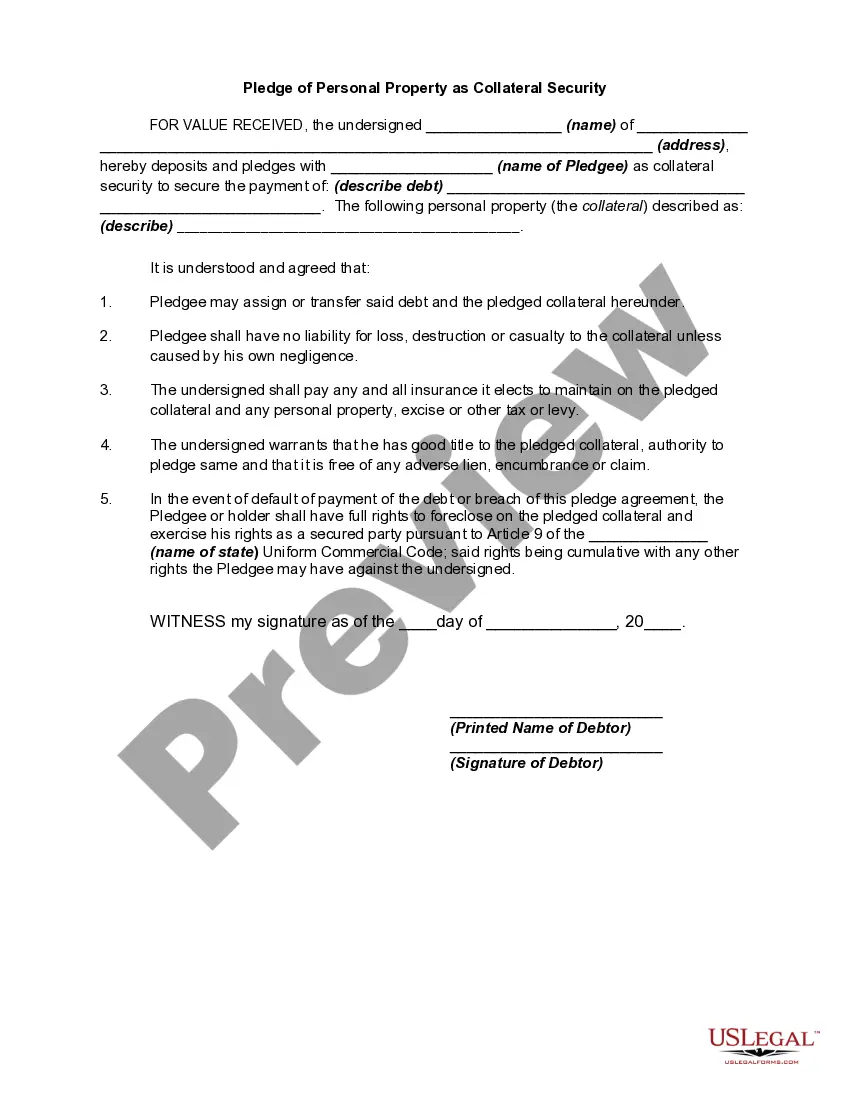

The South Carolina Pledge of Personal Property as Collateral Security is an important legal concept that pertains to the use of personal property as collateral for securing loans or debts in the state of South Carolina. This agreement allows individuals and businesses to pledge their personal property as security to obtain financing from a lender while maintaining ownership and possession of said property. Under this pledge, the borrower (known as the pledge) transfers the right to use the personal property to the lender (known as the pledge) as collateral until the loan or debt is repaid in full. This arrangement provides assurance to the lender that if the borrower fails to fulfill their financial obligations, the lender has the right to claim and sell the pledged property to recover the outstanding debt. The South Carolina Pledge of Personal Property as Collateral Security is governed by statutes and regulations that outline the rights and responsibilities of both parties involved. It is crucial for both the pledge and the pledge to draft a detailed pledge agreement that clearly defines the terms and conditions, including the description of the collateral, its value, any maintenance or custody requirements, and the consequences of default. There are different types of South Carolina Pledge of Personal Property as Collateral Security, including: 1. Chattel Mortgage: A common form of pledge where movable personal property, such as vehicles, machinery, or inventory, is pledged as collateral. 2. Security Agreement: Also known as a UCC-1 financing statement, it is a pledge that covers a broad range of personal property assets, including accounts receivable, inventory, equipment, and other tangible or intangible assets. 3. Agricultural Security Agreement: Specifically designed for farmers and agricultural businesses, this pledge allows the use of farm equipment, livestock, crops, and other agricultural-related assets as collateral for securing loans or debts. 4. Intellectual Property Security Agreement: In cases where intellectual property rights, such as patents, trademarks, or copyrights, hold significant value, this type of pledge allows individuals or businesses to use these intangible assets as collateral. 5. Pledge of Personal Property by a Debtor: This type of pledge mainly applies to individuals who use their personal property, such as jewelry, artwork, or collectibles, as collateral to secure personal loans or debts. It is essential to consult with legal professionals and understand the specific requirements and procedures associated with the South Carolina Pledge of Personal Property as Collateral Security. Clear communication, documentation, and compliance with relevant laws and regulations will ensure a smooth and legally binding agreement between all parties involved.

South Carolina Pledge of Personal Property as Collateral Security

Description

How to fill out South Carolina Pledge Of Personal Property As Collateral Security?

You can commit hrs on-line attempting to find the legitimate file design which fits the state and federal requirements you need. US Legal Forms gives a large number of legitimate types that are evaluated by specialists. You can easily acquire or printing the South Carolina Pledge of Personal Property as Collateral Security from my services.

If you already have a US Legal Forms bank account, you may log in and then click the Down load option. Following that, you may comprehensive, edit, printing, or signal the South Carolina Pledge of Personal Property as Collateral Security. Each legitimate file design you purchase is the one you have permanently. To acquire yet another version of the bought form, visit the My Forms tab and then click the corresponding option.

If you use the US Legal Forms website for the first time, keep to the easy recommendations under:

- First, be sure that you have chosen the correct file design to the area/area of your choosing. See the form outline to make sure you have chosen the correct form. If readily available, utilize the Preview option to appear with the file design at the same time.

- In order to discover yet another variation from the form, utilize the Look for discipline to get the design that meets your requirements and requirements.

- Upon having found the design you need, click on Get now to carry on.

- Choose the prices strategy you need, enter your credentials, and sign up for an account on US Legal Forms.

- Full the financial transaction. You may use your Visa or Mastercard or PayPal bank account to pay for the legitimate form.

- Choose the formatting from the file and acquire it to the device.

- Make alterations to the file if necessary. You can comprehensive, edit and signal and printing South Carolina Pledge of Personal Property as Collateral Security.

Down load and printing a large number of file templates while using US Legal Forms site, that provides the most important assortment of legitimate types. Use expert and state-particular templates to handle your company or person demands.