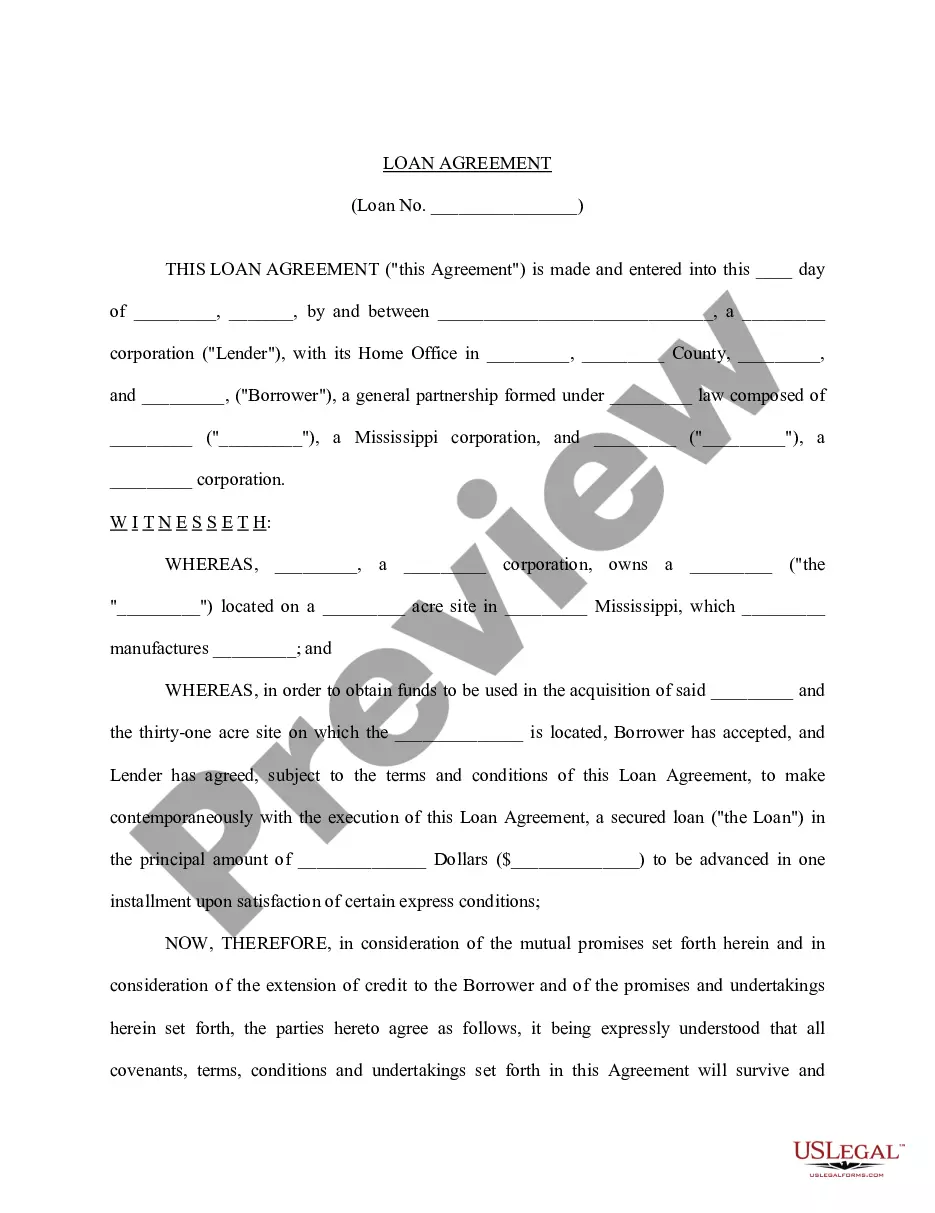

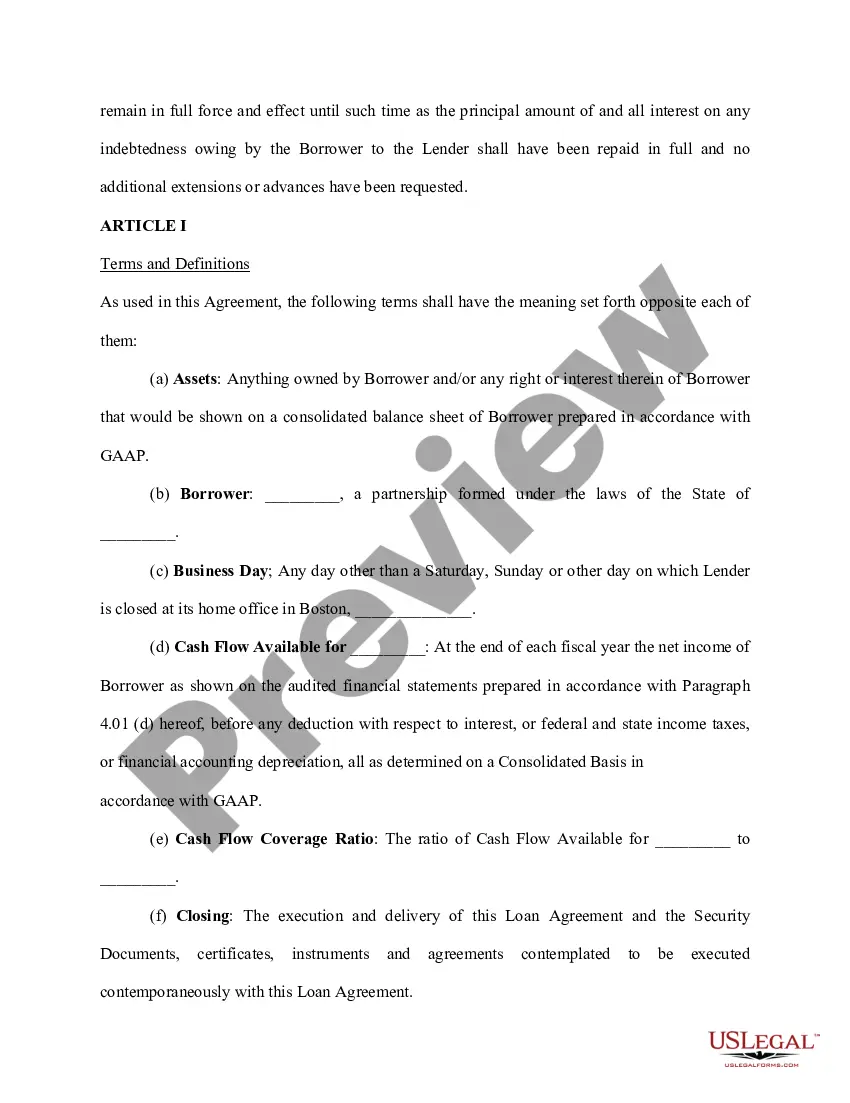

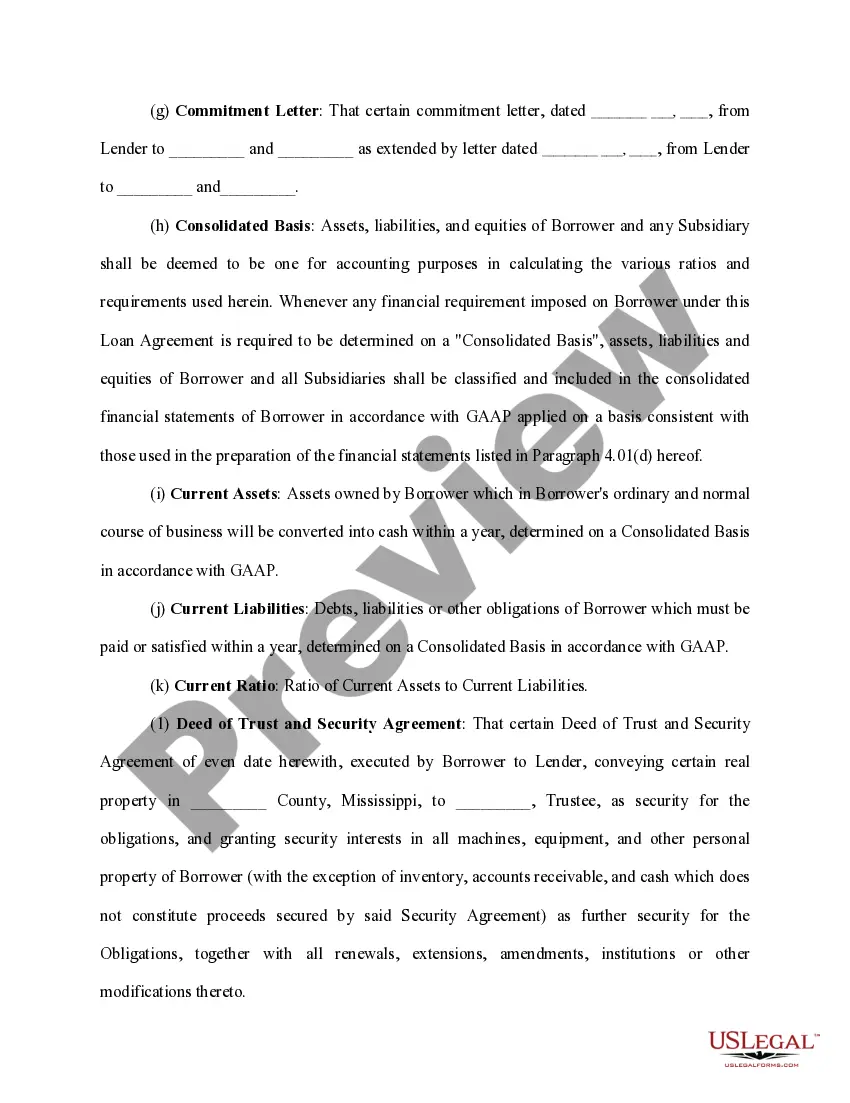

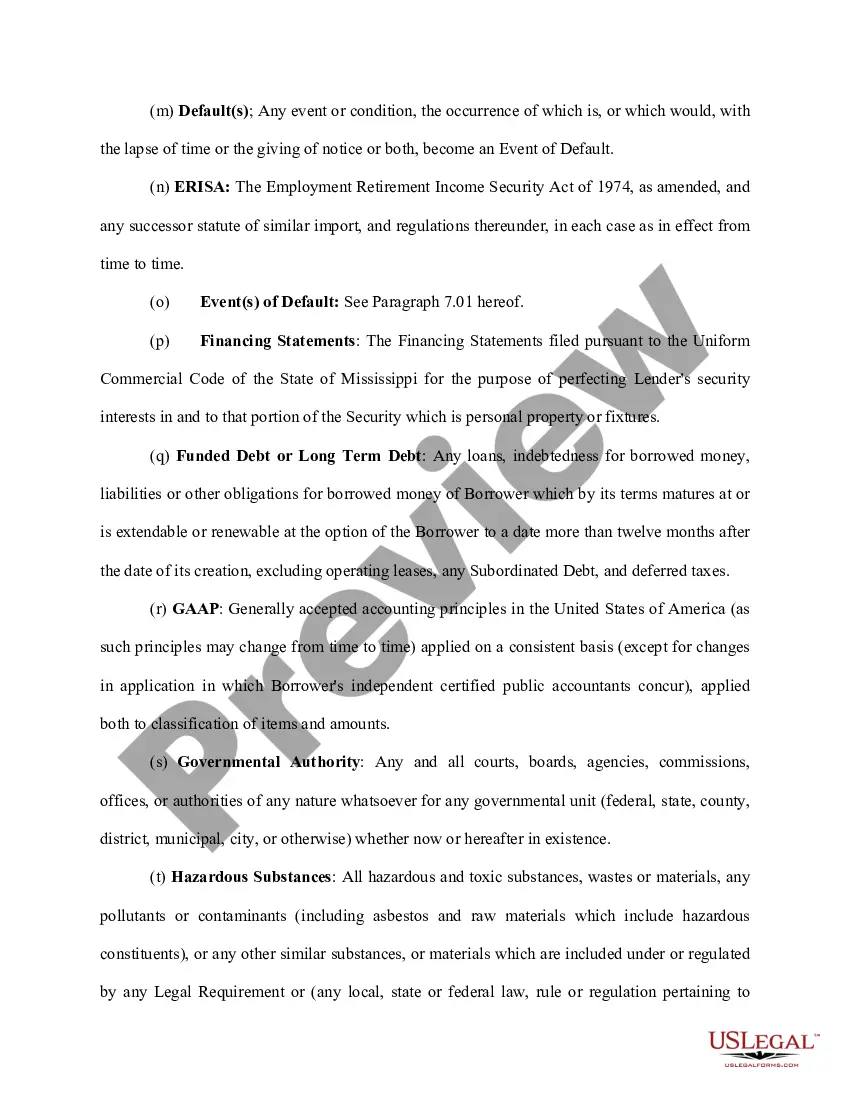

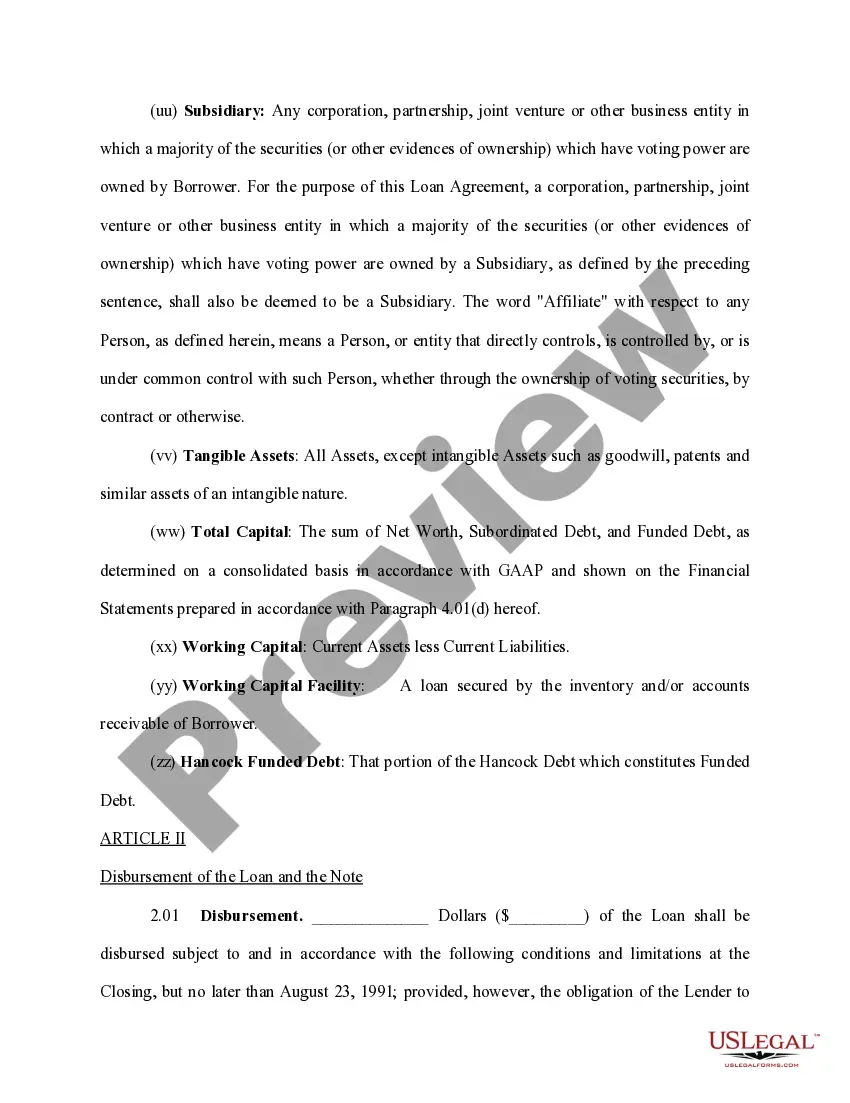

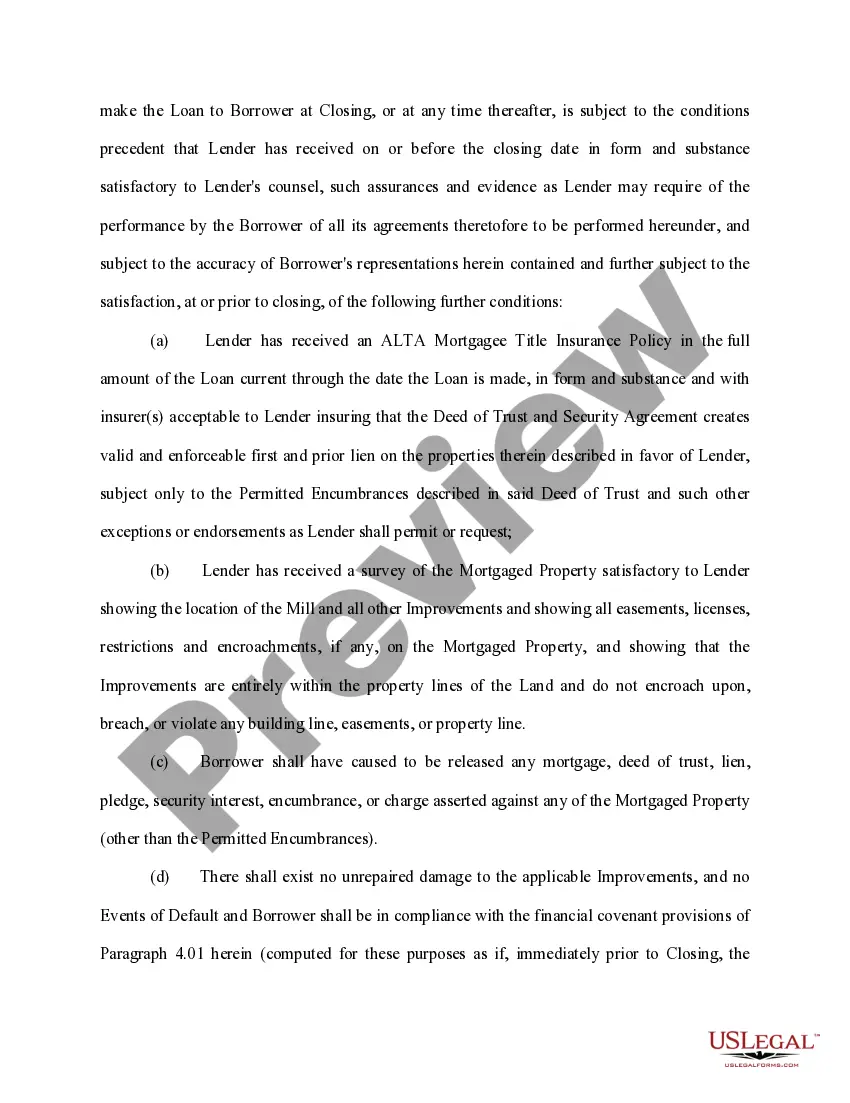

A South Carolina Loan Agreement for Equipment is a legal document that outlines the terms and conditions of a loan specifically for the acquisition or leasing of equipment in the state of South Carolina. This agreement serves as a binding contract between the lender and the borrower and ensures that both parties understand their rights, obligations, and responsibilities throughout the loan term. The South Carolina Loan Agreement for Equipment typically includes the following key components: 1. Parties Involved: The agreement clearly identifies the lender and the borrower, including their legal names, addresses, and contact information. Additionally, it may include information about any third-party guarantors or co-signers, if applicable. 2. Description of Equipment: The agreement provides a detailed and comprehensive description of the equipment being loaned or leased, including any identifying serial numbers, make, model, and condition. This section ensures that both parties are in agreement regarding the specific equipment involved in the loan transaction. 3. Loan Amount and Repayment Terms: The agreement specifies the total loan amount being provided to the borrower, the interest rate (if applicable), and the repayment terms, such as the installment schedule, due dates, and the method of payment. It may also include any late payment penalties or default consequences. 4. Security Agreement: In some cases, the lender may require the borrower to provide collateral or security for the equipment loan. This section outlines the details of the security interest, including the specific equipment pledged as collateral and the procedures for the lender to exercise their rights in case of default. 5. Insurance and Maintenance Responsibilities: The agreement may outline the borrower's obligations to maintain insurance coverage for the equipment, protecting the lender's interests. It may also specify requirements for maintenance and repairs, ensuring that the equipment remains in good working order throughout the loan term. 6. Default and Remedies: This section defines the consequences if either party fails to fulfill their obligations under the agreement. It may include provisions for late payments, default, repossession of the equipment, or legal actions that the lender can pursue to recover the outstanding loan amount. Types of South Carolina Loan Agreements for Equipment can include: 1. Equipment Lease Agreement: This type of agreement allows the borrower to use the equipment for a specified period in exchange for regular lease payments. Ownership of the equipment typically remains with the lender, and the borrower may have the option to purchase the equipment at the end of the lease term. 2. Equipment Financing Agreement: This agreement provides the borrower with a loan specifically for the purpose of acquiring equipment. The borrower takes ownership of the equipment from the beginning, while making installment payments to the lender over a predetermined period. 3. Equipment Security Agreement: This agreement establishes a loan secured by the equipment itself. In the event of default, the lender has the right to repossess and sell the equipment to recover the outstanding loan amount. In conclusion, a South Carolina Loan Agreement for Equipment is a legally binding document that safeguards the interests of both lenders and borrowers in equipment loan or lease transactions. It defines the terms, repayment schedule, and responsibilities of each party, ensuring a transparent and mutually beneficial arrangement.

South Carolina Loan Agreement for Equipment

Description

How to fill out South Carolina Loan Agreement For Equipment?

Finding the right legitimate record format can be a have a problem. Of course, there are a variety of templates available online, but how will you obtain the legitimate type you will need? Use the US Legal Forms internet site. The support provides thousands of templates, for example the South Carolina Loan Agreement for Equipment, that can be used for organization and private requirements. Each of the forms are inspected by pros and meet up with state and federal requirements.

When you are presently signed up, log in for your bank account and then click the Obtain option to get the South Carolina Loan Agreement for Equipment. Utilize your bank account to look throughout the legitimate forms you have purchased in the past. Go to the My Forms tab of your bank account and have an additional backup from the record you will need.

When you are a fresh user of US Legal Forms, here are straightforward instructions that you should follow:

- Initial, ensure you have selected the right type to your town/area. It is possible to examine the shape utilizing the Preview option and browse the shape outline to make certain this is basically the best for you.

- If the type fails to meet up with your preferences, take advantage of the Seach industry to discover the right type.

- Once you are positive that the shape would work, go through the Acquire now option to get the type.

- Opt for the costs plan you would like and enter in the necessary info. Create your bank account and buy an order making use of your PayPal bank account or Visa or Mastercard.

- Select the document file format and down load the legitimate record format for your product.

- Comprehensive, modify and produce and signal the obtained South Carolina Loan Agreement for Equipment.

US Legal Forms may be the largest collection of legitimate forms that you will find numerous record templates. Use the service to down load appropriately-created documents that follow express requirements.