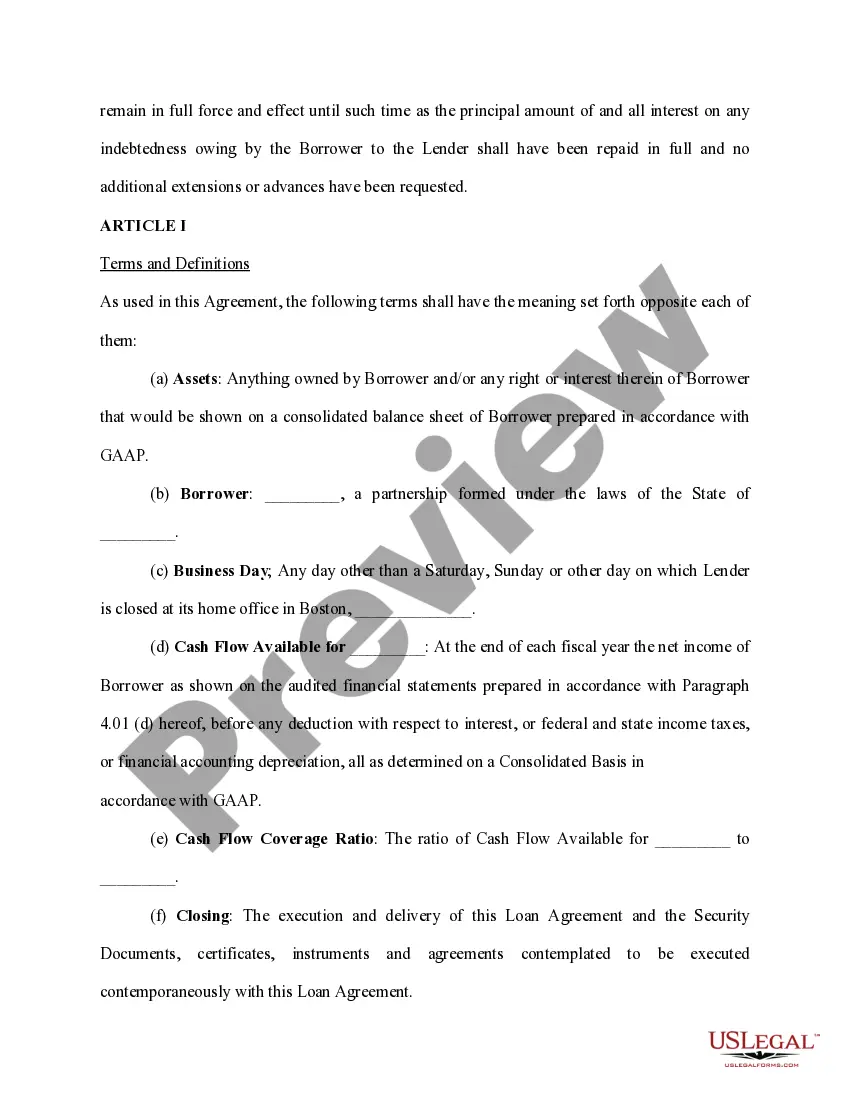

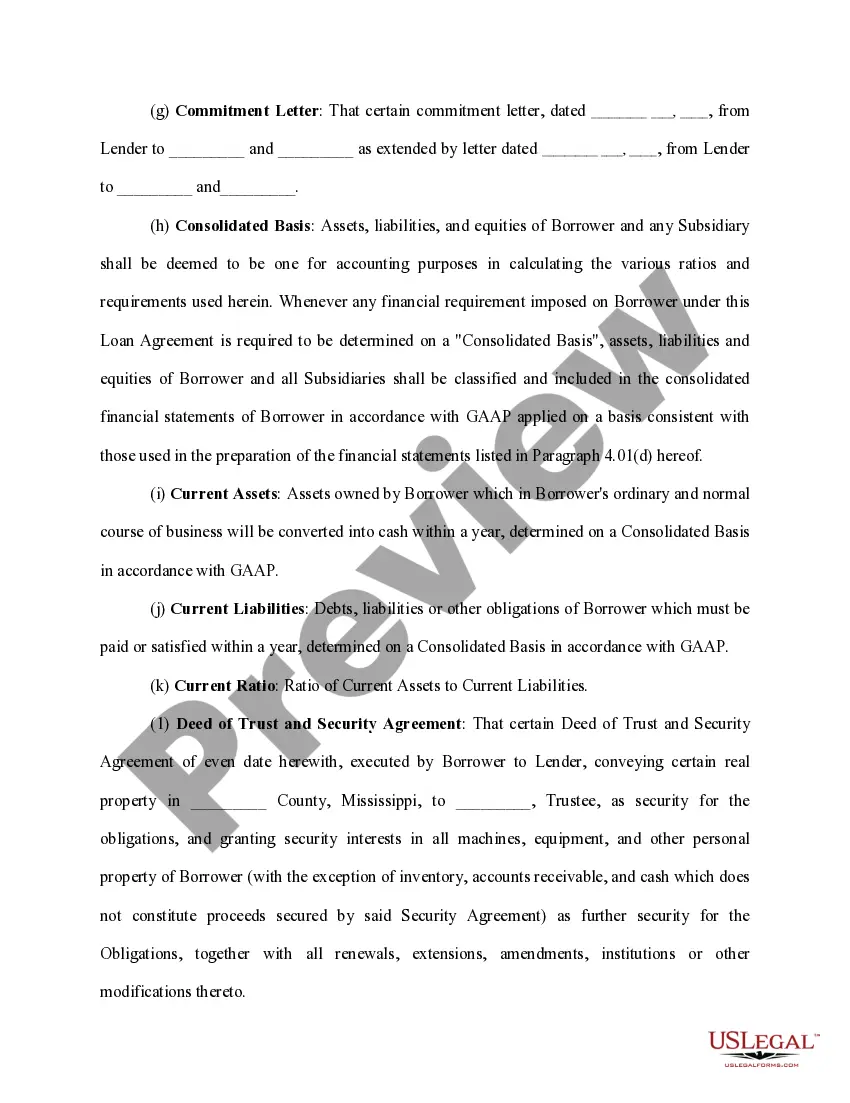

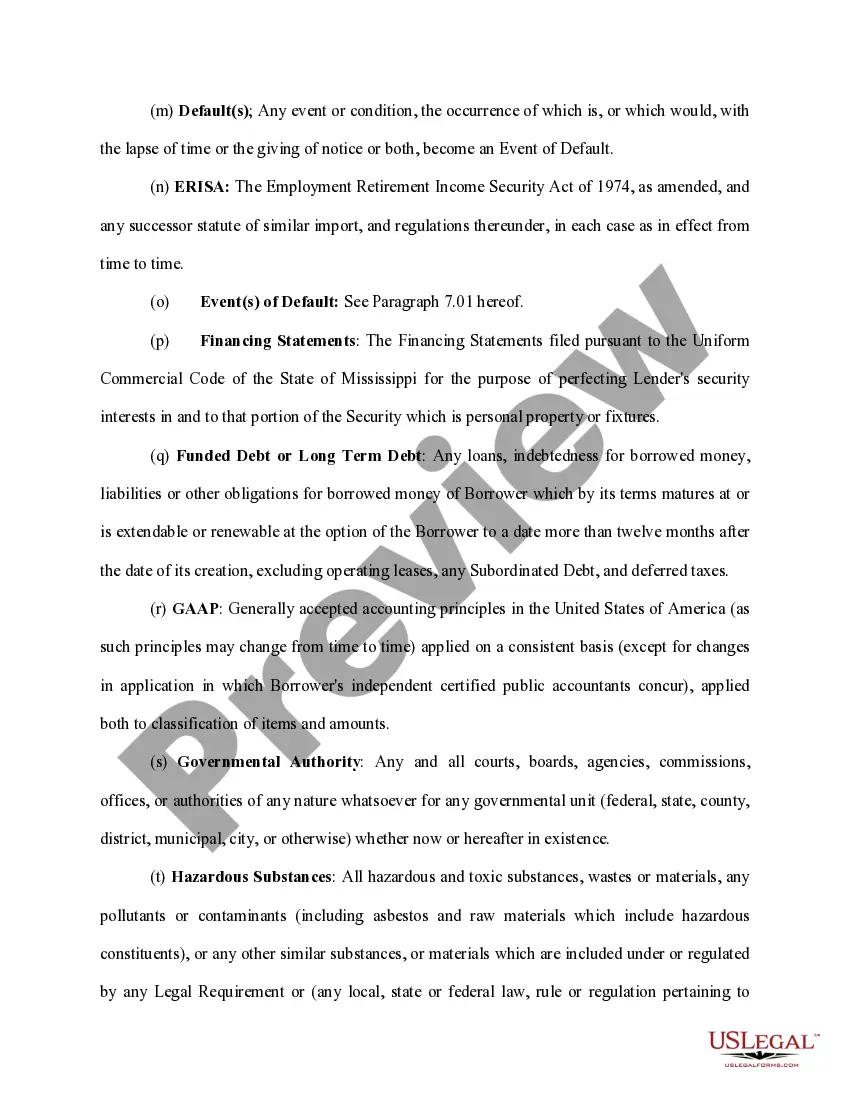

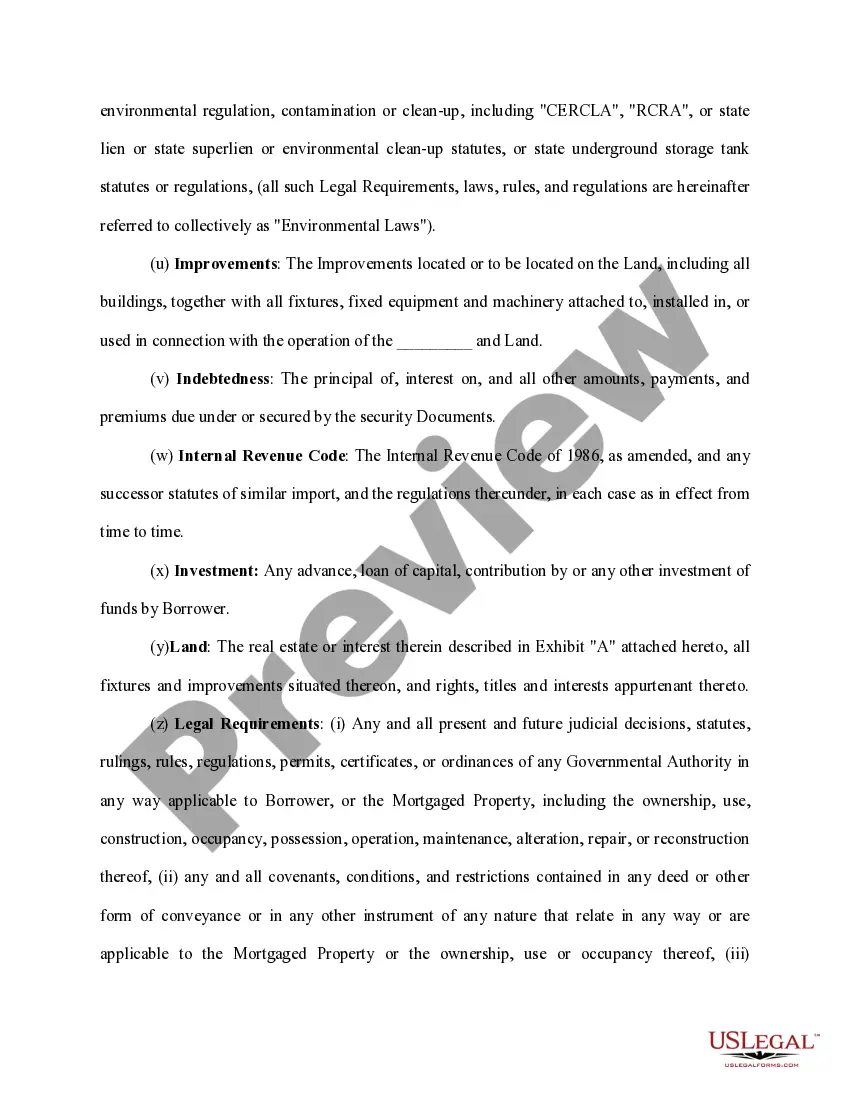

South Carolina Loan Agreement for Vehicle: A Comprehensive Guide Overview: A South Carolina Loan Agreement for Vehicle is a legal contract that outlines the terms and conditions of a loan obtained to finance the purchase of a vehicle. This agreement establishes the rights and responsibilities of both the borrower and lender, ensuring a clear understanding of the loan terms. Different types of loan agreements may exist depending on specific factors such as loan amount, interest rate, and repayment plans. Keywords: South Carolina, Loan Agreement, Vehicle, Types of South Carolina Loan Agreements for Vehicle: 1. Traditional Auto Loan Agreement: The most common type of loan agreement for vehicle purchases, this contract encompasses terms regarding the loan amount, interest rate, repayment schedule, and consequences of default. Borrowers obtain financing from a lender, often a bank or credit union, and repay the loan in installments over an agreed-upon period. 2. Dealership Financing Agreement: This type of loan agreement occurs when the vehicle purchase and financing are both arranged through an authorized dealership. These agreements tend to offer convenience as borrowers can negotiate the terms of the loan and vehicle purchase simultaneously. Dealership financing may involve different lenders, and the terms can vary. 3. Refinancing Loan Agreement: Refinancing allows borrowers to replace their current loan agreement with a new one. This may be beneficial when interest rates decrease, creditworthiness improves, or a better loan opportunity arises. Refinancing can potentially lower monthly payments or reduce the overall cost of the loan. 4. Title Loan Agreement: Title loans involve using the title of a vehicle as collateral for a loan. In South Carolina, title loans are regulated, and specific terms and conditions must be met. These agreements often have higher interest rates and shorter repayment periods, making them suitable for borrowers needing immediate cash but with limited options. Key Elements in a South Carolina Loan Agreement for Vehicle: 1. Parties involved: Identifies the lender (individual or entity providing the loan) and the borrower (individual purchasing the vehicle). 2. Vehicle details: Includes make, model, year, vehicle identification number (VIN), and any specific vehicle conditions or modifications. 3. Loan terms and repayment: Specifies the principal loan amount, interest rate, repayment schedule (monthly, bi-monthly, etc.), due dates, and how payments will be made (e.g., check, electronic transfer). 4. Consequences of default: Outlines the actions the lender can take if the borrower fails to meet the agreed-upon terms, including repossession of the vehicle. 5. Insurance requirements: States the borrower's obligation to maintain comprehensive and collision insurance on the vehicle for the loan's duration. 6. Governing law: Specifies that the loan agreement is subject to South Carolina state laws. Conclusion: A South Carolina Loan Agreement for Vehicle is a legally binding contract that facilitates financing for individuals purchasing a vehicle. Whether obtaining financing through a traditional auto loan, dealership financing, refinancing arrangement, or a title loan, it is essential for borrowers to thoroughly understand the terms and conditions outlined in their loan agreements to ensure a successful and transparent transaction.

South Carolina Loan Agreement for Vehicle

Description

How to fill out South Carolina Loan Agreement For Vehicle?

If you wish to full, down load, or printing lawful record themes, use US Legal Forms, the greatest variety of lawful kinds, which can be found on the web. Make use of the site`s basic and convenient look for to get the documents you want. Different themes for enterprise and individual reasons are categorized by types and claims, or keywords. Use US Legal Forms to get the South Carolina Loan Agreement for Vehicle in just a number of click throughs.

In case you are currently a US Legal Forms customer, log in to the account and click the Acquire button to find the South Carolina Loan Agreement for Vehicle. You may also access kinds you formerly acquired inside the My Forms tab of your own account.

If you work with US Legal Forms the first time, follow the instructions under:

- Step 1. Be sure you have chosen the shape for the correct city/land.

- Step 2. Use the Review method to look through the form`s information. Never neglect to read the information.

- Step 3. In case you are not happy with all the type, utilize the Research field at the top of the screen to locate other types in the lawful type format.

- Step 4. When you have discovered the shape you want, click on the Purchase now button. Choose the prices plan you prefer and put your qualifications to register on an account.

- Step 5. Process the deal. You may use your bank card or PayPal account to finish the deal.

- Step 6. Choose the file format in the lawful type and down load it on your system.

- Step 7. Total, modify and printing or sign the South Carolina Loan Agreement for Vehicle.

Each and every lawful record format you get is the one you have eternally. You might have acces to every type you acquired within your acccount. Go through the My Forms area and select a type to printing or down load yet again.

Remain competitive and down load, and printing the South Carolina Loan Agreement for Vehicle with US Legal Forms. There are millions of skilled and express-specific kinds you can use for your personal enterprise or individual requirements.