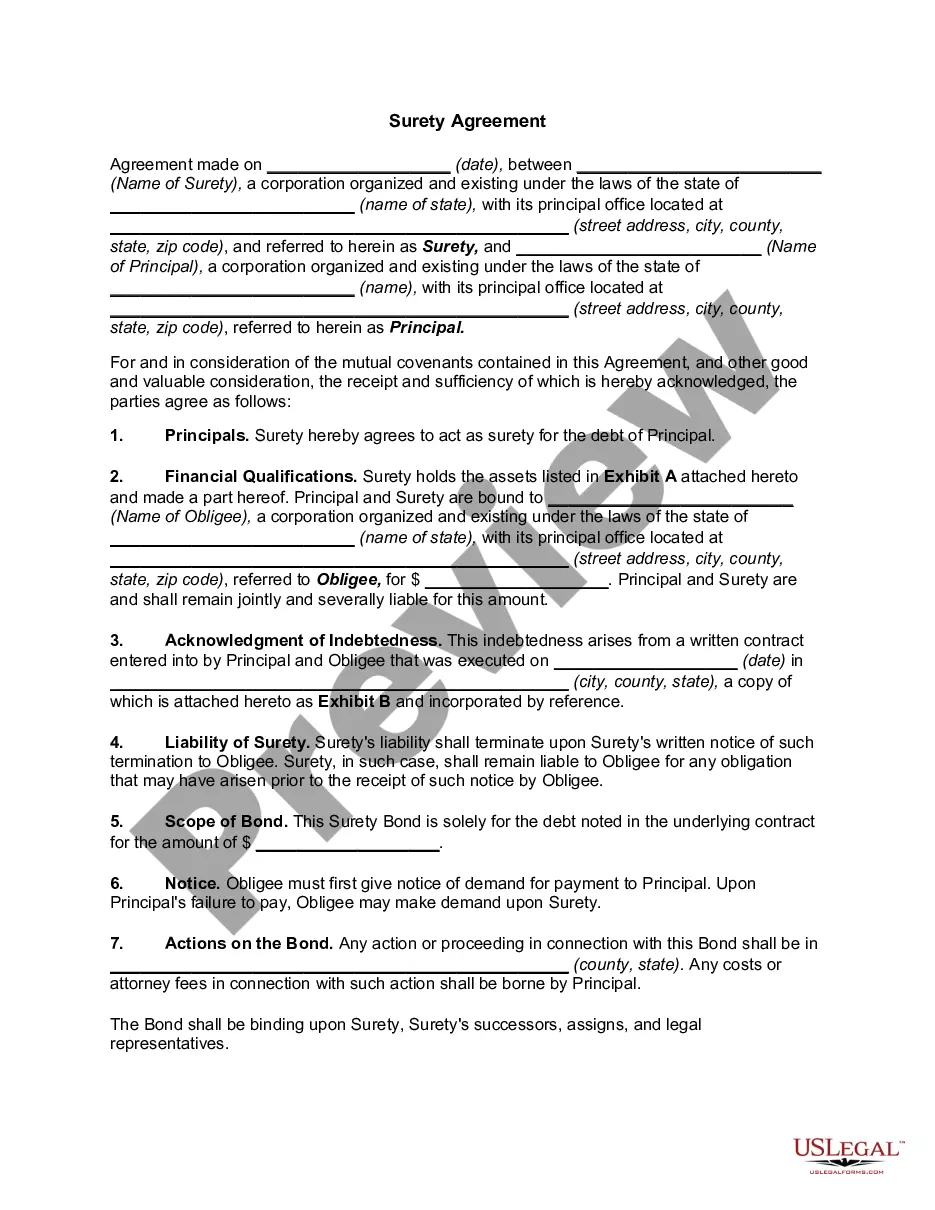

A South Carolina Surety Agreement is a legally binding contract established between three parties: the principal, the obliged, and the surety. It is commonly used in various industries, including construction, to ensure that a project is completed as agreed upon and to protect the obliged's interests. This agreement guarantees that the principal will fulfill their obligations outlined in a separate contract, typically a construction contract, and provides financial security in case the principal fails to meet these obligations. In South Carolina, there are different types of Surety Agreements, each serving a specific purpose: 1. Bid Bond: This type of surety agreement guarantees that the principal, usually a contractor, will honor their bid and enter into a contract if awarded a project. It acts as a safeguard for the project owner, ensuring that the winning bidder will perform the work as proposed in the bid. 2. Performance Bond: A performance bond guarantees the principal's completion of a project according to the terms and conditions set forth in the contract. If the principal fails to fulfill their obligations, the surety will step in and ensure the project is completed or compensate the obliged for any financial loss incurred. 3. Payment Bond: A payment bond protects subcontractors, suppliers, and laborers involved in a construction project by ensuring they are paid for the work or materials provided. In case the principal fails to make the necessary payments, the surety covers the outstanding amount owed to the claimants. 4. Maintenance Bond: This type of surety agreement ensures the principal's workmanship for a specific period after the project's completion. It guarantees that any defects or deficiencies resulting from the principal's work will be rectified at no additional cost to the obliged. These South Carolina Surety Agreements play a vital role in fostering trust and mitigating risks in various contractual relationships. They provide reassurance to project owners or obliges that their investments will be protected and the contractual terms will be upheld. By involving a surety, parties can ensure financial security, facilitate successful project completion, and maintain the integrity of the construction industry in South Carolina.

South Carolina Surety Agreement

Description

How to fill out South Carolina Surety Agreement?

US Legal Forms - among the biggest libraries of lawful kinds in the States - delivers a wide array of lawful record themes it is possible to download or print. Utilizing the web site, you can find 1000s of kinds for organization and person functions, sorted by categories, claims, or search phrases.You will discover the most up-to-date types of kinds like the South Carolina Surety Agreement within minutes.

If you already have a subscription, log in and download South Carolina Surety Agreement in the US Legal Forms library. The Down load option will appear on every single kind you look at. You get access to all in the past delivered electronically kinds inside the My Forms tab of your accounts.

If you want to use US Legal Forms the very first time, listed below are simple instructions to help you started off:

- Make sure you have picked out the proper kind for your town/area. Click on the Review option to review the form`s content material. Browse the kind information to ensure that you have chosen the appropriate kind.

- When the kind does not match your needs, utilize the Look for industry on top of the screen to discover the one which does.

- If you are happy with the form, verify your selection by clicking on the Buy now option. Then, pick the costs prepare you prefer and offer your references to register on an accounts.

- Method the purchase. Use your Visa or Mastercard or PayPal accounts to finish the purchase.

- Choose the format and download the form on the gadget.

- Make adjustments. Fill out, revise and print and indicator the delivered electronically South Carolina Surety Agreement.

Every single design you included with your bank account does not have an expiration particular date and it is the one you have permanently. So, in order to download or print an additional backup, just check out the My Forms segment and click on about the kind you require.

Get access to the South Carolina Surety Agreement with US Legal Forms, by far the most substantial library of lawful record themes. Use 1000s of skilled and express-certain themes that satisfy your business or person requires and needs.