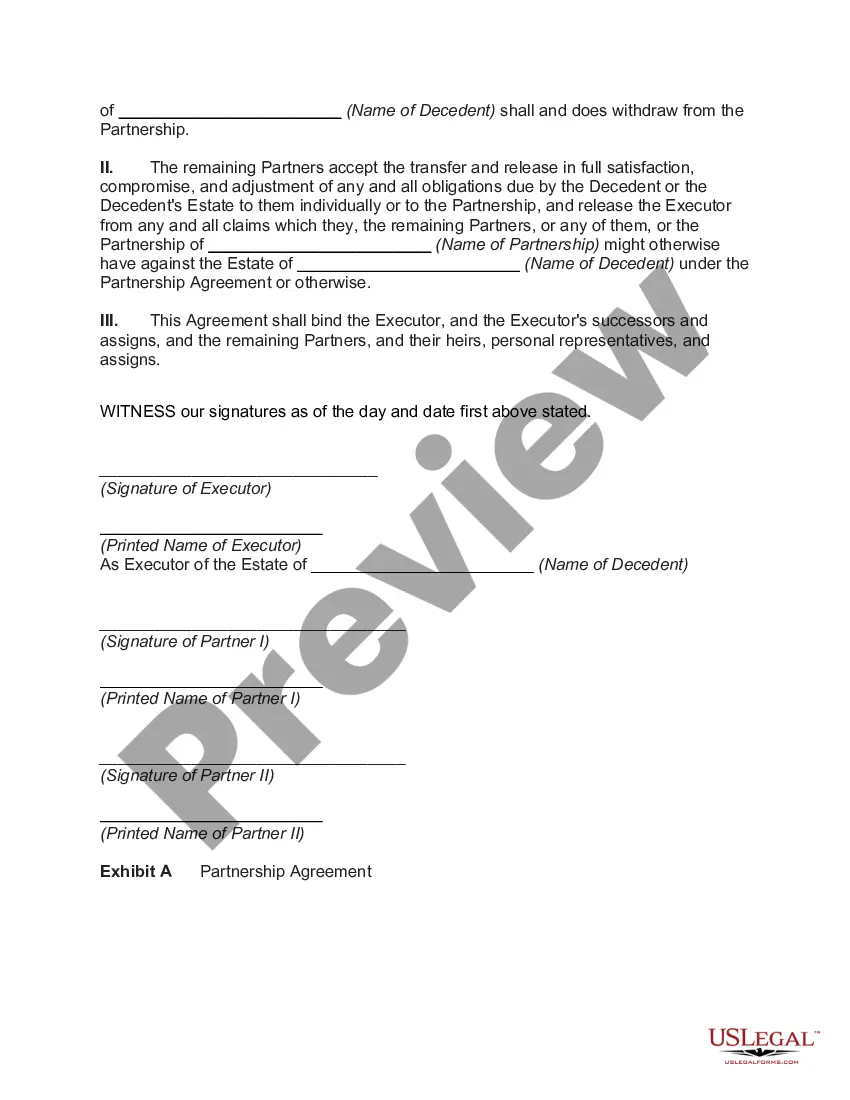

the remaining partners of a business partnership.

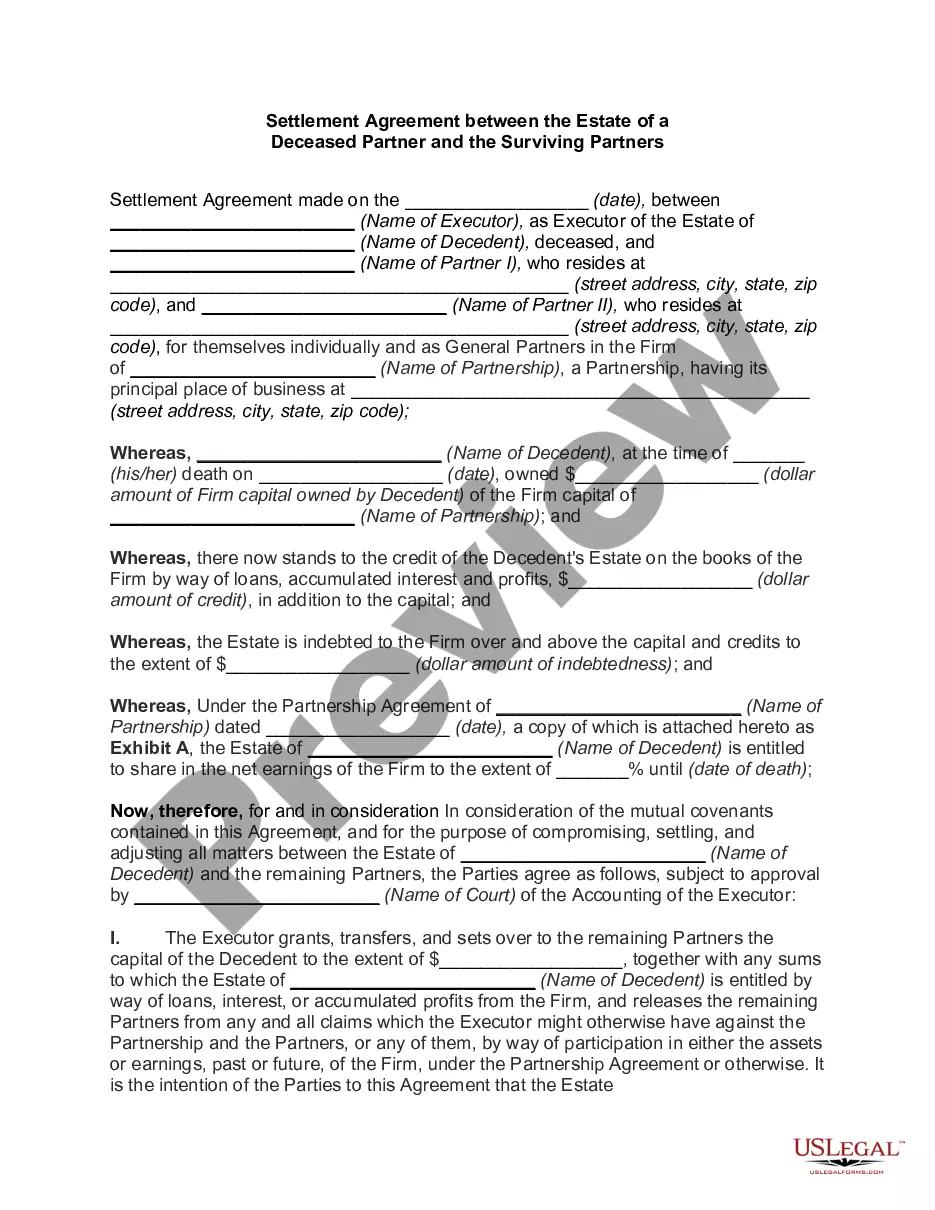

A South Carolina settlement agreement between the estate of a deceased partner and the surviving partners is a legally binding document that outlines the terms and conditions for resolving any disputes or obligations arising from the death of a partner in a business or professional partnership based in South Carolina. This agreement is designed to facilitate a smooth transition of the deceased partner's interest in the partnership to their estate while ensuring the continuity of the business and protecting the interests of both the surviving partners and the deceased partner's estate. Some key elements typically included in a South Carolina settlement agreement between the estate of a deceased partner and the surviving partners may involve the following: 1. Identification of the Parties: The agreement begins by clearly identifying the deceased partner's estate, including the executor or personal representative who will be representing the estate's interests, and the surviving partners who are party to the agreement. 2. Purpose and Intent: The agreement states the purpose of the settlement, which is to resolve any claims or disputes arising from the death of the partner and to establish the rights and obligations of both the estate and the surviving partners. 3. Distribution of Assets and Liabilities: This section outlines how the deceased partner's interest in the partnership, including assets such as capital, profits, and investments, will be distributed among the surviving partners and the estate. It also defines how any liabilities or debts, such as loans or obligations to third parties, will be handled. 4. Valuation and Buyout: In some cases, the settlement agreement may include a provision for valuing the deceased partner's interest in the partnership, either through a predetermined formula or by hiring an independent appraiser. This valuation helps establish a fair buyout price if the surviving partners wish to purchase the deceased partner's interest. 5. Succession and Management Rights: The agreement may outline the process for appointing a replacement partner or transferring the deceased partner's management responsibilities, ensuring the continued operation of the partnership. It may also address any decision-making authority and voting rights for the estate or the surviving partners. 6. Non-Compete and Confidentiality: To protect the interests of the remaining partners, the settlement agreement may include non-compete clauses preventing the estate from competing directly with the business and confidentiality provisions to safeguard trade secrets and sensitive information. 7. Dispute Resolution: In case of any future disputes or disagreements between the estate and the surviving partners, the agreement may specify the preferred method of dispute resolution, such as mediation or arbitration. Different types of South Carolina settlement agreements between the estate of a deceased partner and the surviving partners may include variations in the specific terms depending on the nature of the partnership and the desires of the parties involved. Some specialized agreements may address partnerships involved in professional services, real estate ventures, or joint ventures with multiple partners, each requiring tailored provisions to suit their unique circumstances. Overall, a South Carolina settlement agreement between the estate of a deceased partner and the surviving partners ensures a fair and orderly transition for the partnership, protecting the rights of all parties involved and allowing the business to continue operating without disruption.