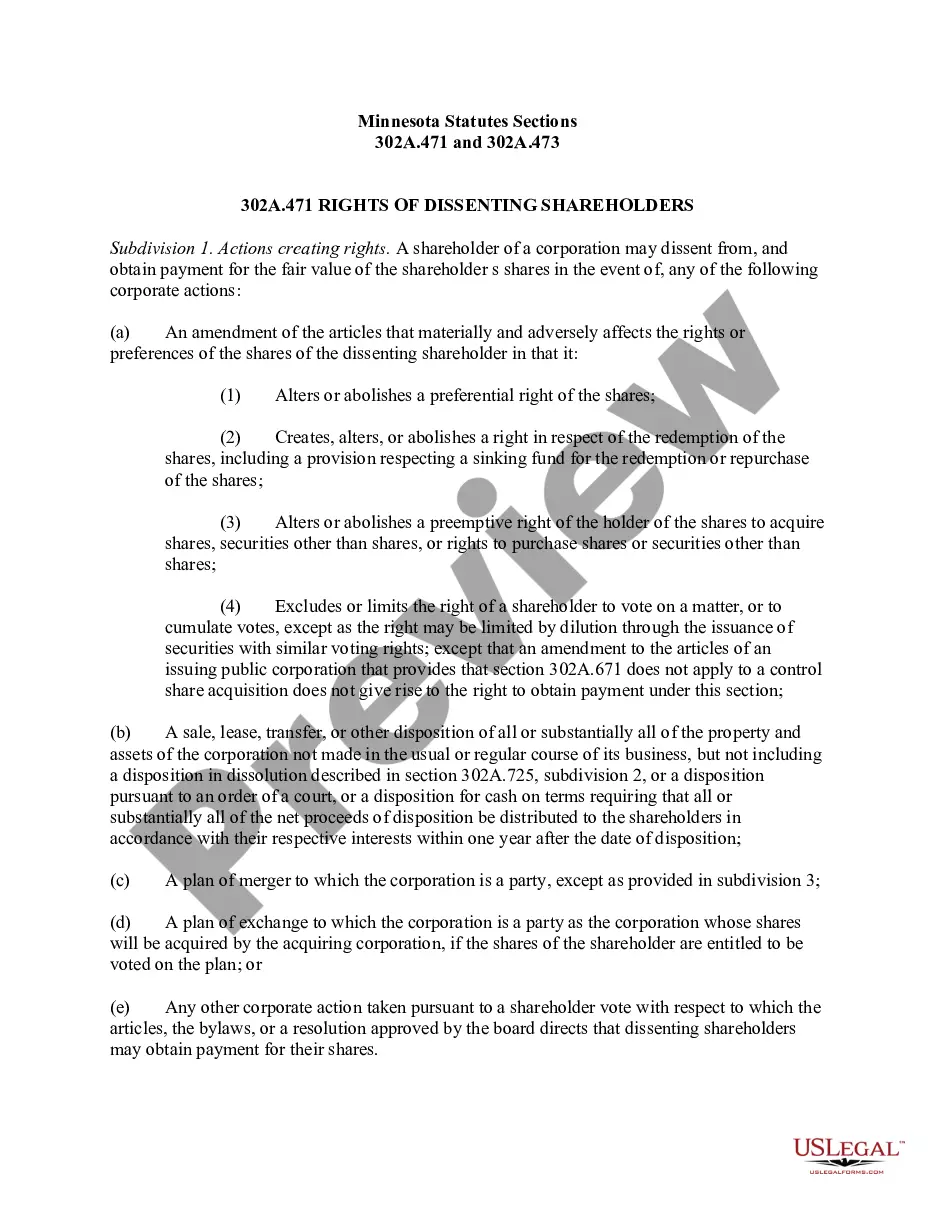

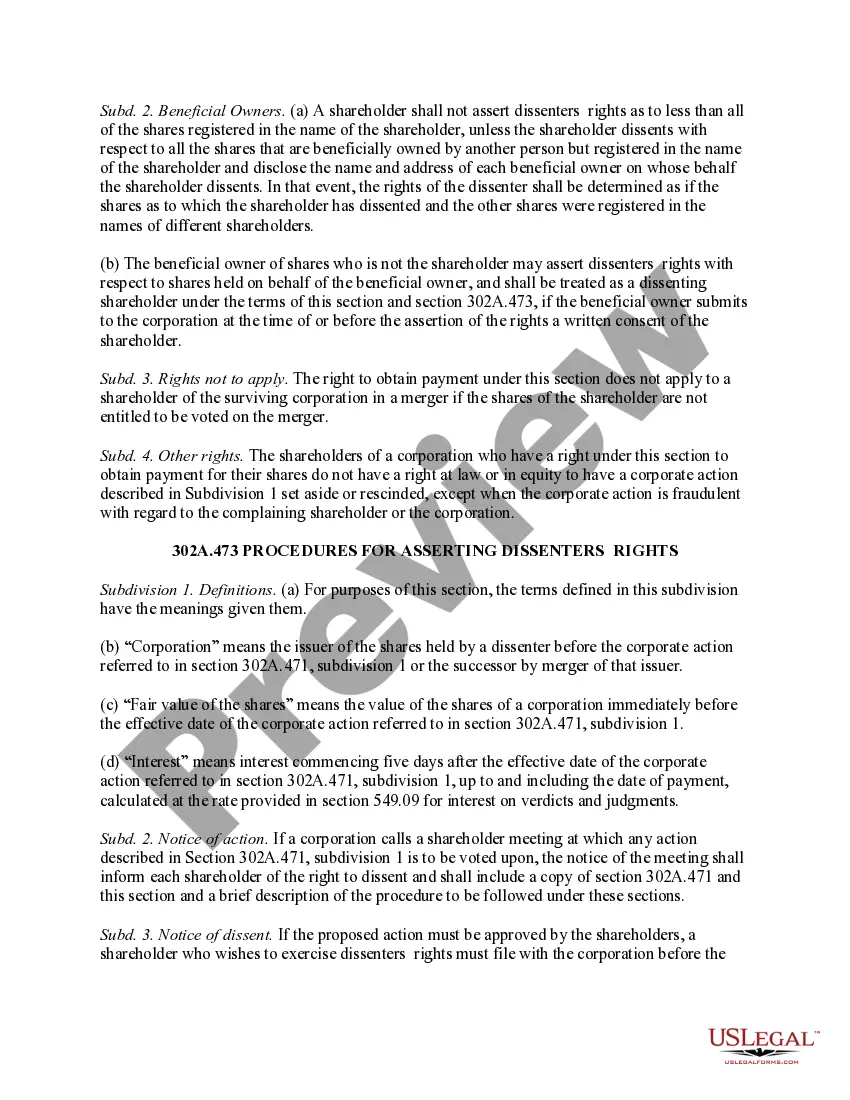

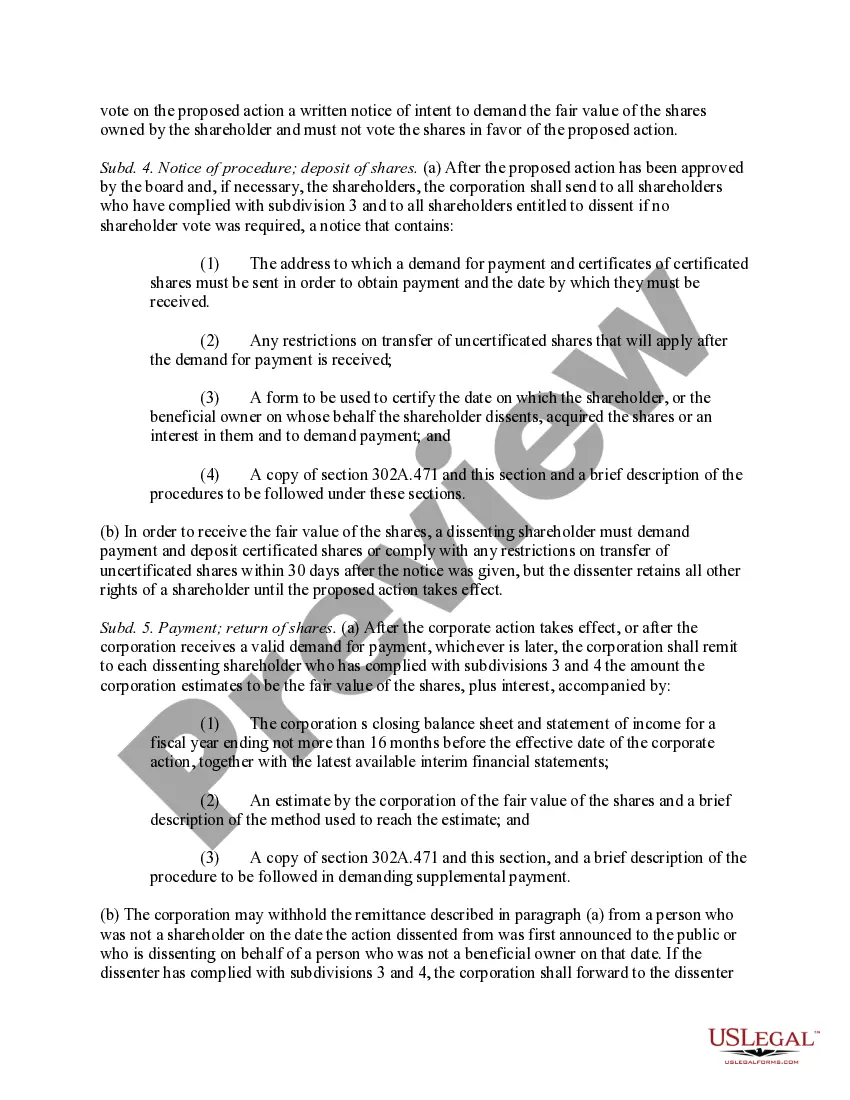

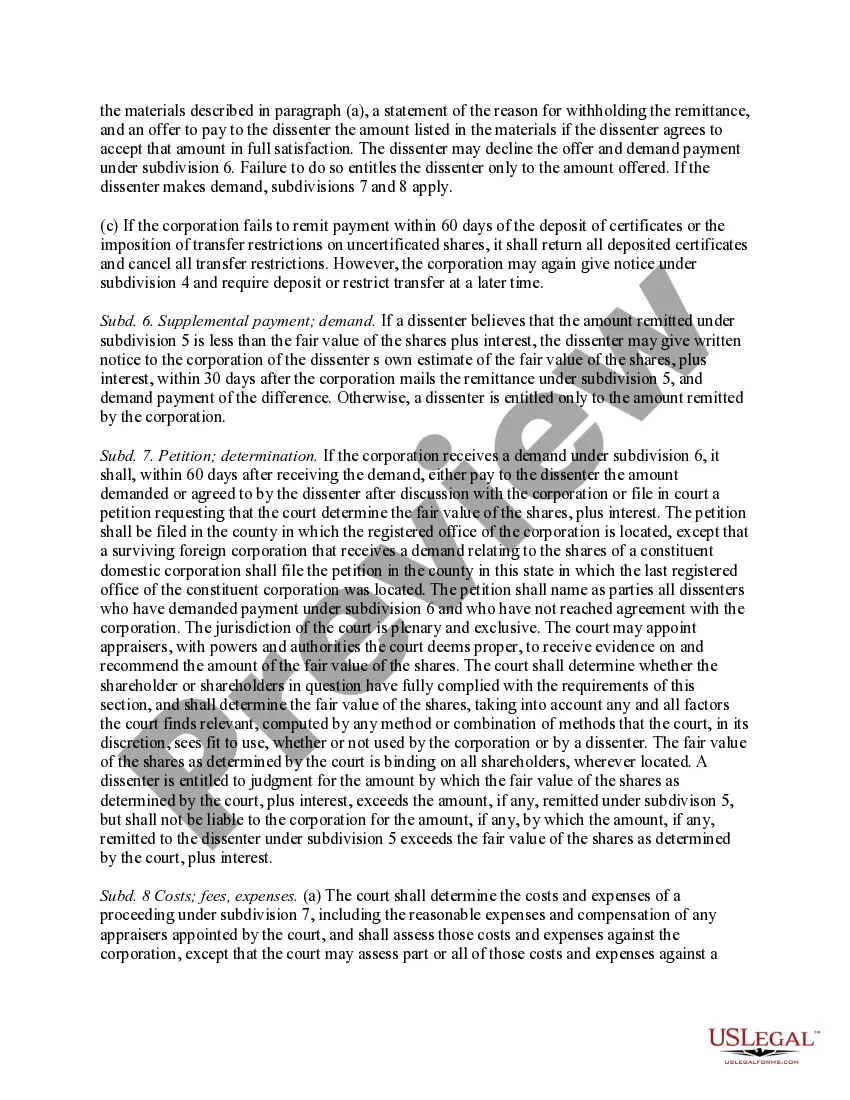

TITLE: Understanding South Carolina Sections 302A.471 and 302A.473 of Minnesota Business Corporation Act: An In-Depth Look INTRODUCTION: South Carolina plays a crucial role in governing business corporations, and two significant sections of the Minnesota Business Corporation Act—302A.471 and 302A.473—are specifically dedicated to regulating various aspects. In this article, we will explore the details of these sections, their significance, and any relevant distinctions. SECTION 1: OVERVIEW OF SOUTH CAROLINA SECTIONS 302A.471 AND 302A.473 Section 302A.471: Declaration of Dividends: Keywords: South Carolina, Minnesota Business Corporation Act, Section 302A.471, declaration, dividends Section 302A.471 of the Minnesota Business Corporation Act pertains to the declaration of dividends by South Carolina corporations. This section outlines the legal requirements and limitations associated with dividend declarations. It specifies the conditions under which dividends may be declared, the process involved, and various restrictions that must be taken into account. Key Points: 1. Dividend Declaration Requirements: Section 302A.471 establishes the criteria that must be met before a dividend can be declared. These include the availability of surplus, adherence to statutory capital requirements, and consideration of potential impairments or restrictions. 2. Prudent Business Judgment: Companies must exercise careful and prudent business judgment while determining the timing and amount of dividend declarations. This includes considering factors such as financial statements, future prospects, and potential liabilities. 3. Restrictions and Prohibitions: The section highlights certain restrictions on dividend declarations, such as the prohibition against declaring dividends that would render the corporation insolvent or unable to meet its obligations. It also addresses situations when dividends may be temporarily suspended or restricted. SECTION 2: DISTINCT TYPES OF SOUTH CAROLINA SECTIONS 302A.471 AND 302A.473 Section 302A.471(f): Restrictions on Declaring Dividends: Keywords: South Carolina, Minnesota Business Corporation Act, Section 302A.471(f), restrictions, declaring dividends Section 302A.471(f) of the Minnesota Business Corporation Act addresses specific restrictions on declaring dividends. This subsection expands on the limitations mentioned in Section 302A.471, further guiding South Carolina corporations on dividend declarations. Key Points: 1. Additional Restrictions: Section 302A.471(f) elaborates on factors that may restrict dividend declarations, including contractual obligations, borrowing, and capital maintenance requirements. Such restrictions help maintain stability and ensure the corporation's ability to fulfill obligations beyond dividend payments. 2. Positive Determination: To determine whether dividends can be declared, corporations analyze financial statements, balance sheets, potential risks, forecasts, and other relevant factors. Section 302A.471(f) emphasizes the need for a positive determination indicating that the declaration would not adversely impact the company's financial position or expose it to potential solvency issues. Section 302A.473: Right of Dissent for Shareholders: Keywords: South Carolina, Minnesota Business Corporation Act, Section 302A.473, right of dissent, shareholders Section 302A.473 of the Minnesota Business Corporation Act grants shareholders of South Carolina corporations the right to dissent in certain circumstances. This crucial provision safeguards shareholder interests and provides them with an avenue to express disagreement in specific corporate actions. Key Points: 1. Dissent Rights: When a corporation undertakes certain actions, such as mergers, consolidations, or amendments to articles of incorporation, shareholders who dissent have the right to receive fair monetary compensation. This helps protect shareholders' investment and ensures they are adequately compensated in case of disapproval. 2. Procedures and Limitations: Section 302A.473 outlines the procedural requirements, including timely notice of dissent and filing a dissenting shareholder notice, to exercise dissent rights effectively. It also states the time frame within which shareholders must initiate legal proceedings related to dissent. CONCLUSION: South Carolina Sections 302A.471 and 302A.473 of the Minnesota Business Corporation Act encompass vital aspects in the governance of business corporations. With Section 302A.471 focusing on dividend declarations and restrictions, and Section 302A.473 detailing dissent rights for shareholders, these provisions play a pivotal role in protecting corporate stakeholders' interests and maintaining financial stability. Understanding these sections is crucial for both South Carolina corporations and shareholders alike, ensuring compliance and an environment of fairness in business operations.

South Carolina Sections 302A.471 and 302A.473 of Minnesota Business Corporation Act

Description

How to fill out South Carolina Sections 302A.471 And 302A.473 Of Minnesota Business Corporation Act?

Are you inside a place that you will need papers for both organization or individual reasons nearly every day? There are a lot of lawful file templates available on the Internet, but finding types you can rely on is not straightforward. US Legal Forms delivers 1000s of form templates, like the South Carolina Sections 302A.471 and 302A.473 of Minnesota Business Corporation Act, that happen to be published in order to meet federal and state needs.

In case you are already familiar with US Legal Forms web site and also have a merchant account, basically log in. After that, it is possible to acquire the South Carolina Sections 302A.471 and 302A.473 of Minnesota Business Corporation Act web template.

Should you not have an profile and need to begin to use US Legal Forms, abide by these steps:

- Obtain the form you will need and make sure it is to the correct city/area.

- Make use of the Review switch to analyze the shape.

- Look at the outline to actually have chosen the correct form.

- In the event the form is not what you`re trying to find, utilize the Lookup discipline to obtain the form that meets your needs and needs.

- When you find the correct form, click Buy now.

- Pick the pricing prepare you desire, complete the necessary info to produce your bank account, and pay money for the order using your PayPal or charge card.

- Pick a hassle-free document formatting and acquire your duplicate.

Locate every one of the file templates you may have purchased in the My Forms menus. You can aquire a more duplicate of South Carolina Sections 302A.471 and 302A.473 of Minnesota Business Corporation Act anytime, if possible. Just go through the needed form to acquire or printing the file web template.

Use US Legal Forms, the most considerable variety of lawful varieties, in order to save time and steer clear of blunders. The services delivers skillfully produced lawful file templates that you can use for a selection of reasons. Produce a merchant account on US Legal Forms and commence making your daily life easier.