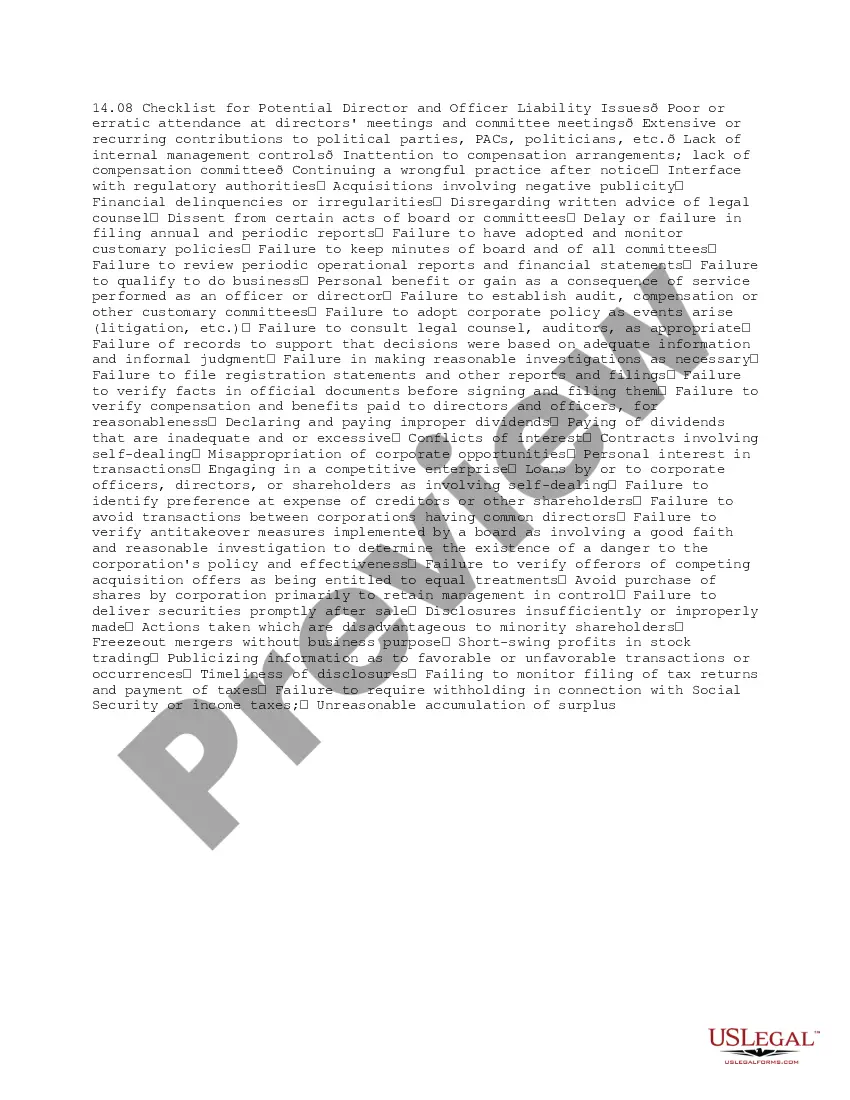

This due diligence checklist lists liability issues for future directors and officers in a company regarding business transactions.

South Carolina Checklist for Potential Director and Officer Liability Issues

Category:

State:

Multi-State

Control #:

US-DD01408

Format:

Word;

PDF;

Rich Text

Instant download

Description

How to fill out South Carolina Checklist For Potential Director And Officer Liability Issues?

Are you presently in the placement in which you need files for possibly business or personal purposes almost every time? There are plenty of authorized document layouts available on the Internet, but getting ones you can trust is not simple. US Legal Forms delivers 1000s of form layouts, like the South Carolina Checklist for Potential Director and Officer Liability Issues, that happen to be composed to fulfill federal and state demands.

Should you be previously informed about US Legal Forms internet site and get a free account, merely log in. Afterward, you can download the South Carolina Checklist for Potential Director and Officer Liability Issues web template.

Unless you come with an account and want to begin using US Legal Forms, abide by these steps:

- Get the form you need and make sure it is to the proper town/county.

- Utilize the Preview key to examine the shape.

- Read the information to actually have selected the proper form.

- When the form is not what you are seeking, utilize the Research discipline to get the form that suits you and demands.

- If you get the proper form, click Acquire now.

- Opt for the prices plan you need, fill out the necessary info to produce your bank account, and pay for your order using your PayPal or credit card.

- Decide on a practical document format and download your duplicate.

Find all of the document layouts you possess bought in the My Forms menus. You can obtain a more duplicate of South Carolina Checklist for Potential Director and Officer Liability Issues whenever, if possible. Just click the necessary form to download or print the document web template.

Use US Legal Forms, by far the most considerable collection of authorized varieties, to save time and avoid faults. The services delivers skillfully created authorized document layouts which you can use for an array of purposes. Produce a free account on US Legal Forms and commence creating your way of life easier.

Form popularity

FAQ

D&O insurance does cover2026"The type of D&O lawsuits (include) claims of negligence and allegations of mismanagement on behalf of the board; housing discriminatory complaints, usually associated with a denial of a purchase/sublet application involving a designated minority class; employment discrimination, sexual

Board members can generally be held personally liable for breach of fiduciary duties, particularly in cases involving egregious neglect of the Board member's oversight responsibilities or the receipt of a personal benefit from the organization's assets or resources (sometimes referred to as private inurement).

D&O policies include an exclusion for losses related to criminal or deliberately fraudulent activities. Additionally, if an individual insured receives illegal profits or remuneration to which they were not legally entitled, they will not be covered if a lawsuit is brought forward due to this.

Management liability, also known as directors and officers' insurance, includes extra coverage for the individual directors or officers of a business for their official company actions. Long story short, it's coverage for your managers. That's the big difference between it and professional liability.

The following are several examples of Management Liability (D&O) claims.Misrepresentation. Directors and officers at a company failed to disclose material facts and provided inaccurate and misleading information to their investors.Credit Fraud.Stolen Corporate Secrets.Recruiting Sales Executives.Investment Agreement.

Directors and officers (D&O) liability insurance protects the personal assets of corporate directors and officers, and their spouses, in the event they are personally sued by employees, vendors, competitors, investors, customers, or other parties, for actual or alleged wrongful acts in managing a company.

Limited liability protects shareholders, directors, officers and employees against personal liability for actions taken in the name of the corporation and corporate debts. Ordinarily, an officer of the corporation, whether also a shareholder, director or employee, cannot be held personally liable.

Typically, a corporate officer isn't held personally liable, as long as his or her actions fall within the scope of their position and the parameters of the law. An officer of a corporation may serve on the board of directors or fulfill a managerial role.

Exclusion a provision of an insurance policy or bond referring to hazards, perils, circumstances, or property not covered by the policy. Exclusions are usually contained in the coverage form or causes of loss form used to construct the insurance policy.

More info

The cover page on the legal-looking document ?com- mands? you to ?appear? or ?answer? ?The Complaint? in twenty (20) days. You are a director or officer of ...3 pagesMissing: Carolina ? Must include: Carolina

The cover page on the legal-looking document ?com- mands? you to ?appear? or ?answer? ?The Complaint? in twenty (20) days. You are a director or officer of ... South Carolina Education Lottery (SCEL). Attention: Licensing Department. PO Box 11949. Columbia, SC 29211-1949. Filling out the application completely and ...Therefore, it is possible under occurrence based policies to have a number of policies issued over a number of years triggered where a claim involves an ... DIRECTORS AND OFFICERS looking to buy liability insurance arethe scope of D&O cover and how they should respond in the event of a claim ...20 pagesMissing: Carolina ? Must include: Carolina

? DIRECTORS AND OFFICERS looking to buy liability insurance arethe scope of D&O cover and how they should respond in the event of a claim ... That must be weighed to evaluate possible shortfalls in coverage.officers and directors and the company's other liability insurance.12 pagesMissing: Checklist ? Must include: Checklist

that must be weighed to evaluate possible shortfalls in coverage.officers and directors and the company's other liability insurance. Let the Good Deed Go Unpunished: Avoiding Nonprofit Board Liability. By Zachary S. Kester, Executive Director and Robert Miller, Program Officer ... The board of directors will vote to dissolve the organization, but its job doesn't end there. Before making an important decision such as dissolving a ... LINE(S) OF INSURANCE. CODES. Directors & Officers Liability. 17.0006. CODE: 17.0000. IF CHECKLIST IS NOT APPLICABLE, PLEASE EXPLAIN: REVIEW. REQUIREMENTS. Troopers and officers of the South Carolina Highway Patrol.safety issues and utilizes these technologies to deter driving under the. Nevada, New York, North Dakota, Oregon, South Carolina, South Dakota, andcomplete discussion of the requirement for clergy to report child abuse and.