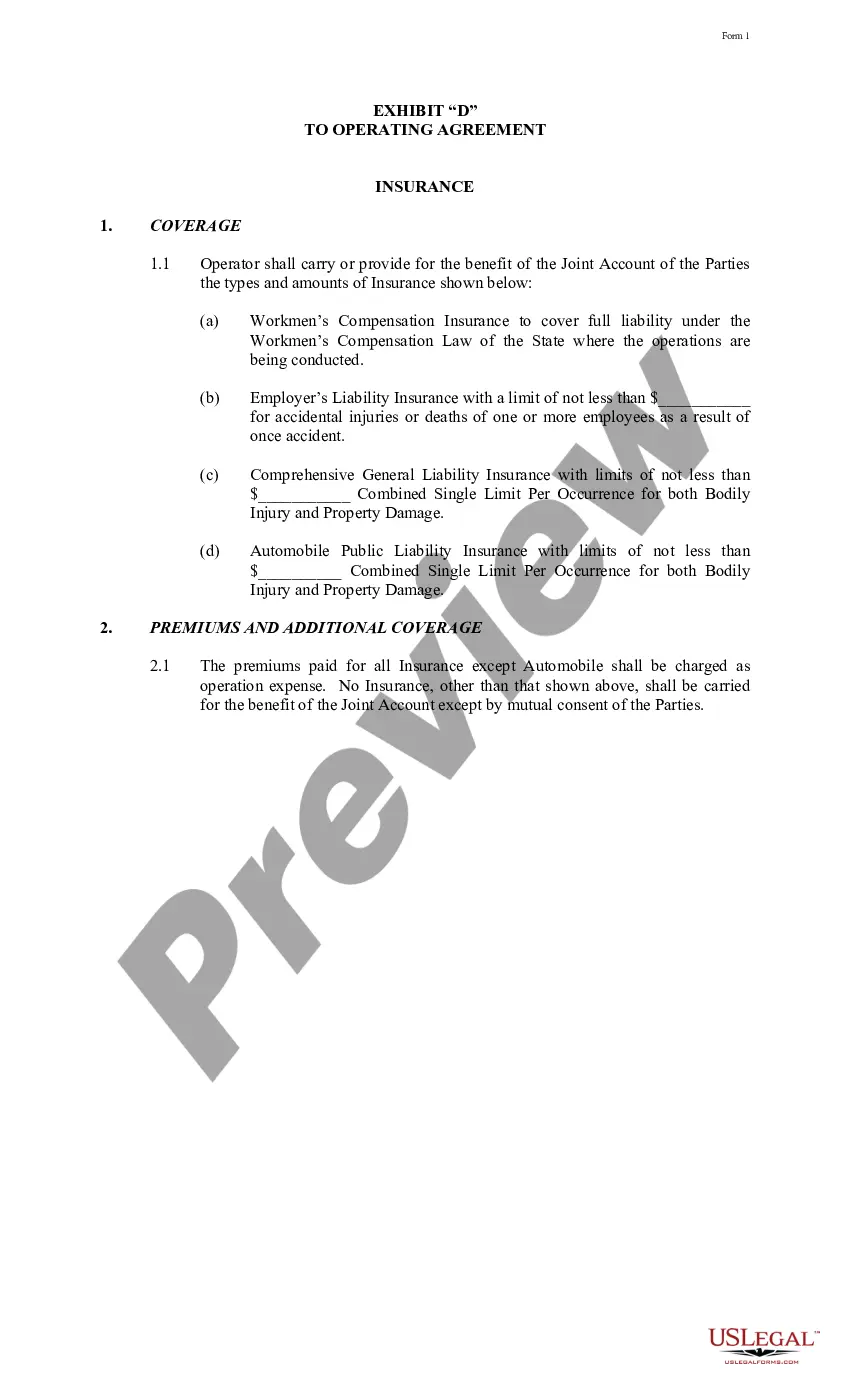

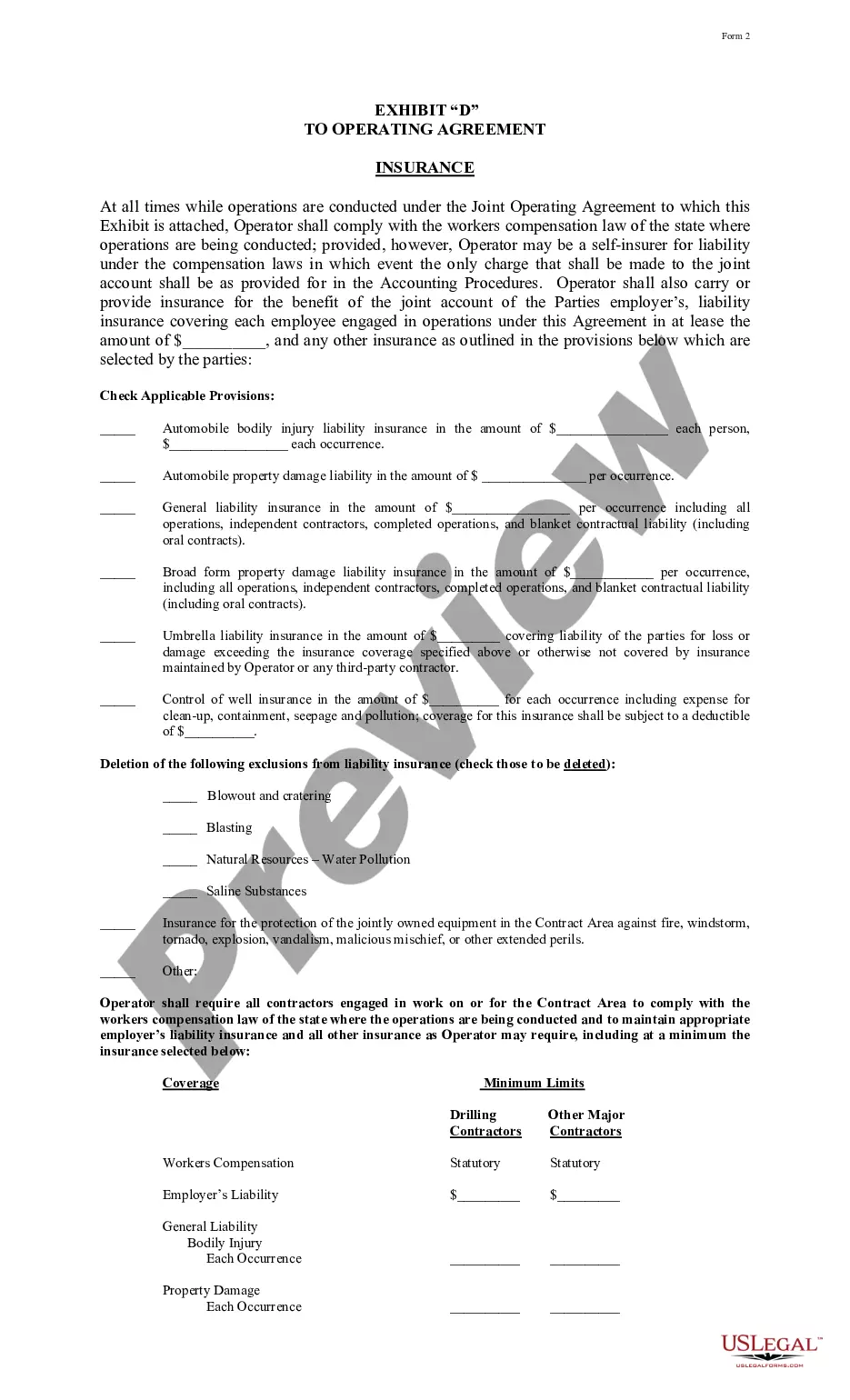

South Carolina Exhibit C Accounting Procedure Joint Operations

Description

How to fill out Exhibit C Accounting Procedure Joint Operations?

If you want to complete, obtain, or produce legal papers web templates, use US Legal Forms, the most important selection of legal forms, which can be found on the Internet. Take advantage of the site`s easy and handy lookup to get the files you will need. Various web templates for business and person functions are categorized by categories and claims, or key phrases. Use US Legal Forms to get the South Carolina Exhibit C Accounting Procedure Joint Operations within a few click throughs.

In case you are previously a US Legal Forms buyer, log in to your profile and then click the Down load switch to obtain the South Carolina Exhibit C Accounting Procedure Joint Operations. You can also accessibility forms you formerly saved from the My Forms tab of your respective profile.

If you use US Legal Forms for the first time, follow the instructions listed below:

- Step 1. Make sure you have selected the shape for the appropriate city/nation.

- Step 2. Utilize the Preview option to look through the form`s content material. Do not neglect to learn the explanation.

- Step 3. In case you are not satisfied using the develop, take advantage of the Search area towards the top of the display screen to find other variations in the legal develop web template.

- Step 4. When you have identified the shape you will need, click the Buy now switch. Pick the rates plan you choose and put your references to register to have an profile.

- Step 5. Approach the purchase. You may use your credit card or PayPal profile to perform the purchase.

- Step 6. Pick the structure in the legal develop and obtain it in your device.

- Step 7. Complete, modify and produce or indicator the South Carolina Exhibit C Accounting Procedure Joint Operations.

Every legal papers web template you buy is your own forever. You might have acces to each and every develop you saved in your acccount. Select the My Forms section and select a develop to produce or obtain once again.

Compete and obtain, and produce the South Carolina Exhibit C Accounting Procedure Joint Operations with US Legal Forms. There are millions of specialist and status-certain forms you can utilize for your business or person requirements.