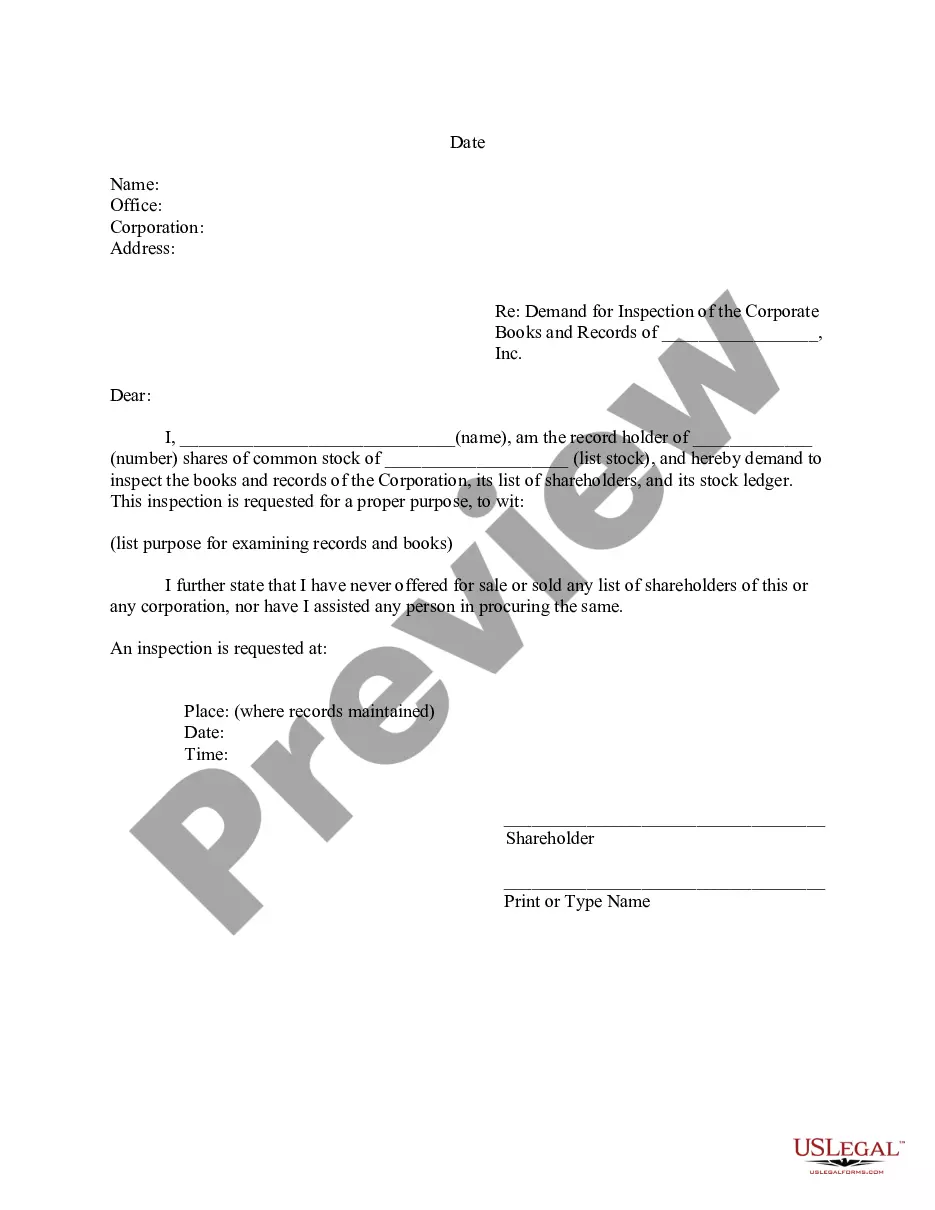

Form with which a shareholder may demand the opportunity to inspect the records of a corporation in which the shareholder holds stock.

South Dakota Demand Inspection of Books — Corporate Resolutions refers to a legal process in the state of South Dakota that allows shareholders of a corporation to demand access to the corporation's books and records for inspection. This process is governed by South Dakota state laws and provides shareholders with a mechanism to ensure transparency and accountability within the corporation. The demand for inspection of books and records can be made by any shareholder of the corporation and must be in writing, specifying the documents or records the shareholder wishes to inspect. The demand must also include a proper purpose for the inspection, which can include investigating the corporation's financial condition, evaluating potential mismanagement or fraudulent activities, or monitoring compliance with corporate resolutions. There are different types of South Dakota Demand Inspection of Books — Corporate Resolutions, depending on the specific purposes and circumstances of the shareholder. Some of these types include: 1. Financial Inspection: Shareholders may request access to financial statements, tax records, and other financial documents to assess the corporation's financial health, monitor profitability, or evaluate investment opportunities. 2. Compliance Inspection: Shareholders may demand inspection of corporate records to ensure compliance with corporate resolutions, bylaws, and other governing documents. This type of inspection can help identify any breaches of fiduciary duties or violations of corporate policies. 3. Mismanagement Investigation: Shareholders may seek access to corporate books and records to investigate potential mismanagement, self-dealing, or fraudulent activities within the corporation. This could involve reviewing minutes of board meetings, contracts, or internal communications to uncover any improper actions. 4. Merger or Acquisition Inspection: In the event of a merger or acquisition, shareholders may request access to documents related to the transaction, such as valuation reports, due diligence materials, or agreements. This type of inspection enables shareholders to evaluate the fairness and legality of the proposed transaction. It is important to note that shareholders must have a proper purpose for requesting an inspection of books and records. This means that the purpose must be directly related to the shareholder's interest as a shareholder and not for personal or unrelated reasons. Additionally, the corporation may impose reasonable restrictions on the inspection, such as time, place, or procedures, to protect sensitive or confidential information. In summary, South Dakota Demand Inspection of Books — Corporate Resolutions is a legal mechanism that enables shareholders to demand access to corporate books and records for inspection. This process facilitates transparency and helps shareholders monitor the corporation's financial health, compliance with resolutions, investigate potential mismanagement, or evaluate merger and acquisition transactions.South Dakota Demand Inspection of Books — Corporate Resolutions refers to a legal process in the state of South Dakota that allows shareholders of a corporation to demand access to the corporation's books and records for inspection. This process is governed by South Dakota state laws and provides shareholders with a mechanism to ensure transparency and accountability within the corporation. The demand for inspection of books and records can be made by any shareholder of the corporation and must be in writing, specifying the documents or records the shareholder wishes to inspect. The demand must also include a proper purpose for the inspection, which can include investigating the corporation's financial condition, evaluating potential mismanagement or fraudulent activities, or monitoring compliance with corporate resolutions. There are different types of South Dakota Demand Inspection of Books — Corporate Resolutions, depending on the specific purposes and circumstances of the shareholder. Some of these types include: 1. Financial Inspection: Shareholders may request access to financial statements, tax records, and other financial documents to assess the corporation's financial health, monitor profitability, or evaluate investment opportunities. 2. Compliance Inspection: Shareholders may demand inspection of corporate records to ensure compliance with corporate resolutions, bylaws, and other governing documents. This type of inspection can help identify any breaches of fiduciary duties or violations of corporate policies. 3. Mismanagement Investigation: Shareholders may seek access to corporate books and records to investigate potential mismanagement, self-dealing, or fraudulent activities within the corporation. This could involve reviewing minutes of board meetings, contracts, or internal communications to uncover any improper actions. 4. Merger or Acquisition Inspection: In the event of a merger or acquisition, shareholders may request access to documents related to the transaction, such as valuation reports, due diligence materials, or agreements. This type of inspection enables shareholders to evaluate the fairness and legality of the proposed transaction. It is important to note that shareholders must have a proper purpose for requesting an inspection of books and records. This means that the purpose must be directly related to the shareholder's interest as a shareholder and not for personal or unrelated reasons. Additionally, the corporation may impose reasonable restrictions on the inspection, such as time, place, or procedures, to protect sensitive or confidential information. In summary, South Dakota Demand Inspection of Books — Corporate Resolutions is a legal mechanism that enables shareholders to demand access to corporate books and records for inspection. This process facilitates transparency and helps shareholders monitor the corporation's financial health, compliance with resolutions, investigate potential mismanagement, or evaluate merger and acquisition transactions.