A gift involves transferring title by voluntary action of the owner without receiving anything in exchange. A gift of property is a:

- passing of title;

- made with the intent to pass title;

- without receiving money or value in consideration for the passing of title.

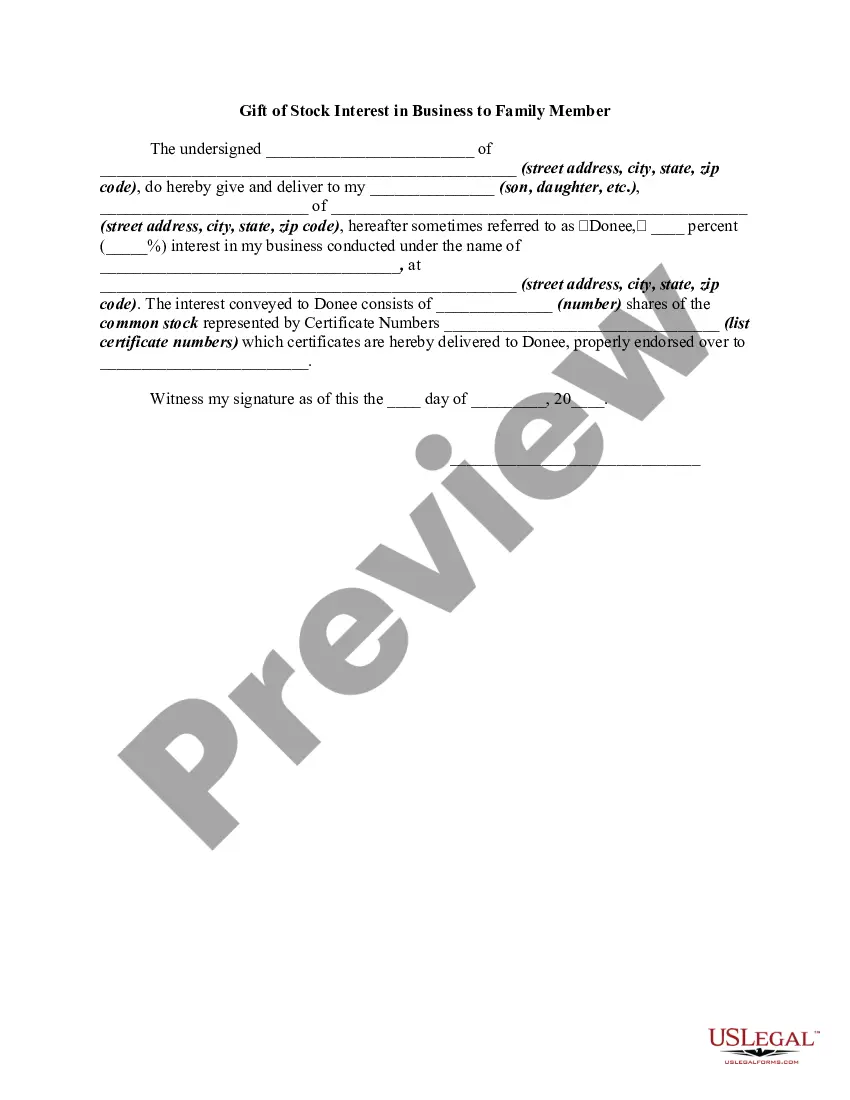

The following form is a gift to a family member of stock in a business owned by the donor.

The South Dakota Gift of Stock Interest in Business to Family Member refers to a legal mechanism available in the state of South Dakota for individuals to transfer ownership or ownership interest in a business entity to a family member through the gifting of stock. This transaction allows the transferor to gift a specific portion of their ownership in a business to a family member, transferring all rights and responsibilities associated with that stock interest. Gifts of stock interests in businesses to family members serve multiple purposes, including estate planning, business restructuring, and passing down ownership to the next generation. By gifting stock interests, the transferor can control the timing and beneficiaries of the transfer while minimizing tax liabilities. It is crucial to note that professional legal and tax advice is recommended during the process to ensure compliance with applicable laws and regulations. There may be different types of South Dakota Gift of Stock Interest in Business to Family Member, which may vary based on the business entity involved. Common types of business structures that stock interests can be gifted include corporations, limited liability companies (LCS), partnerships, and sole proprietorship. In the case of a corporation, the stock interest can be gifted through the transfer of shares. The transferor may have the option to gift a percentage or specific number of shares to the family member, facilitated by the use of a stock transfer form. This form typically outlines details such as the names of the transferor and the recipient, the number of shares being transferred, and any specific conditions or restrictions related to the transfer. For LCS, the transfer of ownership interests can be made by either transferring membership interests or by amending the operating agreement to reflect the new ownership structure. Similar to corporations, LCS often require the completion of specific forms, such as an assignment of membership interest document, to formalize the transfer. In the case of partnerships, transfers of stock interest can be made by amending the partnership agreement and obtaining the necessary approvals from existing partners. This process may require the family member receiving the stock interest to be admitted as a new partner or be designated as a limited partner, depending on the partnership structure. Finally, in the case of a sole proprietorship, the gift of stock interest typically involves transferring business assets to the family member rather than a specific ownership entity. This type of transfer may require the revision of legal contracts, licenses, and permits to reflect the new ownership structure. It is important to understand that the specific requirements and legal procedures for the South Dakota Gift of Stock Interest in Business to Family Member may vary depending on the type of business entity, the nature of the transfer, and the individual circumstances involved. Seeking guidance from legal and tax professionals experienced in South Dakota business laws can help ensure compliance and facilitate a smooth transfer process.

The South Dakota Gift of Stock Interest in Business to Family Member refers to a legal mechanism available in the state of South Dakota for individuals to transfer ownership or ownership interest in a business entity to a family member through the gifting of stock. This transaction allows the transferor to gift a specific portion of their ownership in a business to a family member, transferring all rights and responsibilities associated with that stock interest. Gifts of stock interests in businesses to family members serve multiple purposes, including estate planning, business restructuring, and passing down ownership to the next generation. By gifting stock interests, the transferor can control the timing and beneficiaries of the transfer while minimizing tax liabilities. It is crucial to note that professional legal and tax advice is recommended during the process to ensure compliance with applicable laws and regulations. There may be different types of South Dakota Gift of Stock Interest in Business to Family Member, which may vary based on the business entity involved. Common types of business structures that stock interests can be gifted include corporations, limited liability companies (LCS), partnerships, and sole proprietorship. In the case of a corporation, the stock interest can be gifted through the transfer of shares. The transferor may have the option to gift a percentage or specific number of shares to the family member, facilitated by the use of a stock transfer form. This form typically outlines details such as the names of the transferor and the recipient, the number of shares being transferred, and any specific conditions or restrictions related to the transfer. For LCS, the transfer of ownership interests can be made by either transferring membership interests or by amending the operating agreement to reflect the new ownership structure. Similar to corporations, LCS often require the completion of specific forms, such as an assignment of membership interest document, to formalize the transfer. In the case of partnerships, transfers of stock interest can be made by amending the partnership agreement and obtaining the necessary approvals from existing partners. This process may require the family member receiving the stock interest to be admitted as a new partner or be designated as a limited partner, depending on the partnership structure. Finally, in the case of a sole proprietorship, the gift of stock interest typically involves transferring business assets to the family member rather than a specific ownership entity. This type of transfer may require the revision of legal contracts, licenses, and permits to reflect the new ownership structure. It is important to understand that the specific requirements and legal procedures for the South Dakota Gift of Stock Interest in Business to Family Member may vary depending on the type of business entity, the nature of the transfer, and the individual circumstances involved. Seeking guidance from legal and tax professionals experienced in South Dakota business laws can help ensure compliance and facilitate a smooth transfer process.