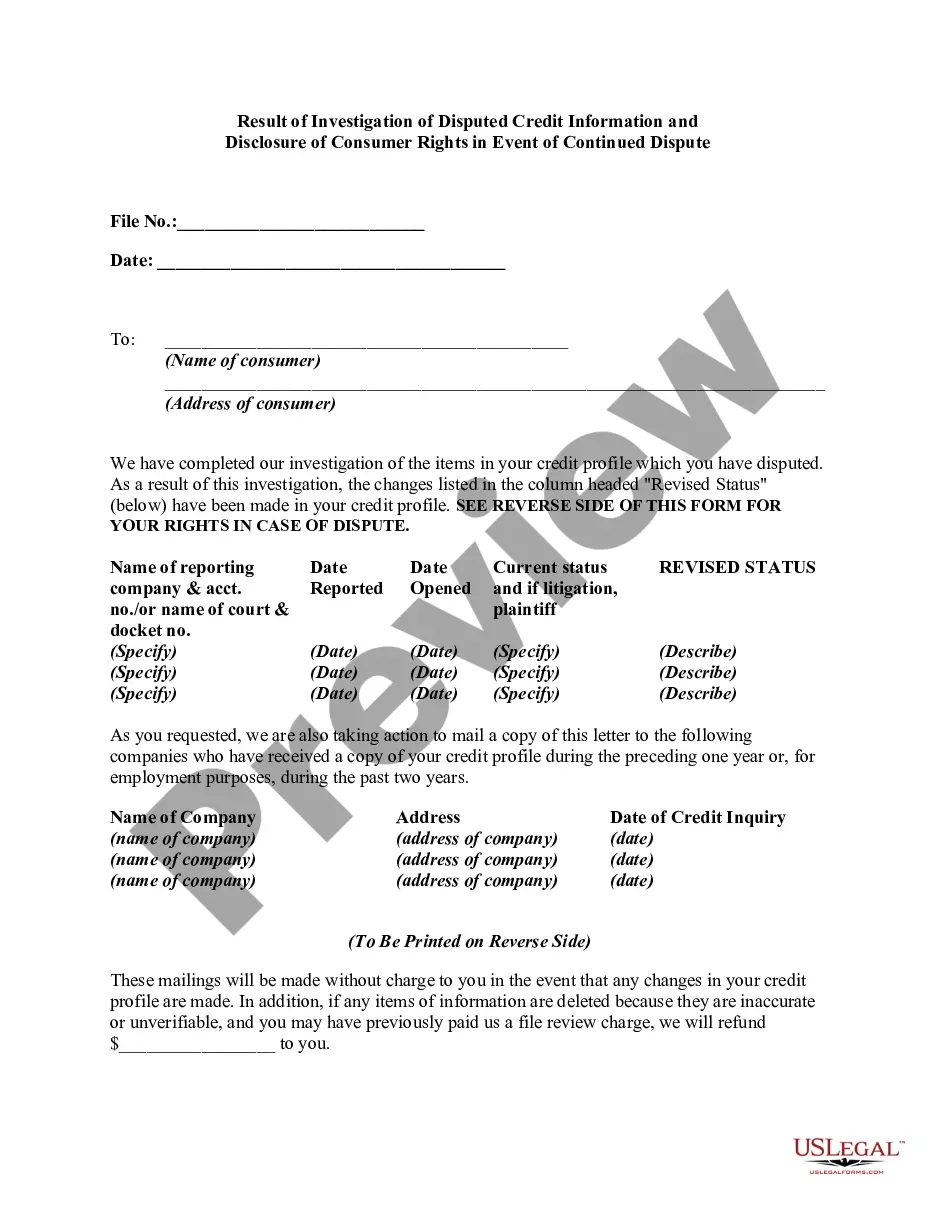

Under the Fair Credit Reporting Act, if a consumer disputes the completeness or accuracy of any item of information in the consumer's file, and the dispute is directly conveyed to the consumer reporting agency by the consumer, the reporting agency must, free of charge, conduct a reasonable reinvestigation to determine whether the disputed information is inaccurate, unless it has reasonable grounds to believe that the dispute is frivolous or irrelevant. If the information is erroneous, inaccurate, or can no longer be verified, the credit reporting agency must promptly correct or delete it and refrain from reporting the information in subsequent consumer reports.

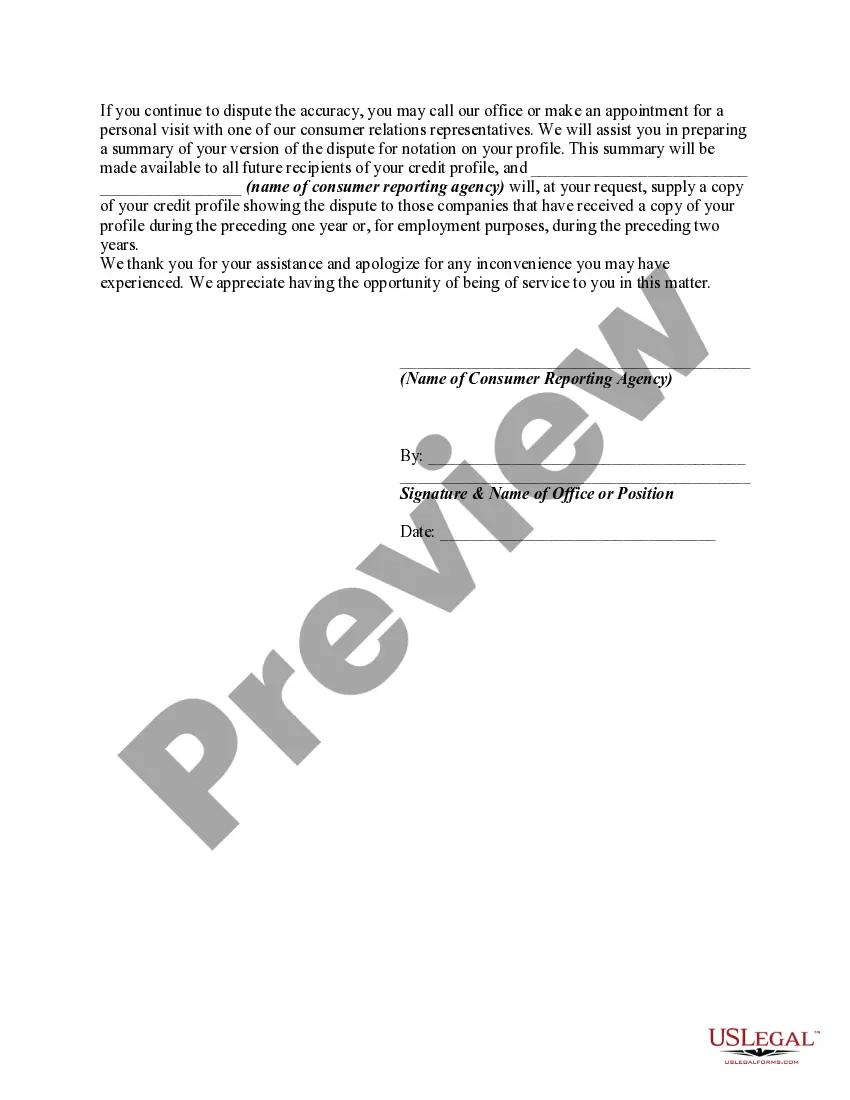

Following any deletion of information or notation as to disputed information, the agency, on request of the consumer, must furnish to certain persons either: (1) notification of the deletion; or (2) the consumer's statement of the dispute or the agency's summary of the statement. The consumer reporting agency must clearly and conspicuously disclose the consumer's rights to make such a request, such disclosure to be made at or prior to the time the information is deleted or the consumer's statement regarding the disputed information is received.

South Dakota is a state located in the Midwestern region of the United States. Known for its breathtaking landscapes, iconic monuments, and historical significance, South Dakota offers a unique blend of cultural experiences and natural wonders. When it comes to the investigation of disputed credit information and disclosure of consumer rights in the event of a continued dispute, South Dakota has specific laws and regulations in place to protect consumers. These regulations ensure that individuals have the right to dispute any inaccurate or incomplete credit information reported by credit bureaus or creditors. The result of an investigation of disputed credit information in South Dakota can have different outcomes. If the investigation concludes that the credit information is accurate, it will remain on the consumer's credit report as it was initially reported. However, if the investigation determines that the credit information is inaccurate or incomplete, it will be corrected or removed from the consumer's credit report. South Dakota's consumer rights provide a comprehensive framework for individuals involved in credit disputes. Consumers have the right to receive written notification of the investigation's results within a specified timeframe. If the dispute remains unresolved, consumers have the right to request that a statement of the dispute be included in their credit reports. This statement will be visible to future creditors or lenders, providing context regarding the unresolved issue. In the event of a continued dispute, South Dakota law provides consumers with additional avenues to protect their rights. One option is to file a complaint with the South Dakota Division of Banking. This governmental body has the authority to investigate complaints related to credit reporting agencies and provide appropriate remedies. Another avenue available to consumers is to seek legal representation to enforce their rights under the Fair Credit Reporting Act (FCRA). Attorneys specializing in credit dispute cases can guide consumers through the legal process, ensuring that their rights are upheld and any necessary legal action is taken. In summary, South Dakota recognizes the importance of protecting consumers' rights regarding disputed credit information. The investigation process aims to provide accurate credit reporting, and if disputes persist, individuals have the right to further recourse. It is crucial for consumers to understand their rights and the available avenues to ensure their credit information is accurate and fair.