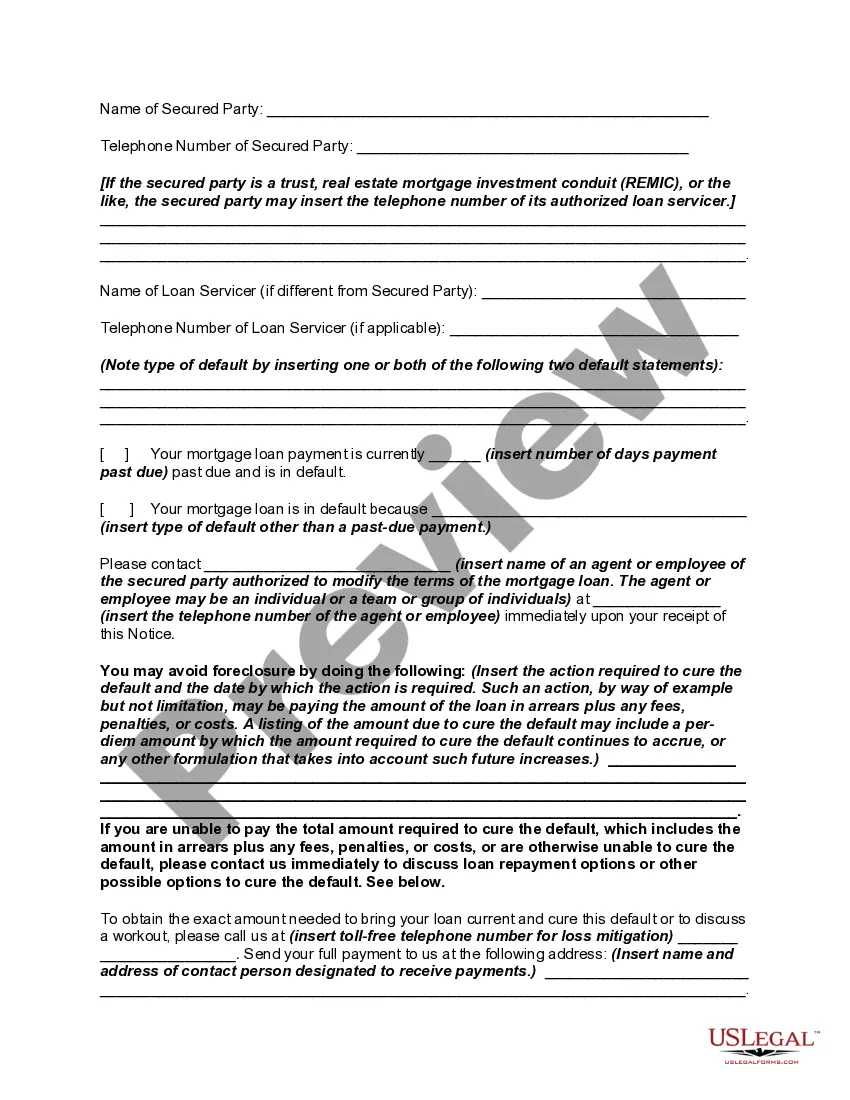

A number of states have enacted measures to facilitate greater communication between borrowers and lenders by requiring mortgage servicers to provide certain notices to defaulted borrowers prior to commencing a foreclosure action. The measures serve a dual purpose, providing more meaningful notice to borrowers of the status of their loans and slowing down the rate of foreclosures within these states. For instance, one state now requires a mortgagee to mail a homeowner a notice of intent to foreclose at least 45 days before initiating a foreclosure action on a loan. The notice must be in writing, and must detail all amounts that are past due and any itemized charges that must be paid to bring the loan current, inform the homeowner that he or she may have options as an alternative to foreclosure, and provide contact information of the servicer, HUD-approved foreclosure counseling agencies, and the state Office of Commissioner of Banks.

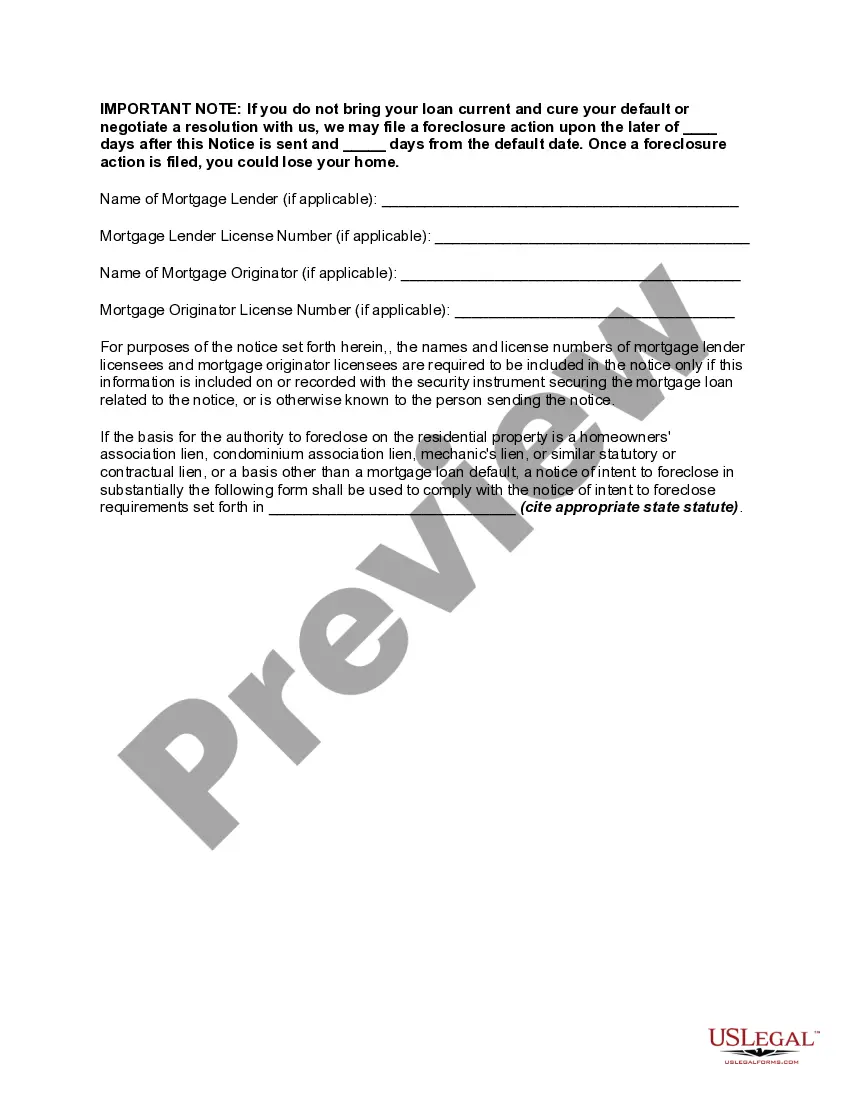

Title: South Dakota Notice of Intent to Foreclose — Mortgage Loan Default: A Comprehensive Guide Introduction: In South Dakota, when a homeowner defaults on their mortgage loan, the lender may initiate foreclosure proceedings. This process begins with the issuance of a Notice of Intent to Foreclose, informing the borrower of their default and their lender's intention to initiate foreclosure proceedings. This article will provide a detailed description of what a South Dakota Notice of Intent to Foreclose — Mortgage Loan Default entails, along with its key components and significant legal implications. 1. Understanding the South Dakota Notice of Intent to Foreclose: A South Dakota Notice of Intent to Foreclose is a legal document that serves as a warning to the borrower about the lender's plan to initiate foreclosure proceedings due to mortgage loan default. Lenders are legally obligated to provide this notice to borrowers before commencing foreclosure actions. It is an essential step in the foreclosure process, designed to provide borrowers with an opportunity to rectify the default and potentially avoid foreclosure. 2. Key components of the South Dakota Notice of Intent to Foreclose: i. Borrower's identification: The notice will clearly identify the borrower by their name, address, and contact information. ii. Lender's identification: The lender's name, address, and contact information will be prominently mentioned in the notice. iii. Loan details: The notice will include specific information about the mortgage loan, such as the loan amount, terms, and payment history. iv. Default details: The notice will outline the reasons for default, including missed payments, late payments, or violation of loan terms. v. Cure period: The notice will specify a cure period during which the borrower can remedy the default by paying the overdue amount and any additional fees. vi. Consequences: The notice will clearly state the potential consequences of failing to cure the default within the prescribed period, which may include foreclosure and loss of the property. vii. Contact details: The notice will provide contact details for the lender's representative who can assist the borrower in resolving the default or answer queries related to the foreclosure process. 3. Types of South Dakota Notice of Intent to Foreclose: While there may not be different types of South Dakota Notices of Intent to Foreclose, variations can occur in accordance with specific circumstances and loan agreements. Some alternative versions may include notices related to: i. Acceleration Clauses: If acceleration clauses exist within the loan agreement, the notice may include specific information regarding the acceleration of the entire loan amount due to default. ii. Redemption Rights: Notices may differ if the borrower is entitled to redemption rights, providing them with the opportunity to redeem the property even after foreclosure proceedings have commenced. iii. Deed in Lieu of Foreclosure: In some cases, lenders may offer borrowers the option to avoid foreclosure by executing a Deed in Lieu of Foreclosure, wherein the borrower surrenders the property to the lender voluntarily. Conclusion: When facing a South Dakota Notice of Intent to Foreclose — Mortgage Loan Default, it is important for borrowers to understand the implications and take appropriate action within the stipulated cure period. Seeking legal counsel and communicating with the lender can help explore options and possibly avoid foreclosure. Proper understanding and timely action are vital to protect homeownership rights and navigate the challenging foreclosure process in South Dakota.Title: South Dakota Notice of Intent to Foreclose — Mortgage Loan Default: A Comprehensive Guide Introduction: In South Dakota, when a homeowner defaults on their mortgage loan, the lender may initiate foreclosure proceedings. This process begins with the issuance of a Notice of Intent to Foreclose, informing the borrower of their default and their lender's intention to initiate foreclosure proceedings. This article will provide a detailed description of what a South Dakota Notice of Intent to Foreclose — Mortgage Loan Default entails, along with its key components and significant legal implications. 1. Understanding the South Dakota Notice of Intent to Foreclose: A South Dakota Notice of Intent to Foreclose is a legal document that serves as a warning to the borrower about the lender's plan to initiate foreclosure proceedings due to mortgage loan default. Lenders are legally obligated to provide this notice to borrowers before commencing foreclosure actions. It is an essential step in the foreclosure process, designed to provide borrowers with an opportunity to rectify the default and potentially avoid foreclosure. 2. Key components of the South Dakota Notice of Intent to Foreclose: i. Borrower's identification: The notice will clearly identify the borrower by their name, address, and contact information. ii. Lender's identification: The lender's name, address, and contact information will be prominently mentioned in the notice. iii. Loan details: The notice will include specific information about the mortgage loan, such as the loan amount, terms, and payment history. iv. Default details: The notice will outline the reasons for default, including missed payments, late payments, or violation of loan terms. v. Cure period: The notice will specify a cure period during which the borrower can remedy the default by paying the overdue amount and any additional fees. vi. Consequences: The notice will clearly state the potential consequences of failing to cure the default within the prescribed period, which may include foreclosure and loss of the property. vii. Contact details: The notice will provide contact details for the lender's representative who can assist the borrower in resolving the default or answer queries related to the foreclosure process. 3. Types of South Dakota Notice of Intent to Foreclose: While there may not be different types of South Dakota Notices of Intent to Foreclose, variations can occur in accordance with specific circumstances and loan agreements. Some alternative versions may include notices related to: i. Acceleration Clauses: If acceleration clauses exist within the loan agreement, the notice may include specific information regarding the acceleration of the entire loan amount due to default. ii. Redemption Rights: Notices may differ if the borrower is entitled to redemption rights, providing them with the opportunity to redeem the property even after foreclosure proceedings have commenced. iii. Deed in Lieu of Foreclosure: In some cases, lenders may offer borrowers the option to avoid foreclosure by executing a Deed in Lieu of Foreclosure, wherein the borrower surrenders the property to the lender voluntarily. Conclusion: When facing a South Dakota Notice of Intent to Foreclose — Mortgage Loan Default, it is important for borrowers to understand the implications and take appropriate action within the stipulated cure period. Seeking legal counsel and communicating with the lender can help explore options and possibly avoid foreclosure. Proper understanding and timely action are vital to protect homeownership rights and navigate the challenging foreclosure process in South Dakota.