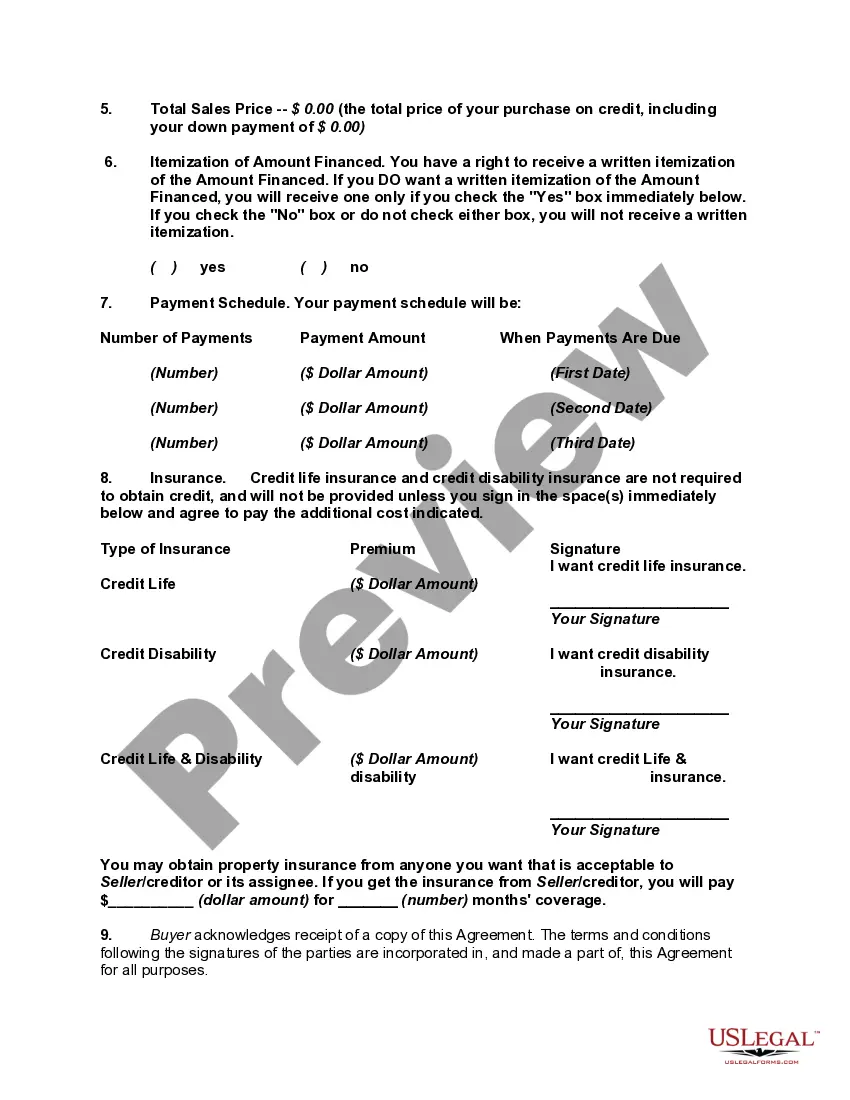

Disclosure of credit terms should have the content and form required under the federal Truth in Lending Act (15 U.S.C.A. §§ 1601 et seq.) and applicable regulations (Regulation Z, 12 C.F.R. § 226), and under state consumer credit laws to the extent that they differ from the federal Act. In connection with specified installment sales and other consumer credit transactions, these enactments require written disclosure and advice as to finance charges, annual percentage rates and other matters relating to credit. Under the federal Act, the disclosures may be set forth in the contract document itself or in a separate statement or statements.

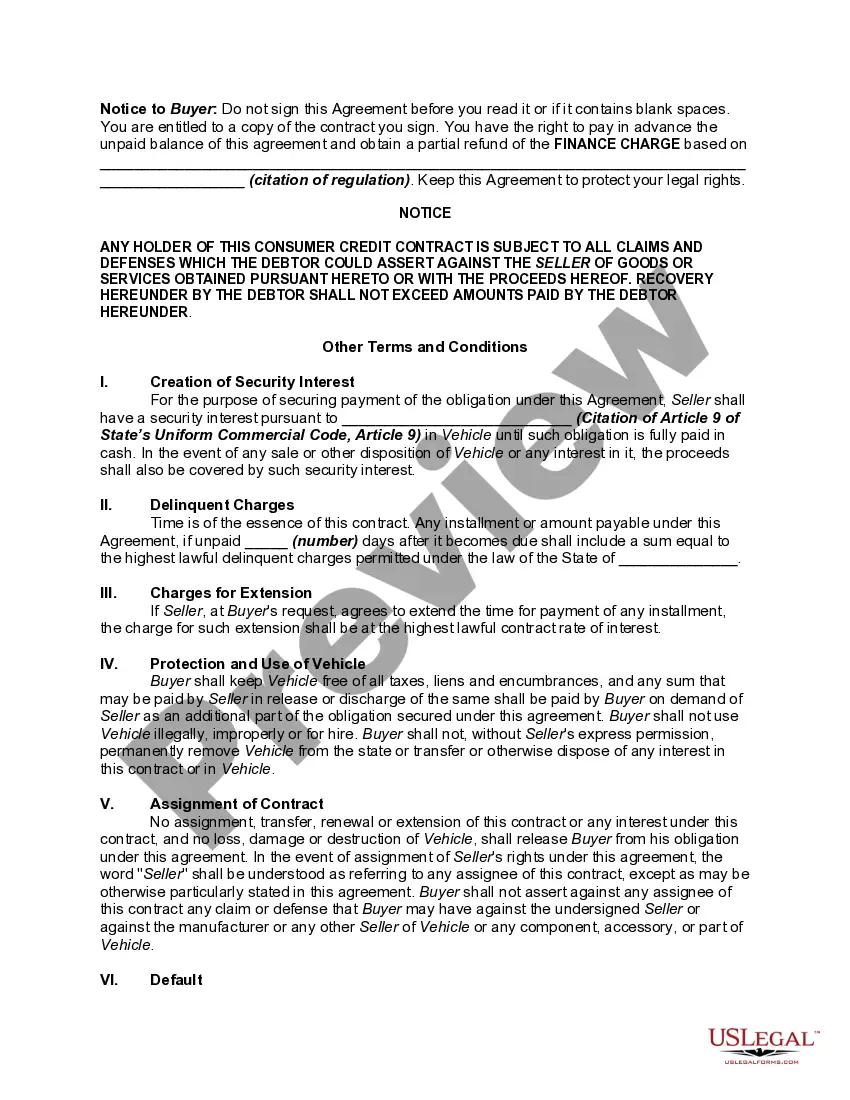

A federal notice regarding preservation of the consumer's claims and defenses is required on all consumer credit contracts by Federal Trade Commission regulation. 16 C.F.R. § 433.2. The notice must appear in 10-point bold type or print and must be worded as set forth in the above form.

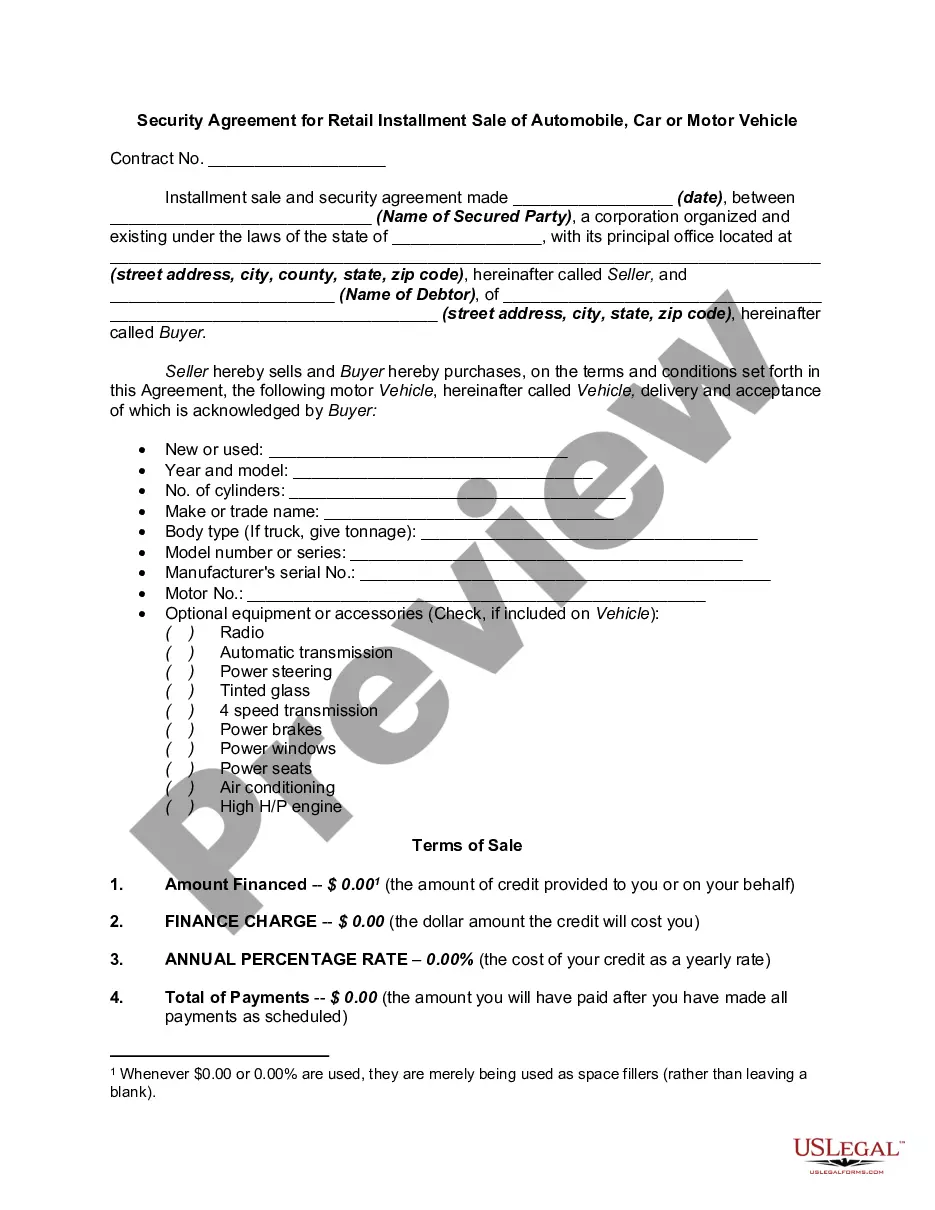

The South Dakota Security Agreement for Retail Installment Sale of Automobile, Car, or Motor Vehicle is a legal document that serves to protect the financial interest of the lender or creditor in a retail installment sale transaction. This agreement ensures that the lender has a security interest in the vehicle being purchased, providing them with the right to repossess the vehicle if the borrower defaults on their payment obligations. Keywords: South Dakota Security Agreement, Retail Installment Sale, Automobile, Car, Motor Vehicle, legal document, financial interest, lender, creditor, retail installment sale transaction, security interest, repossess, borrower, payment obligations. There are different types of South Dakota Security Agreements for Retail Installment Sale of Automobile, Car, or Motor Vehicle, including: 1. Traditional Security Agreement: This is the standard form used in most retail installment sales. It outlines the terms and conditions of the agreement, including the purchase price, interest rate, payment schedule, and consequences of default. 2. Balloon Payment Security Agreement: This type of agreement allows the borrower to make lower monthly payments throughout the loan term, with a large final payment (balloon payment) due at the end. The lender retains a security interest in the vehicle until the final payment is made. 3. Lease Agreement with Option to Purchase: In this arrangement, the borrower leases the vehicle for a certain period with an option to purchase it at the end of the lease term. The security agreement protects the lender's interest in the vehicle during the lease period and outlines the terms of the purchase option. 4. Conditional Sales Contract: This agreement is similar to a traditional security agreement but includes a condition that specifies the transfer of ownership to the borrower only after fulfilling all payment obligations. Until then, the lender has a security interest in the vehicle. 5. Chattel Mortgage Agreement: This type of security agreement is used when the borrower uses the vehicle as collateral for the loan. If the borrower defaults on the payments, the lender has the right to seize and sell the vehicle to recoup their losses. By utilizing these various types of South Dakota Security Agreements for Retail Installment Sale of Automobile, Car, or Motor Vehicle, lenders and borrowers can establish clear terms and protect their interests during the purchase and financing process.