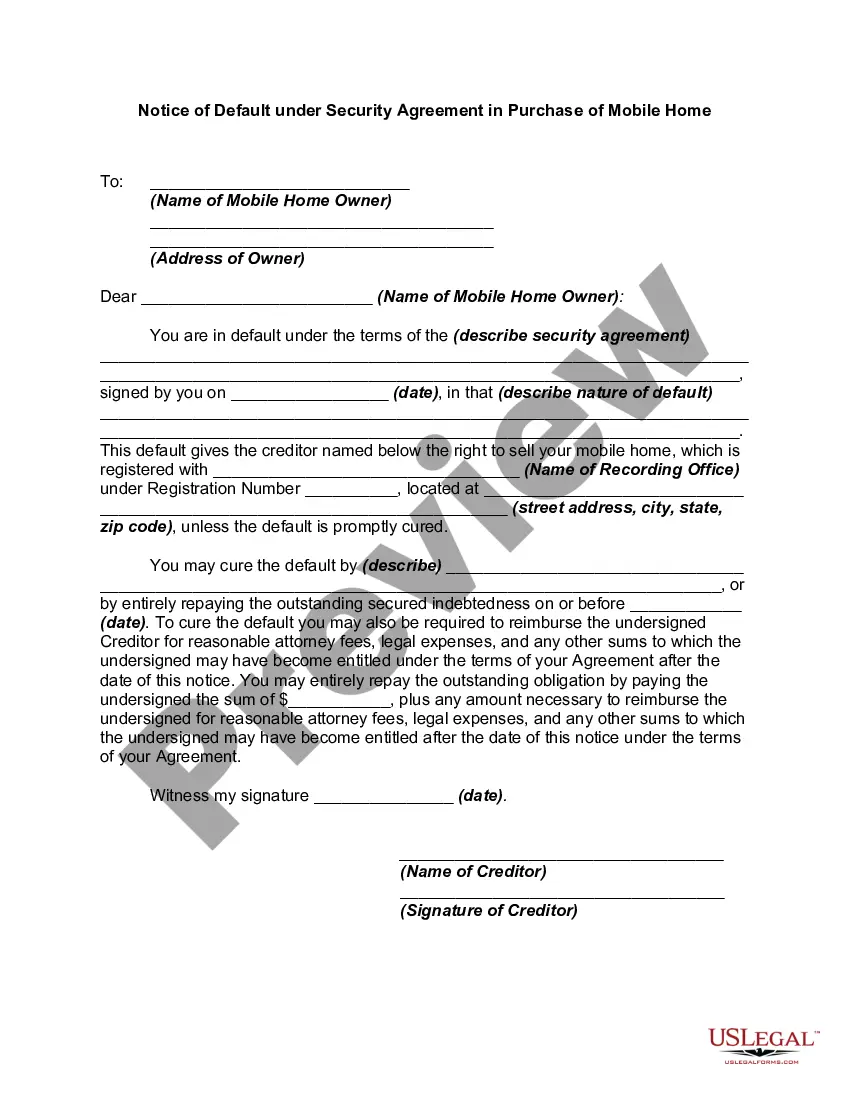

A South Dakota Notice of Default under Security Agreement in Purchase of Mobile Home is a legal document that notifies the borrower of their default on loan repayments for a mobile home purchase. This document is crucial in protecting the rights of the lender and initiating the necessary legal actions to remedy the default situation. The Notice of Default generally includes the following key information: 1. Identification details: It begins with the name and contact information of both parties involved in the agreement — the lender (secured party) and the borrower (debtor). 2. Description of the mobile home: The document specifies the mobile home's details, such as the make, model, year, vehicle identification number (VIN), and the physical address where it is located. 3. Loan details: This section outlines the terms and conditions of the loan, including the original loan amount, interest rate, repayment schedule, and any additional charges or fees. 4. Default clause: Here, the specific language of the default is detailed, specifying the exact condition(s) that the borrower has failed to meet. This can include failure to repay installments, neglecting insurance requirements, or breaching other contractual obligations. 5. Amount owed: The notice also states the total amount the borrower owes as a result of the default, which may include outstanding loan principal, accrued interest, late payment fees, legal fees, and any other related expenses. 6. Cure period: There is usually a cure period mentioned, allowing the borrower a specific period (usually 30 days) to rectify the default by catching up on missed payments. If the borrower fails to cure the default within the specified timeframe, additional legal actions may be taken by the lender. While there may not be different types of South Dakota Notice of Default under Security Agreement in Purchase of Mobile Home, variations might exist based on the specific terms of the purchase agreement or loan contract. It is important to seek legal advice or consult an attorney experienced in South Dakota property law when creating or responding to a Notice of Default under Security Agreement in Purchase of Mobile Home, as the requirements and procedures may vary.

South Dakota Notice of Default under Security Agreement in Purchase of Mobile Home

Description

How to fill out South Dakota Notice Of Default Under Security Agreement In Purchase Of Mobile Home?

If you want to comprehensive, download, or produce legitimate papers themes, use US Legal Forms, the most important variety of legitimate types, which can be found on-line. Take advantage of the site`s basic and practical lookup to obtain the paperwork you will need. Various themes for enterprise and personal functions are sorted by types and suggests, or key phrases. Use US Legal Forms to obtain the South Dakota Notice of Default under Security Agreement in Purchase of Mobile Home within a few click throughs.

Should you be previously a US Legal Forms consumer, log in to the account and click the Download button to find the South Dakota Notice of Default under Security Agreement in Purchase of Mobile Home. You may also accessibility types you earlier saved from the My Forms tab of your respective account.

Should you use US Legal Forms the very first time, follow the instructions listed below:

- Step 1. Make sure you have chosen the form for that proper area/land.

- Step 2. Take advantage of the Preview solution to examine the form`s information. Don`t forget about to learn the outline.

- Step 3. Should you be not satisfied using the form, utilize the Lookup industry at the top of the display to find other variations of the legitimate form design.

- Step 4. When you have found the form you will need, click the Acquire now button. Opt for the pricing prepare you like and put your references to sign up for an account.

- Step 5. Process the purchase. You can utilize your credit card or PayPal account to complete the purchase.

- Step 6. Choose the structure of the legitimate form and download it on your device.

- Step 7. Full, modify and produce or sign the South Dakota Notice of Default under Security Agreement in Purchase of Mobile Home.

Each and every legitimate papers design you purchase is your own property for a long time. You possess acces to each and every form you saved within your acccount. Click on the My Forms segment and select a form to produce or download yet again.

Remain competitive and download, and produce the South Dakota Notice of Default under Security Agreement in Purchase of Mobile Home with US Legal Forms. There are millions of professional and condition-certain types you can use for your enterprise or personal demands.