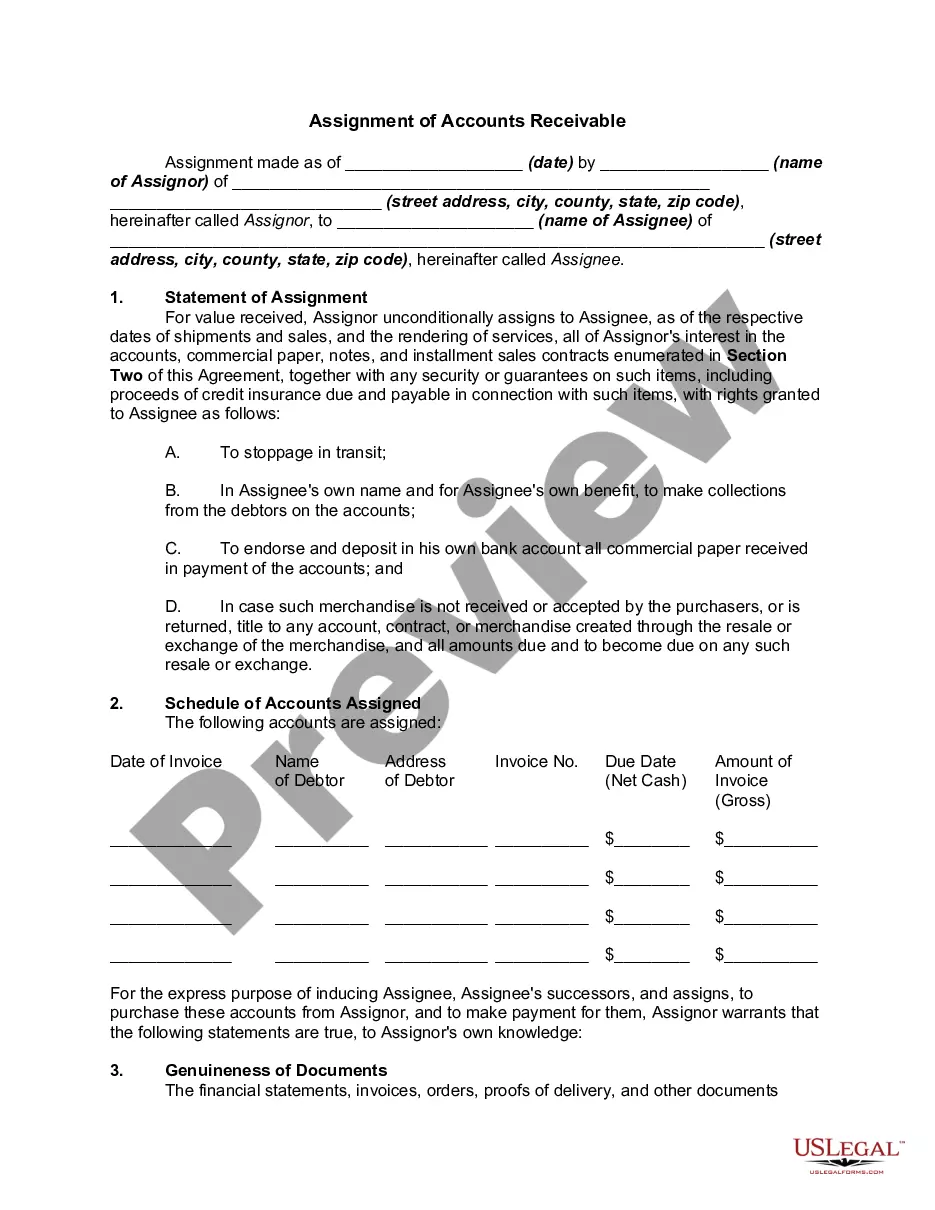

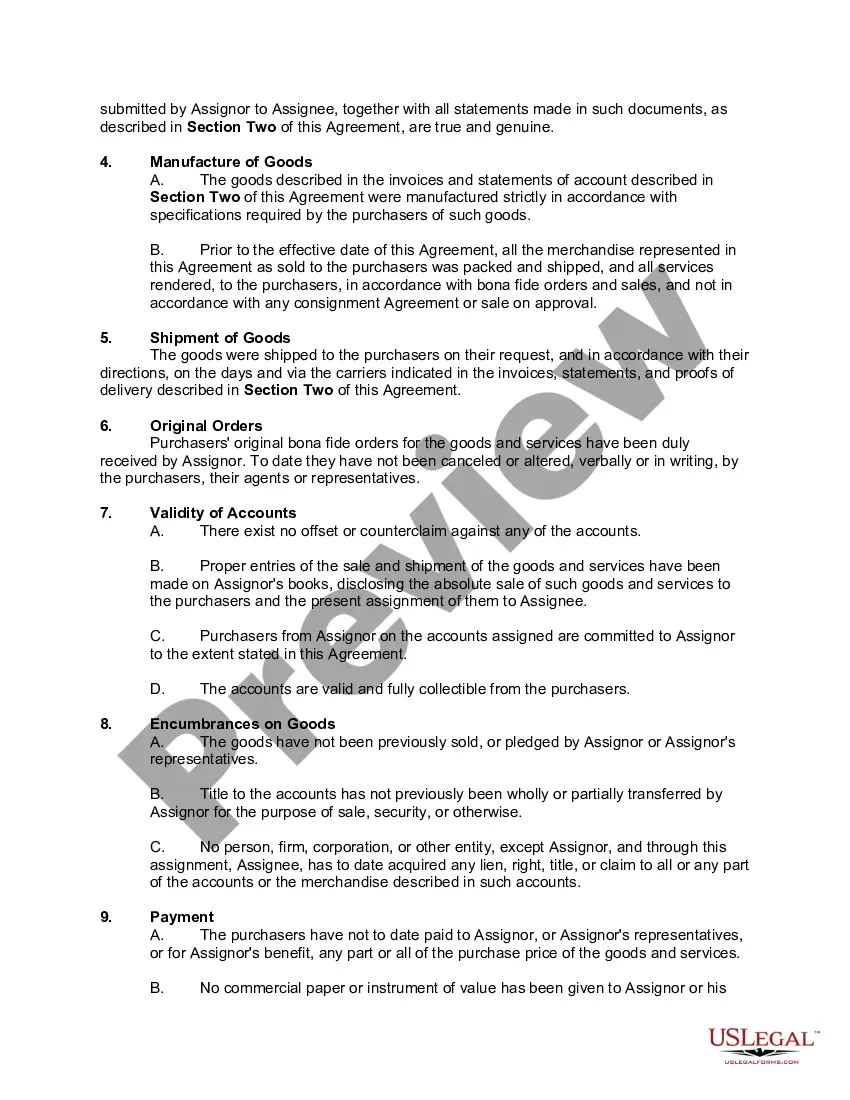

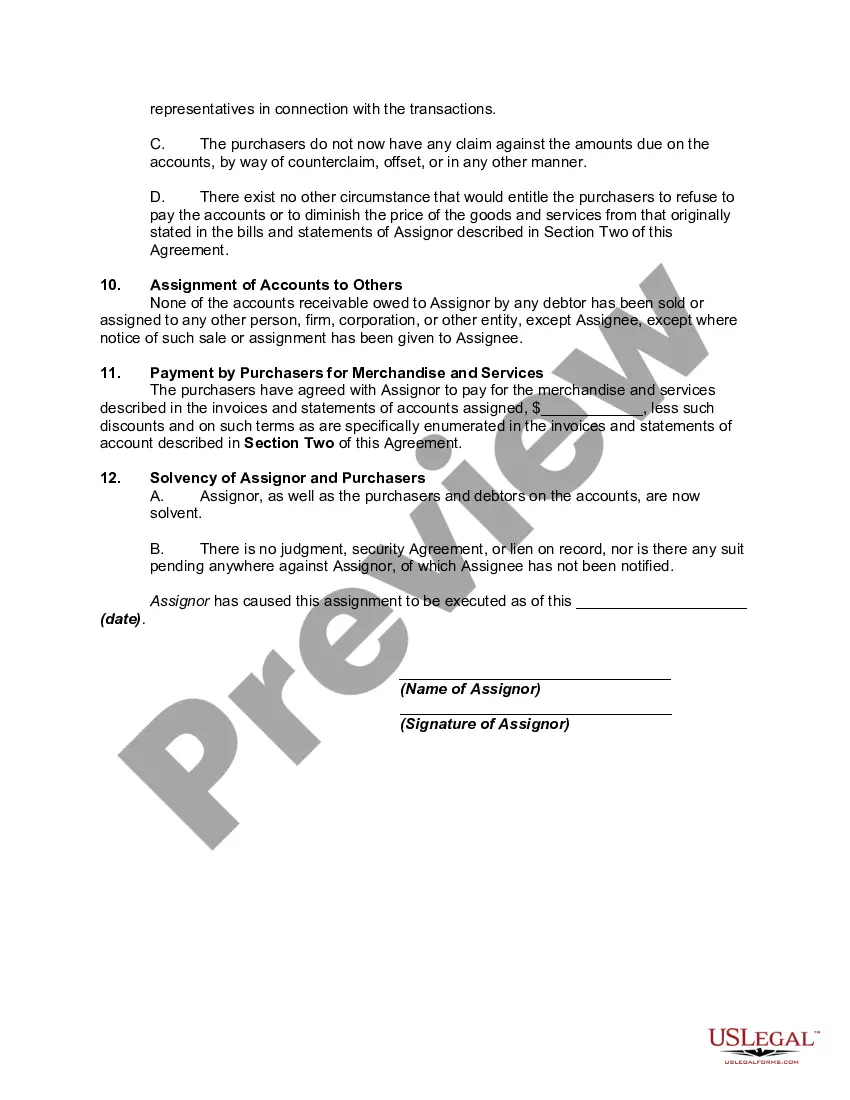

South Dakota Assignment of Accounts Receivable is a legal document utilized in business transactions where a company permanently transfers its accounts receivable to another party, known as the assignee. This assignment aims to provide immediate cash flow to the assigning company in exchange for the future collection of these accounts receivable by the assignee. In South Dakota, there are two primary types of Assignment of Accounts Receivable: 1. Absolute Assignment of Accounts Receivable: This type of assignment involves a complete transfer of ownership and rights over the accounts receivable. The assigning company has no further claim or control over the assigned accounts receivable once the assignment is made. The assignee assumes all responsibilities and entitlements associated with collecting the debts. 2. Collateral Assignment of Accounts Receivable: This type of assignment is more commonly used to secure a debt or loan. The assigning company pledges its accounts receivable as collateral without fully transferring ownership to the assignee. In case of default, the assignee obtains the right to collect debt from the assigned accounts receivable to recover the loan amount. It is important to note that when conducting an Assignment of Accounts Receivable in South Dakota, companies must comply with the state's specific laws and regulations governing such transactions. The Uniform Commercial Code (UCC), particularly Article 9, provides the legal framework for assignments and sets guidelines for required documentation and notification procedures. The South Dakota Assignment of Accounts Receivable document should include comprehensive information about the assigning company, the assignee, the assigned accounts receivable, and any terms and conditions agreed upon. The document should be signed by authorized representatives of both parties involved to ensure its validity. By utilizing a South Dakota Assignment of Accounts Receivable, businesses can effectively manage their cash flow needs, access immediate funds, and reduce the risk associated with outstanding receivables. This legal instrument can provide financial stability to companies by converting their accounts receivable into liquid assets, allowing them to meet their operational goals and obligations.

South Dakota Assignment of Accounts Receivable

Description

How to fill out South Dakota Assignment Of Accounts Receivable?

It is possible to invest hrs on the web looking for the legitimate document template which fits the state and federal needs you require. US Legal Forms gives a large number of legitimate varieties that happen to be reviewed by specialists. It is simple to download or printing the South Dakota Assignment of Accounts Receivable from my services.

If you have a US Legal Forms bank account, you are able to log in and then click the Obtain switch. Next, you are able to comprehensive, change, printing, or indicator the South Dakota Assignment of Accounts Receivable. Every legitimate document template you purchase is yours eternally. To get one more backup of any purchased develop, visit the My Forms tab and then click the related switch.

If you are using the US Legal Forms internet site for the first time, follow the easy directions listed below:

- First, make certain you have chosen the proper document template for that state/metropolis of your choice. Read the develop description to make sure you have selected the correct develop. If accessible, take advantage of the Review switch to appear with the document template also.

- In order to locate one more variation in the develop, take advantage of the Look for area to find the template that meets your requirements and needs.

- After you have found the template you want, click Buy now to carry on.

- Select the pricing plan you want, enter your references, and register for a merchant account on US Legal Forms.

- Comprehensive the financial transaction. You can use your charge card or PayPal bank account to fund the legitimate develop.

- Select the structure in the document and download it in your product.

- Make adjustments in your document if needed. It is possible to comprehensive, change and indicator and printing South Dakota Assignment of Accounts Receivable.

Obtain and printing a large number of document themes making use of the US Legal Forms Internet site, that offers the biggest collection of legitimate varieties. Use expert and condition-distinct themes to handle your company or person demands.