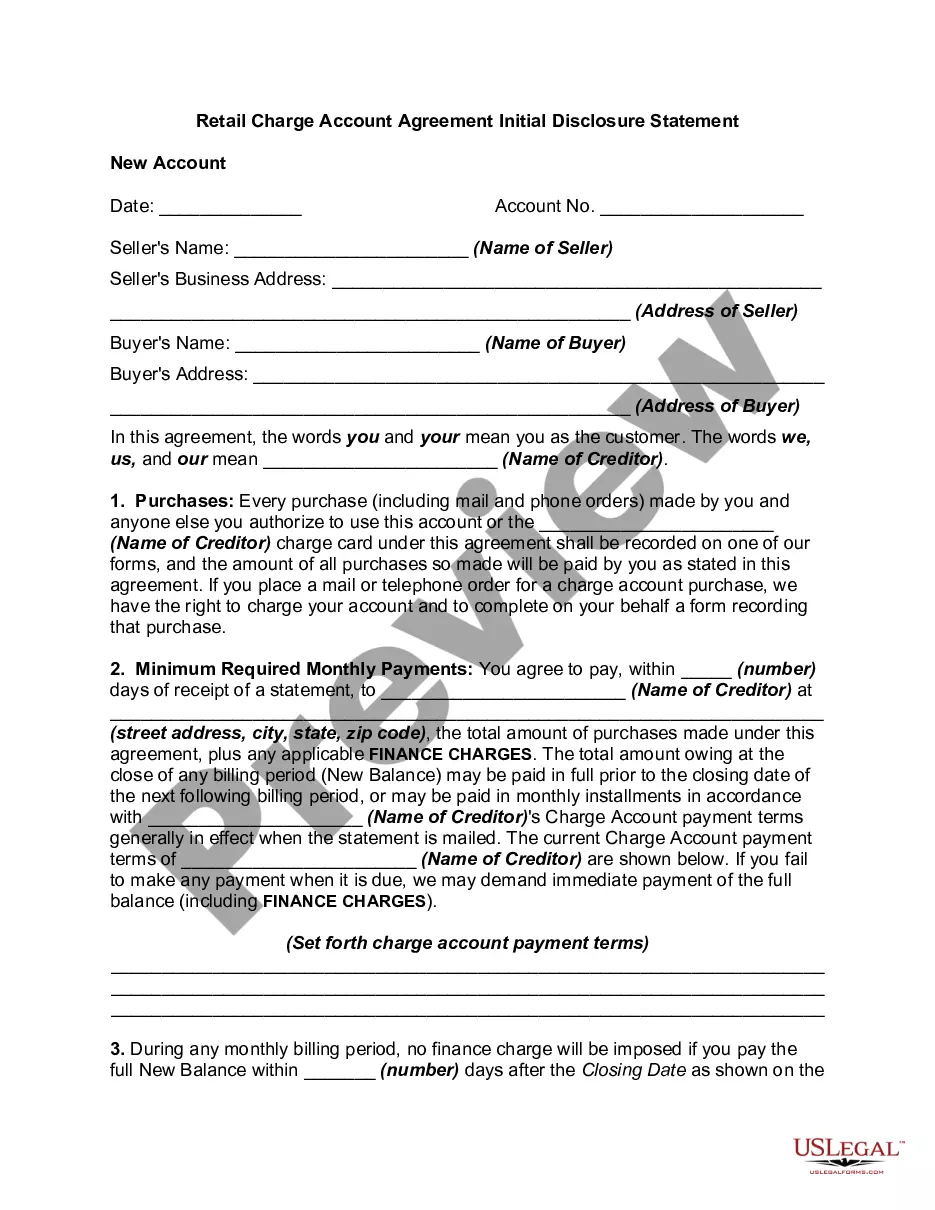

South Dakota Charge Account Terms and Conditions

Description

How to fill out Charge Account Terms And Conditions?

Have you been in the place where you will need papers for sometimes enterprise or personal functions virtually every working day? There are plenty of legitimate document web templates available online, but discovering ones you can rely is not simple. US Legal Forms provides thousands of develop web templates, much like the South Dakota Charge Account Terms and Conditions, that happen to be created in order to meet state and federal demands.

If you are previously familiar with US Legal Forms internet site and possess a merchant account, basically log in. Afterward, you may download the South Dakota Charge Account Terms and Conditions format.

If you do not offer an profile and want to begin to use US Legal Forms, adopt these measures:

- Discover the develop you require and make sure it is for your appropriate metropolis/region.

- Utilize the Preview option to review the form.

- Look at the description to actually have selected the proper develop.

- If the develop is not what you are searching for, take advantage of the Search discipline to get the develop that fits your needs and demands.

- Once you get the appropriate develop, simply click Purchase now.

- Choose the rates plan you would like, fill in the specified information and facts to generate your bank account, and pay money for the transaction with your PayPal or credit card.

- Pick a convenient paper structure and download your version.

Get all the document web templates you have purchased in the My Forms menu. You can get a more version of South Dakota Charge Account Terms and Conditions whenever, if necessary. Just go through the necessary develop to download or print the document format.

Use US Legal Forms, probably the most extensive collection of legitimate varieties, to save lots of time and avoid faults. The service provides professionally produced legitimate document web templates that you can use for an array of functions. Generate a merchant account on US Legal Forms and commence making your lifestyle easier.

Form popularity

FAQ

Living in South Dakota comes with tax benefits like not having to pay state income tax and favorable requirements for small-scale businesses. South Dakota is considered the happiest State in America because its economy is one of the strongest in the country, giving small businesses the best environment for growth.

You must sign the deed and get your signature notarized, and then record (file) the deed with the county register of deeds office before your death. Otherwise, it won't be valid. You can make a South Dakota transfer on death deed with WillMaker.

SOUTH DAKOTA A judgment becomes a lien on real property for a period of 10 years. S.D. Codified Laws § 15-16-7. A judgment may be renewed for an additional period of ten years.

In South Dakota, when a person dies without leaving a will, the surviving spouse is entitled to receive the entire intestate estate unless the decedent was survived by descendants of a prior marriage or other relationship, in which event, the spouse receives $100,000.00 plus half of the remaining estate, plus certain ...

Our iconic attractions include Mount Rushmore National Memorial, Badlands National Park, the Black Hills and the Missouri River. On top of that, we have abundant state parks, lakes and trails. Beyond that, we have some of the nation's best hunting and fishing. It's the complete package.

Unmarried Individuals Without Children in South Dakota Inheritance Law Intestate Succession: Extended FamilyChildren, but unmarriedEntire estate to childrenParents, but no spouse, children, or siblingsEntire estate to parentsParents are deceased, and no spouse or childrenEntire estate goes to siblings.1 more row ?

21-5-3. Limitation of actions. Every action for wrongful death shall be commenced within three years after the death of such deceased person.

29A-6-416. Beneficiary takes property subject to all interests present at transferor's death. Subject to chapter 43-28, a beneficiary takes the property subject to all conveyances, encumbrances, assignments, contracts, mortgages, liens, and other interests to which the property is subject at the transferor's death.