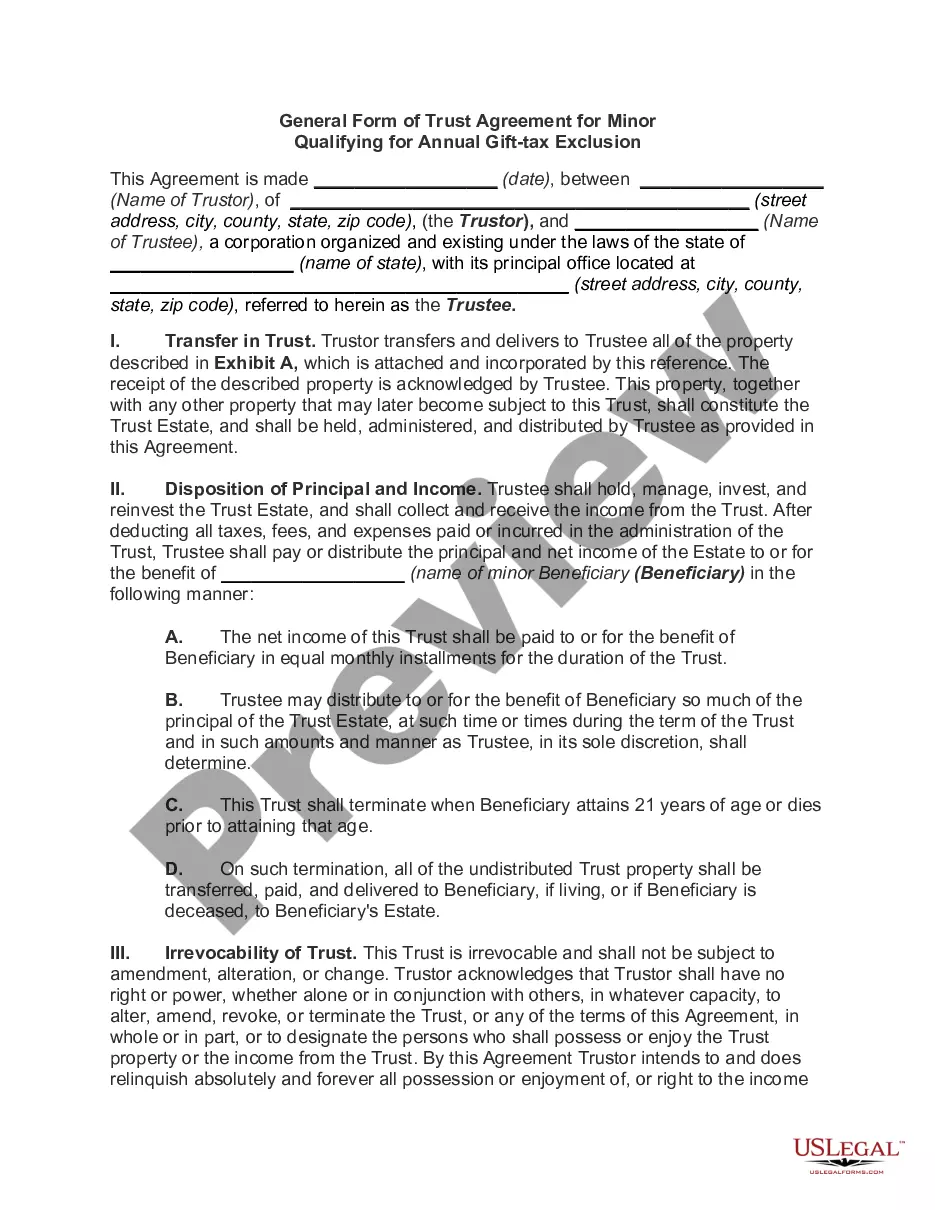

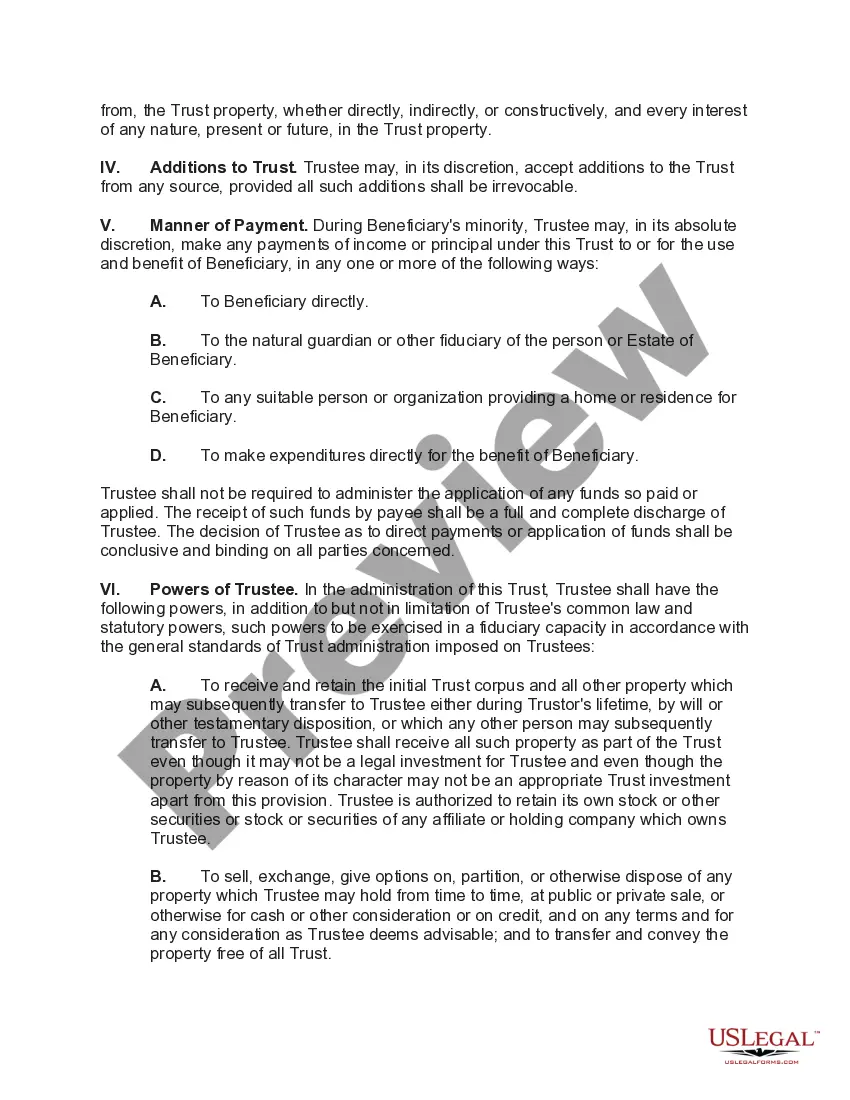

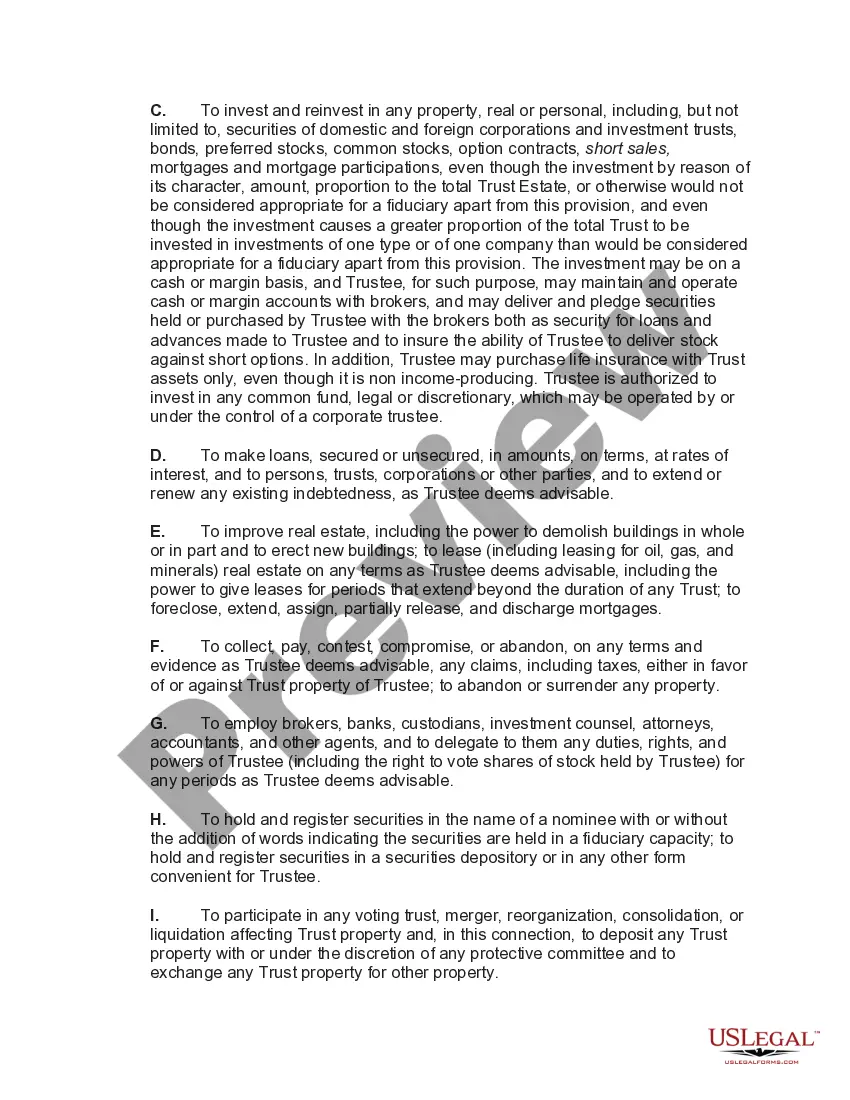

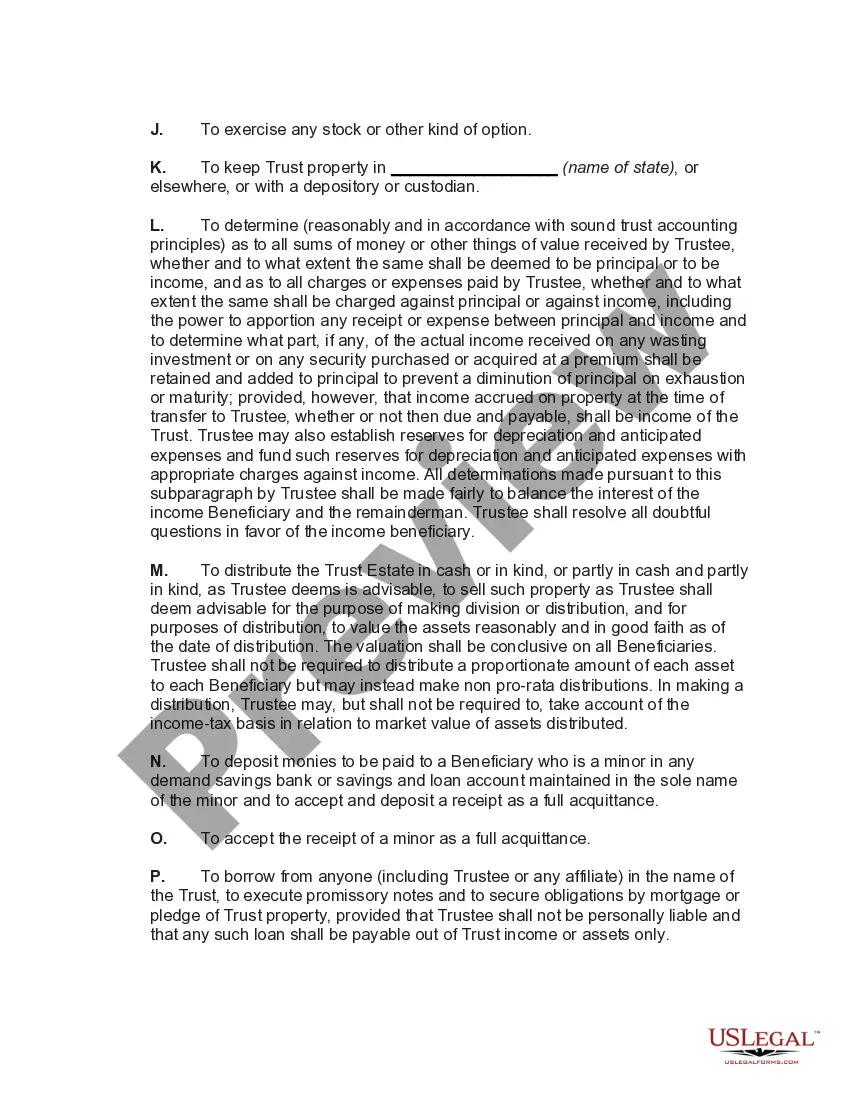

South Dakota General Form of Trust Agreement for Minor Qualifying for Annual Gift Tax Exclusion is a legal document that establishes a trust for the benefit of a minor, while also helping the granter qualify for the annual gift tax exclusion. This type of trust in South Dakota can have various variations and names, including: 1. South Dakota Irrevocable Trust for Minor Qualifying for Annual Gift Tax Exclusion: This form of trust is designed to be permanent and cannot be amended or revoked by the granter once established. It allows the granter to make gifts to the trust for the benefit of a minor child or grandchild, while also reducing potential gift tax liabilities. 2. South Dakota Revocable Trust for Minor Qualifying for Annual Gift Tax Exclusion: Unlike the irrevocable trust, this type of trust allows the granter to retain the power to amend or revoke the trust during their lifetime. However, once the granter passes away, the trust becomes irrevocable. This trust also helps the granter qualify for the annual gift tax exclusion while benefiting a minor. 3. South Dakota Testamentary Trust for Minor Qualifying for Annual Gift Tax Exclusion: This trust is established through a will and takes effect upon the granter's death. It allows the granter to leave assets to a minor beneficiary while also minimizing potential gift tax liabilities. Regardless of the specific type, the South Dakota General Form of Trust Agreement for Minor Qualifying for Annual Gift Tax Exclusion typically includes the following components: 1. Identification of the granter: The person establishing the trust and making gifts to it. 2. Designation of the trustee: The person or entity responsible for managing the trust and distributing assets to the minor beneficiary. 3. Naming the beneficiaries: The minor child or grandchild for whom the trust is being established. 4. Terms of the trust: Detailed provisions outlining how the trust assets will be managed, invested, and distributed for the minor's benefit. 5. Duration of the trust: Whether the trust is irrevocable or revocable, and if it has a predetermined end date or conditions for termination. 6. Tax considerations: Provisions ensuring the trust meets the requirements for annual gift tax exclusion, enabling the granter to maximize tax savings. 7. Contingency plans: Instructions for what happens to the trust assets if the designated trustee is unable or unwilling to fulfill their duties. 8. Signatures: Signatures of the granter, trustee, and witnesses, ensuring the document's legal validity.

South Dakota General Form of Trust Agreement for Minor Qualifying for Annual Gift Tax Exclusion

Description

How to fill out South Dakota General Form Of Trust Agreement For Minor Qualifying For Annual Gift Tax Exclusion?

If you wish to complete, acquire, or produce lawful record templates, use US Legal Forms, the greatest assortment of lawful types, that can be found on the web. Use the site`s simple and easy practical lookup to obtain the paperwork you will need. A variety of templates for business and individual functions are sorted by classes and states, or keywords and phrases. Use US Legal Forms to obtain the South Dakota General Form of Trust Agreement for Minor Qualifying for Annual Gift Tax Exclusion with a number of click throughs.

If you are currently a US Legal Forms client, log in to your accounts and then click the Acquire switch to have the South Dakota General Form of Trust Agreement for Minor Qualifying for Annual Gift Tax Exclusion. You can even access types you previously downloaded within the My Forms tab of the accounts.

If you work with US Legal Forms the first time, follow the instructions beneath:

- Step 1. Ensure you have chosen the shape for your correct metropolis/nation.

- Step 2. Use the Review option to check out the form`s articles. Don`t overlook to learn the information.

- Step 3. If you are unsatisfied with all the type, use the Research industry near the top of the screen to find other variations of the lawful type template.

- Step 4. Upon having found the shape you will need, select the Get now switch. Select the costs plan you choose and add your references to register on an accounts.

- Step 5. Method the financial transaction. You may use your Мisa or Ьastercard or PayPal accounts to accomplish the financial transaction.

- Step 6. Choose the file format of the lawful type and acquire it on the system.

- Step 7. Complete, revise and produce or indication the South Dakota General Form of Trust Agreement for Minor Qualifying for Annual Gift Tax Exclusion.

Every lawful record template you buy is the one you have forever. You may have acces to every type you downloaded with your acccount. Go through the My Forms portion and pick a type to produce or acquire once again.

Be competitive and acquire, and produce the South Dakota General Form of Trust Agreement for Minor Qualifying for Annual Gift Tax Exclusion with US Legal Forms. There are many skilled and status-particular types you may use to your business or individual needs.

Form popularity

FAQ

Section 2503(b) is also known as a Qualifying Minor's Trust or Mandatory Income Trust. This is an irrevocable trust which requires distribution of income on an annual basis. Most often, distributed funds are placed into a custodial bank account until the child reaches legal age.

The federal gift tax law provides that every person can give a present interest gift of up to $14,000 each year to any individual they want.

A gift in trust is a way to avoid taxes on gifts that exceed the annual gift tax exclusion amount. One type of gift in trust is a Crummey trust, which allows gifts to be given for a specific period, establishing the gifts as a present interest and eligible for the gift tax exclusion.

Gifts in trust do not qualify for the annual exclusion unless the trust either qualifies as a Minor's Trust under Internal Revenue Code Section 2503(c) or has certain temporary withdrawal powers called Crummey powers.

The trust allows the trustee to gift from the trust to the current beneficiary's issue up to the annual gift exclusion (currently $15K).

A 2503(c) trust, or minor's trust, is a trust established to hold gifts for one child until he or she attains age 21. A gift to this type of trust qualifies for the annual federal gift tax exclusion.

The trust allows the trustee to gift from the trust to the current beneficiary's issue up to the annual gift exclusion (currently $15K).

The key difference between a 2503(c) trust and a 2503(b) trust is the distribution requirement. Parents who are concerned about providing a child or other beneficiary with access to trust funds at age 21 might be better off with a 2503(b), since there is no requirement for access at age 21.

A Section 2503(c) trust allows all the principal and income to be used for the child until he reaches the age of 21, unlike the 2503(b) trust that extends beyond age 21 and requires income to be paid to the child annually. The trustee can pay the child's college expenses from the 2503(c) trust.

2503(c) trust has one beneficiary, and the assets in the trust are irrevocably his or hers (i.e., the assets cannot be redirected to another beneficiary); Because the trust is irrevocable, the grantor gives up total control of the assets; The trust income tax rates may penalize those trusts that accumulate income; and.