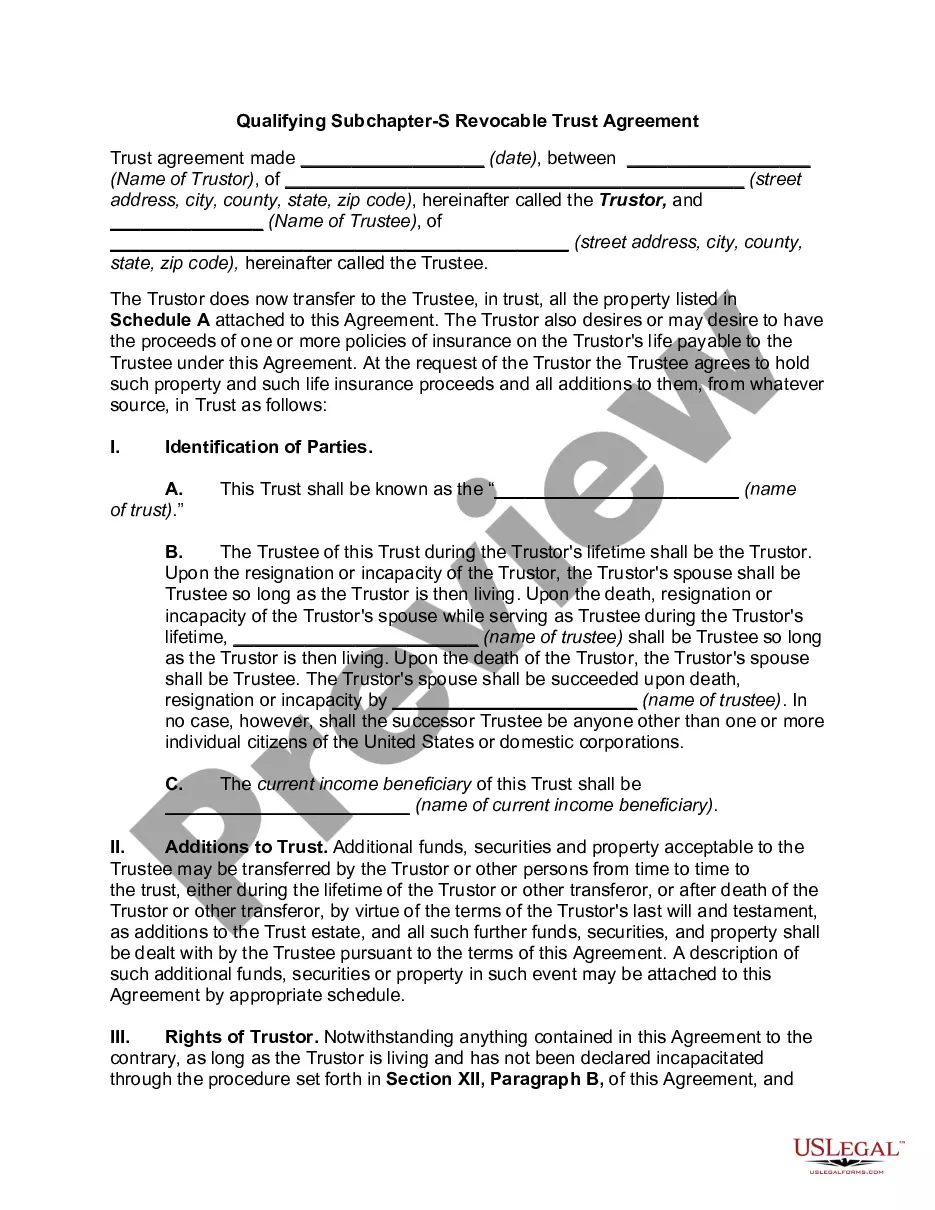

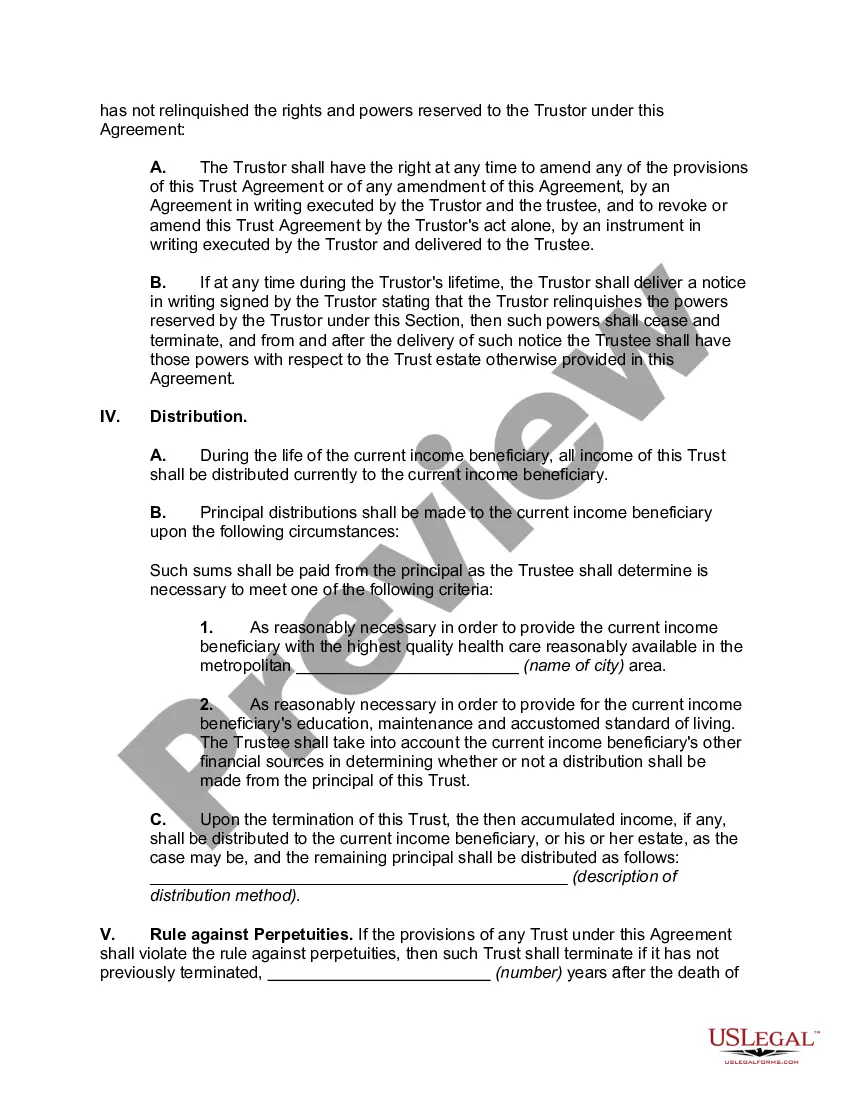

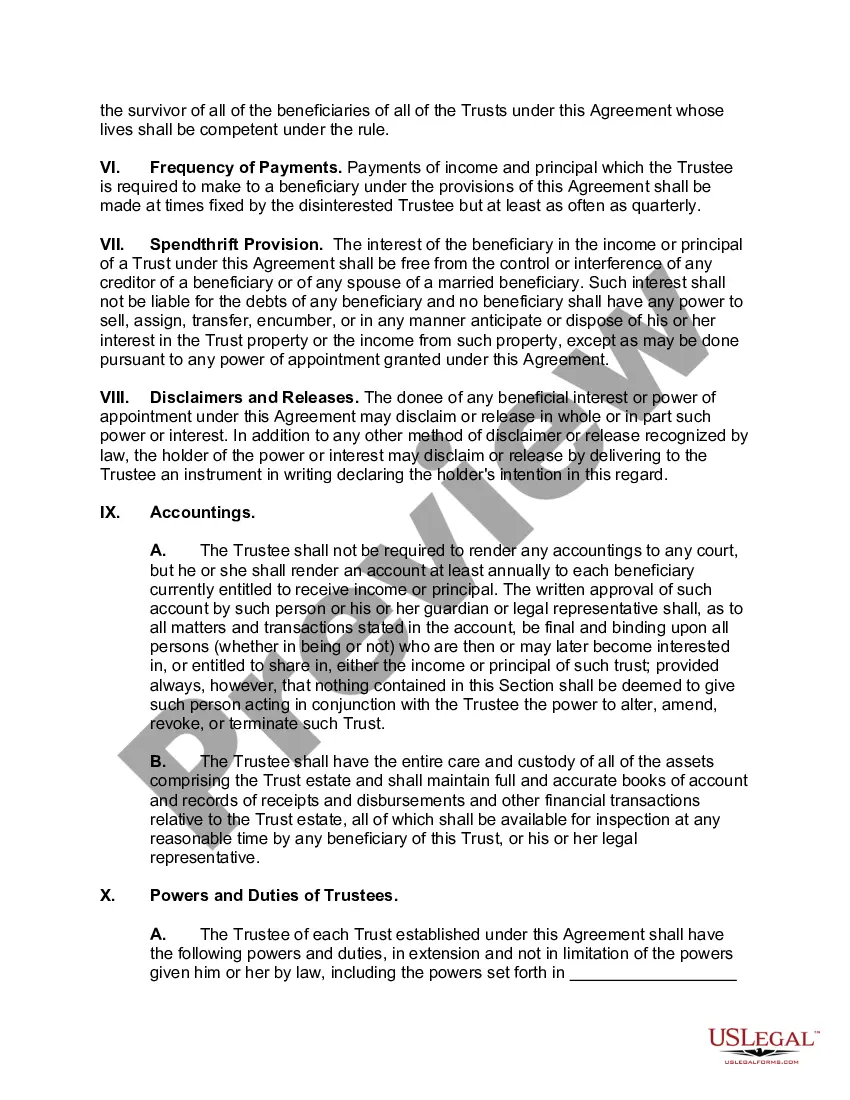

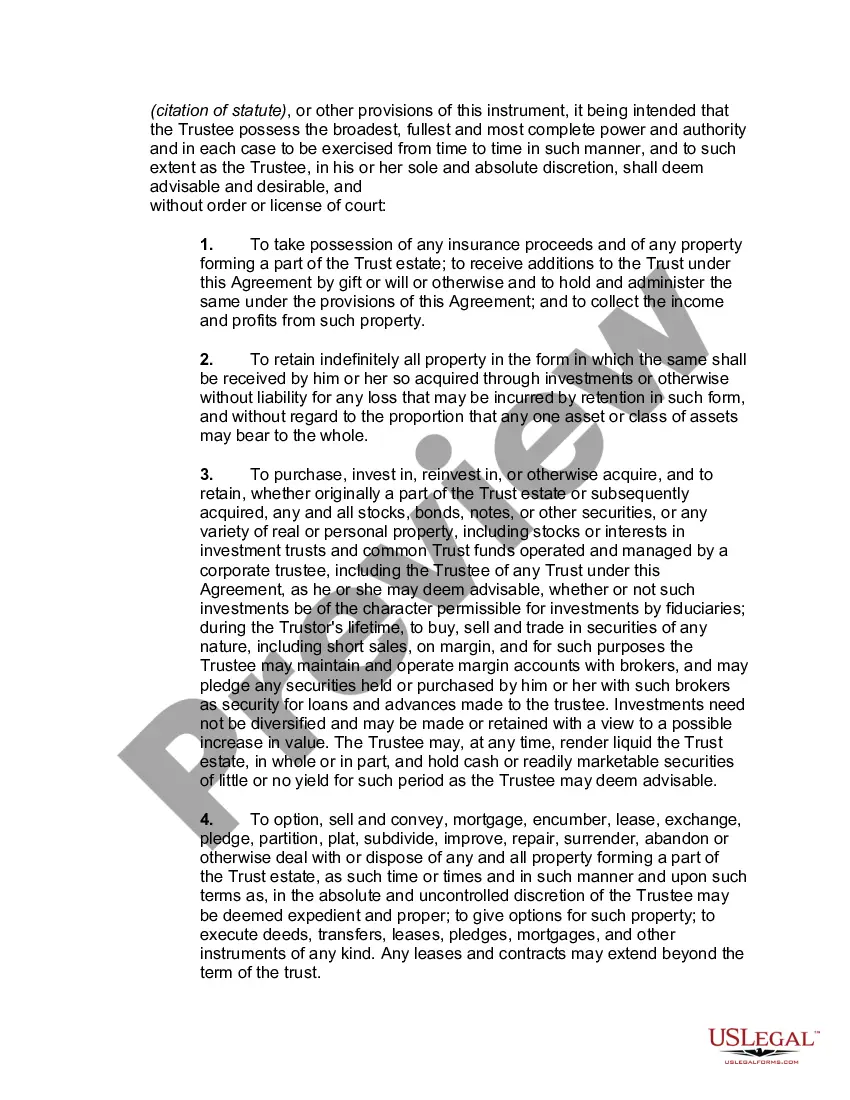

A South Dakota Qualifying Subchapter-S Revocable Trust Agreement is a legal document that serves as a crucial estate planning tool for individuals or families who have chosen to establish a trust structure under the subchapter S rules of the Internal Revenue Code. This specific type of trust is designed to qualify as an S corporation shareholder, allowing the trust to benefit from certain tax advantages and flexible income distribution options. It is important to note that South Dakota is known for its favorable trust laws, making it an attractive jurisdiction for establishing this type of trust agreement. The South Dakota Qualifying Subchapter-S Revocable Trust Agreement primarily enables the granter (the person creating the trust) to maintain control and management over their assets during their lifetime while allowing for a smooth transfer of these assets upon their death. This agreement provides comprehensive directions for the management, distribution, and disposition of the trust assets, as well as detailed provisions outlining the powers and responsibilities of the trustee (the individual or entity appointed to administer the trust). Keywords relevant to the South Dakota Qualifying Subchapter-S Revocable Trust Agreement include: 1. Subchapter-S: Refers to the specific section of the Internal Revenue Code that allows small business corporations and certain trusts to be treated as pass-through entities for tax purposes. 2. Revocable Trust: Denotes a trust that can be modified, amended, or terminated by the granter during their lifetime. 3. Estate Planning: The process of arranging one's assets and affairs to ensure a seamless transfer of wealth to intended beneficiaries upon death while minimizing tax implications. 4. S Corporation: A type of legal business entity that combines the liability protection of a corporation with the pass-through taxation of a partnership. 5. Tax Advantages: Benefits that minimize tax liabilities, such as the avoidance of double taxation and the ability to pass income through to individual shareholders of the S corporation. 6. Asset Management: Refers to the administration, investment, and safeguarding of trust assets by the trustee to ensure growth and protection of the assets. 7. Income Distribution: The process of allocating income generated by the trust among the beneficiaries in accordance with the provisions laid out in the trust agreement. 8. Granter: The individual who creates the trust and transfers their assets into it. 9. Beneficiaries: The individuals or entities specified by the granter to receive the trust's assets or income. 10. Trustee: The person or entity appointed to manage the trust and carry out the granter's instructions. Different types of South Dakota Qualifying Subchapter-S Revocable Trust Agreements may include variations based on the unique circumstances, assets, and intentions of the granter. Examples may include the Family Revocable Trust Agreement, Charitable Revocable Trust Agreement, Special Needs Revocable Trust Agreement, or Business Succession Revocable Trust Agreement. Each of these variations tailors the trust's provisions to suit specific goals or beneficiaries while still qualifying as a Subchapter-S trust under South Dakota law.

South Dakota Qualifying Subchapter-S Revocable Trust Agreement

Description

How to fill out South Dakota Qualifying Subchapter-S Revocable Trust Agreement?

If you need to full, acquire, or printing legal file layouts, use US Legal Forms, the greatest assortment of legal kinds, which can be found on-line. Use the site`s easy and convenient lookup to get the files you require. Numerous layouts for business and personal purposes are sorted by categories and claims, or search phrases. Use US Legal Forms to get the South Dakota Qualifying Subchapter-S Revocable Trust Agreement in just a couple of clicks.

When you are presently a US Legal Forms buyer, log in to your profile and click on the Acquire switch to find the South Dakota Qualifying Subchapter-S Revocable Trust Agreement. You can even gain access to kinds you earlier delivered electronically inside the My Forms tab of the profile.

If you use US Legal Forms initially, refer to the instructions beneath:

- Step 1. Make sure you have chosen the shape to the correct metropolis/nation.

- Step 2. Utilize the Preview method to examine the form`s content material. Do not forget about to read the outline.

- Step 3. When you are unhappy with the kind, take advantage of the Research field towards the top of the display to find other types in the legal kind template.

- Step 4. Once you have identified the shape you require, select the Purchase now switch. Pick the costs strategy you favor and put your accreditations to register for an profile.

- Step 5. Method the purchase. You can utilize your credit card or PayPal profile to complete the purchase.

- Step 6. Select the format in the legal kind and acquire it in your gadget.

- Step 7. Comprehensive, change and printing or sign the South Dakota Qualifying Subchapter-S Revocable Trust Agreement.

Every legal file template you buy is your own property forever. You possess acces to every kind you delivered electronically with your acccount. Click on the My Forms area and choose a kind to printing or acquire again.

Contend and acquire, and printing the South Dakota Qualifying Subchapter-S Revocable Trust Agreement with US Legal Forms. There are many specialist and state-certain kinds you may use for the business or personal requires.

Form popularity

FAQ

Since a revocable trust is not treated as separate from the grantor, it is an eligible S corporation shareholder while the grantor is alive.

Net investment income tax of a QSST 1411(a)(2)). The tax also applies to QSSTs to the extent the net investment income is retained in the trust. Although the S corporation income of a QSST is taxed to the individual income beneficiary, capital gain on the sale of the S corporation stock is taxed at the trust level.

You can put your S-Corp into your living trust by simply transferring your shares ownership to yourself as trustee of your living trust, but again, there are certain procedures that must be strictly followed....These trusts include:Electing small business trusts (ESBT)Grantor trusts.Qualified subchapter S trusts (QSST)

You can put your S-Corp into your living trust by simply transferring your shares ownership to yourself as trustee of your living trust, but again, there are certain procedures that must be strictly followed....These trusts include:Electing small business trusts (ESBT)Grantor trusts.Qualified subchapter S trusts (QSST)

A trust can hold stock in an S corp only if it (1) is treated as owned by its grantor for income tax purposes under us grantor trust rules, (2) was a grantor trust immediately before its grantor's death (the trust can be a shareholder only for two years from that date), (3) received stock from the will of a decedent (

A Qualified Subchapter S Trust, commonly referred to as a QSST Election, or a Q-Sub election, is a Qualified Subchapter S Subsidiary Election made on behalf of a trust that retains ownership as the shareholder of an S corporation, a corporation in the United States which votes to be taxed.

Three commonly used types of ongoing trusts qualify as S corporation shareholders: grantor trusts, qualified subchapter S trusts (QSSTs) and electing small business trusts (ESBTs).

Yes, the IRS allows the estate of a deceased shareholder to be an S-Corporation shareholder. Note the language deceased shareholder. This indicates, correctly, that an estate can step in and become an S-Corp shareholder when a typical shareholder dies.

The main difference between an ESBT and a QSST is that an ESBT may have multiple income beneficiaries, and the trust does not have to distribute all income. Unlike with the QSST, the trustee, rather than the beneficiary, must make the election.