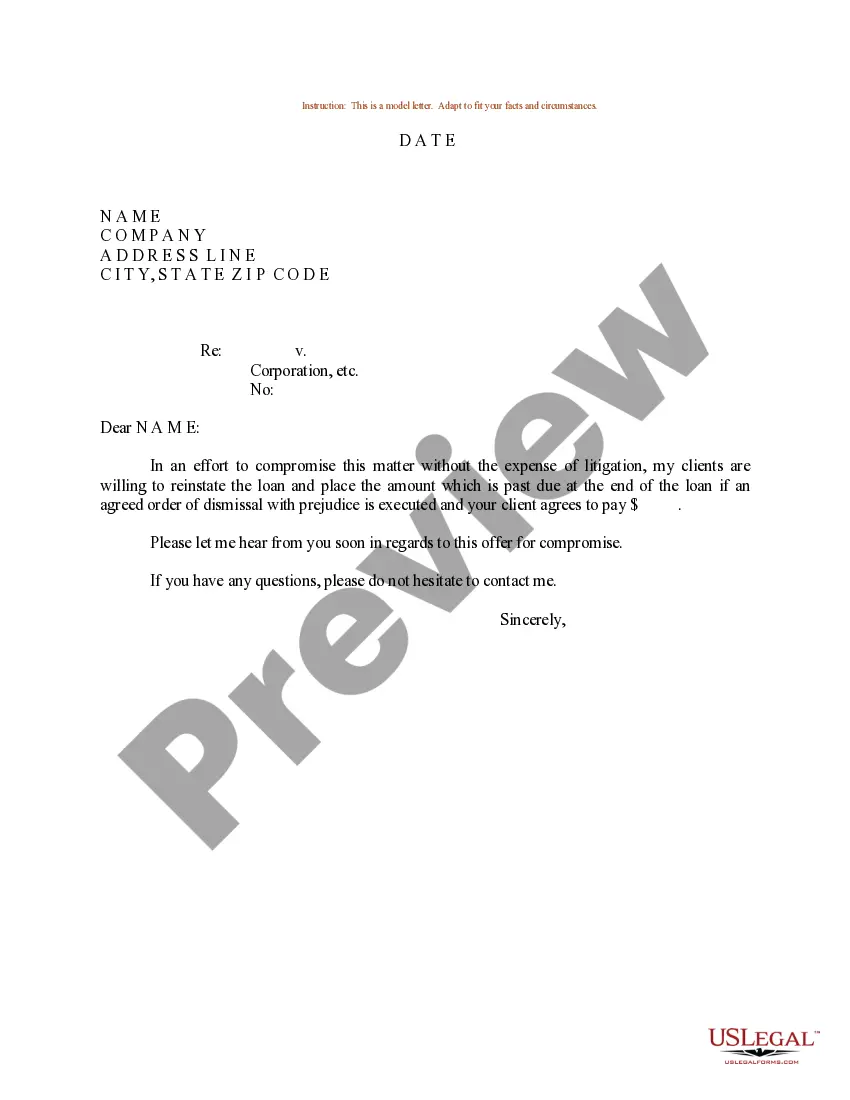

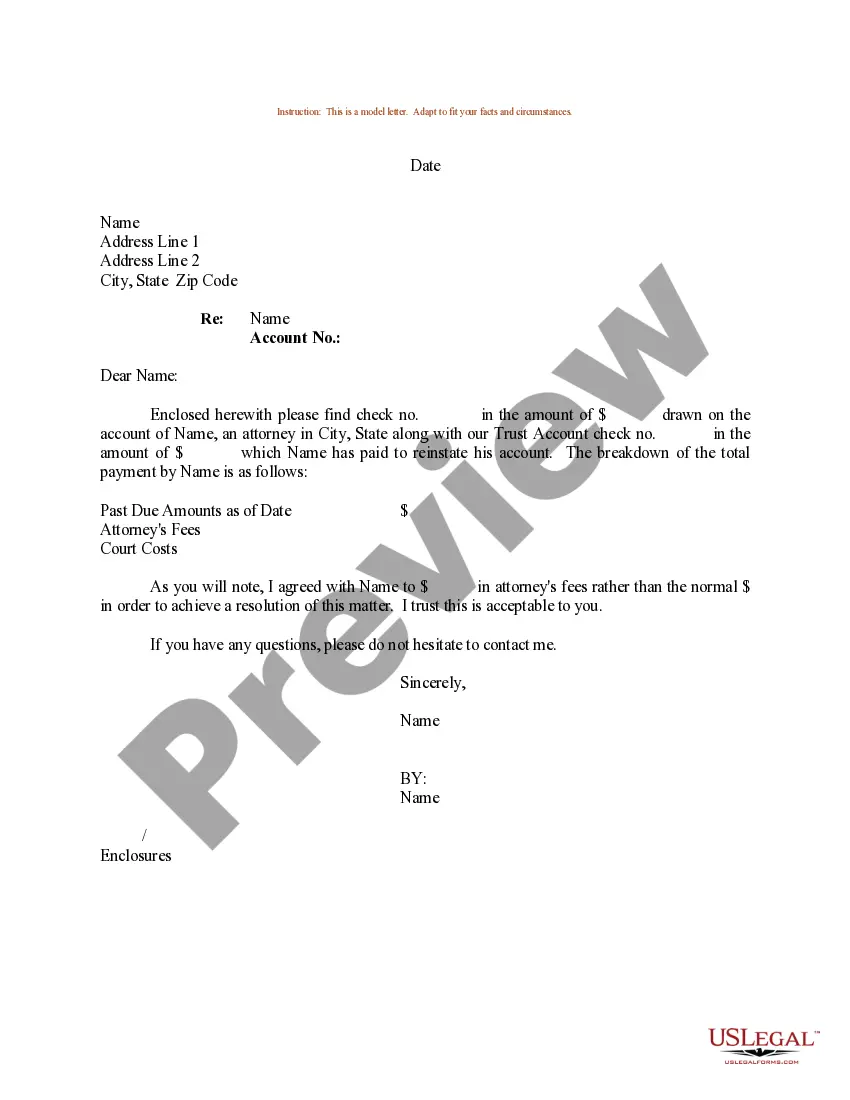

South Dakota Sample Letter for Insufficient Amount to Reinstate Loan

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Sample Letter For Insufficient Amount To Reinstate Loan?

Locating the appropriate official document template can be challenging. Naturally, there are numerous templates available online, but how will you procure the official form you need? Utilize the US Legal Forms website.

The platform offers thousands of templates, including the South Dakota Sample Letter for Insufficient Amount to Reinstate Loan, suitable for both business and personal purposes. All forms are reviewed by experts and meet federal and state requirements.

If you are already a member, Log In to your account and click the Obtain button to download the South Dakota Sample Letter for Insufficient Amount to Reinstate Loan. Use your account to browse the official forms you've purchased previously. Visit the My documents section of your account to retrieve another copy of the document you need.

Select the file format and download the official document template to your device. Fill out, modify, print, and sign the downloaded South Dakota Sample Letter for Insufficient Amount to Reinstate Loan. US Legal Forms is the largest repository of official forms where you can find various document templates. Use the service to obtain professionally crafted documents that adhere to state regulations.

- First, ensure you have selected the correct form for your region/state.

- You can review the form using the Preview button and check the form details to confirm it is the right one for you.

- If the form does not meet your requirements, utilize the Search field to find the correct form.

- Once you are certain that the form is suitable, click the Get now button to download the form.

- Choose the pricing plan you want and enter the required information.

- Create your account and complete the payment for your order using your PayPal account or credit card.

Form popularity

FAQ

In South Dakota, the statute of limitations varies depending on the type of claim. Generally, the time limit for most written contracts, including those related to loans, is six years. Familiarizing yourself with these time frames is crucial, especially if you are drafting documents like a South Dakota Sample Letter for Insufficient Amount to Reinstate Loan. Consulting with a legal expert can help clarify any concerns about your specific situation.

A powerful appeal letter is concise, clear, and compelling. Begin with a strong introduction that outlines your purpose, and follow it with detailed explanations that back your claims. Use the South Dakota Sample Letter for Insufficient Amount to Reinstate Loan as a guideline to format your letter effectively. Ensure you express your request respectfully and conclude with a call to action that encourages a positive response.

To write a denial appeal letter, start by addressing the letter to the appropriate party. Clearly state the reason for your appeal and reference the specific decision you seek to challenge. It’s helpful to include any evidence or documentation that supports your position. If you’re using a South Dakota Sample Letter for Insufficient Amount to Reinstate Loan, you can adapt it to ensure your appeal is formal and persuasive.

To substantiate your financial hardship, you typically need multiple documents, such as tax returns, recent paychecks, and bank account statements. Additionally, a statement outlining your expenses and obligations will provide a clearer picture of your situation. Using a South Dakota Sample Letter for Insufficient Amount to Reinstate Loan can help you compile and organize these documents in a cohesive manner for your lender.

A good hardship letter clearly lays out your circumstances in a straightforward way. It should include the reasons for your financial difficulties, specific details about your situation, and a request for assistance. You may find that a South Dakota Sample Letter for Insufficient Amount to Reinstate Loan serves as an excellent guideline to help you develop a well-structured and impactful letter.

A proof of hardship letter effectively communicates your inability to meet financial obligations. This letter should include a description of your financial situation, supporting documentation, and what options you are seeking. When creating this letter, a South Dakota Sample Letter for Insufficient Amount to Reinstate Loan can guide you in framing your request correctly and effectively.

A proof of financial hardship letter is a document you provide to a lender or creditor detailing your financial struggles. This letter should explain the specific factors contributing to your hardship, such as medical bills or loss of income. By using a South Dakota Sample Letter for Insufficient Amount to Reinstate Loan, you can craft a more compelling case that clearly states your circumstances and requests necessary support.

A financial hardship letter is a personal document written to a lender explaining your current financial situation. For instance, if you're unable to make loan payments due to unexpected job loss, you can use a South Dakota Sample Letter for Insufficient Amount to Reinstate Loan to outline your challenges. This letter should clearly communicate your difficulties, your attempts to resolve the issue, and your request for assistance.