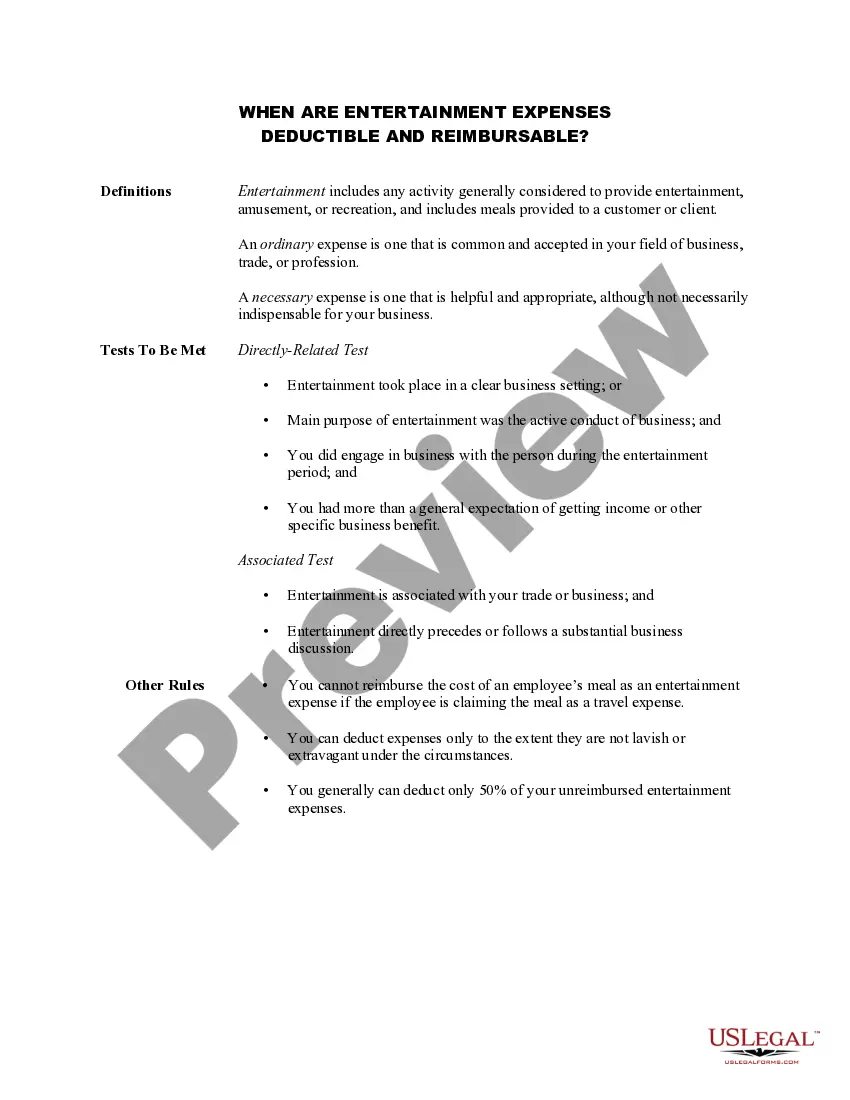

Title: South Dakota Information Sheet — When are Entertainment Expenses Deductible and Reimbursable Introduction: The South Dakota Information Sheet regarding the reducibility and reimbursement of entertainment expenses provides detailed guidelines for individuals and businesses on when they can claim these expenses as tax deductions or request reimbursement. This article aims to provide a comprehensive overview of these guidelines, explaining the different types of entertainment expenses that qualify, and the specific requirements for reducibility and reimbursement. Key Points: 1. Definition of Entertainment Expenses: — South Dakota defines entertainment expenses as costs incurred for activities focused on entertaining or providing amusement, relaxation, or diversion to a client, customer, or employee. 2. Business Entertainment Expenses: Reducibilityty: Business entertainment expenses may be tax-deductible if they are directly related to or associated with the active conduct of a trade or business. — Reimbursement: Employers can reimburse employees for business entertainment expenses incurred on behalf of the business. 3. Deductible Entertainment Expenses: — Meals and Entertainment: South Dakota allows taxpayers to deduct 50% of qualifying food and beverage expenses associated with business-related entertainment activities. — Ticket Costs: Expenses related to tickets for cultural, sporting, or other similar events directly related to the active conduct of a trade or business may be deductible. 4. Reimbursable Entertainment Expenses: — Employers may reimburse employees for qualifying entertainment expenses incurred on behalf of the business, subject to certain restrictions and documentation requirements. — Reimbursements must be supported by adequate substantiation, such as receipts, and must be ordinary and necessary business expenses within IRS guidelines. 5. Non-deductible Entertainment Expenses: — Entertainment activities considered lavish, extravagant, or primarily personal in nature are generally not deductible. — Expenses incurred on entertainment facilities used for personal purposes or offering recreational activities are non-deductible. Conclusion: The South Dakota Information Sheet on the reducibility and reimbursement of entertainment expenses helps individuals and businesses understand the rules surrounding these costs. By following the guidelines, taxpayers are able to determine which entertainment expenses are deductible and can be reimbursed. It is crucial to consult with tax professionals to ensure compliance with state and federal regulations when dealing with entertainment expenses.

South Dakota Information Sheet - When are Entertainment Expenses Deductible and Reimbursable

Description

How to fill out South Dakota Information Sheet - When Are Entertainment Expenses Deductible And Reimbursable?

If you need to comprehensive, download, or printing legitimate document web templates, use US Legal Forms, the most important variety of legitimate forms, which can be found on the Internet. Utilize the site`s easy and practical search to discover the papers you want. Numerous web templates for company and specific functions are sorted by classes and says, or keywords. Use US Legal Forms to discover the South Dakota Information Sheet - When are Entertainment Expenses Deductible and Reimbursable within a number of click throughs.

When you are previously a US Legal Forms consumer, log in in your profile and then click the Obtain switch to find the South Dakota Information Sheet - When are Entertainment Expenses Deductible and Reimbursable. You may also accessibility forms you formerly delivered electronically within the My Forms tab of your own profile.

If you work with US Legal Forms the very first time, follow the instructions beneath:

- Step 1. Be sure you have chosen the form to the correct town/country.

- Step 2. Use the Review choice to look through the form`s information. Don`t neglect to read the outline.

- Step 3. When you are unhappy with all the develop, take advantage of the Research discipline towards the top of the display screen to find other versions of your legitimate develop template.

- Step 4. Once you have discovered the form you want, go through the Get now switch. Choose the rates program you choose and add your credentials to register for the profile.

- Step 5. Method the transaction. You may use your bank card or PayPal profile to finish the transaction.

- Step 6. Choose the file format of your legitimate develop and download it on the system.

- Step 7. Comprehensive, change and printing or indication the South Dakota Information Sheet - When are Entertainment Expenses Deductible and Reimbursable.

Each and every legitimate document template you acquire is the one you have forever. You may have acces to every develop you delivered electronically inside your acccount. Go through the My Forms segment and pick a develop to printing or download once more.

Contend and download, and printing the South Dakota Information Sheet - When are Entertainment Expenses Deductible and Reimbursable with US Legal Forms. There are many professional and status-specific forms you may use to your company or specific demands.