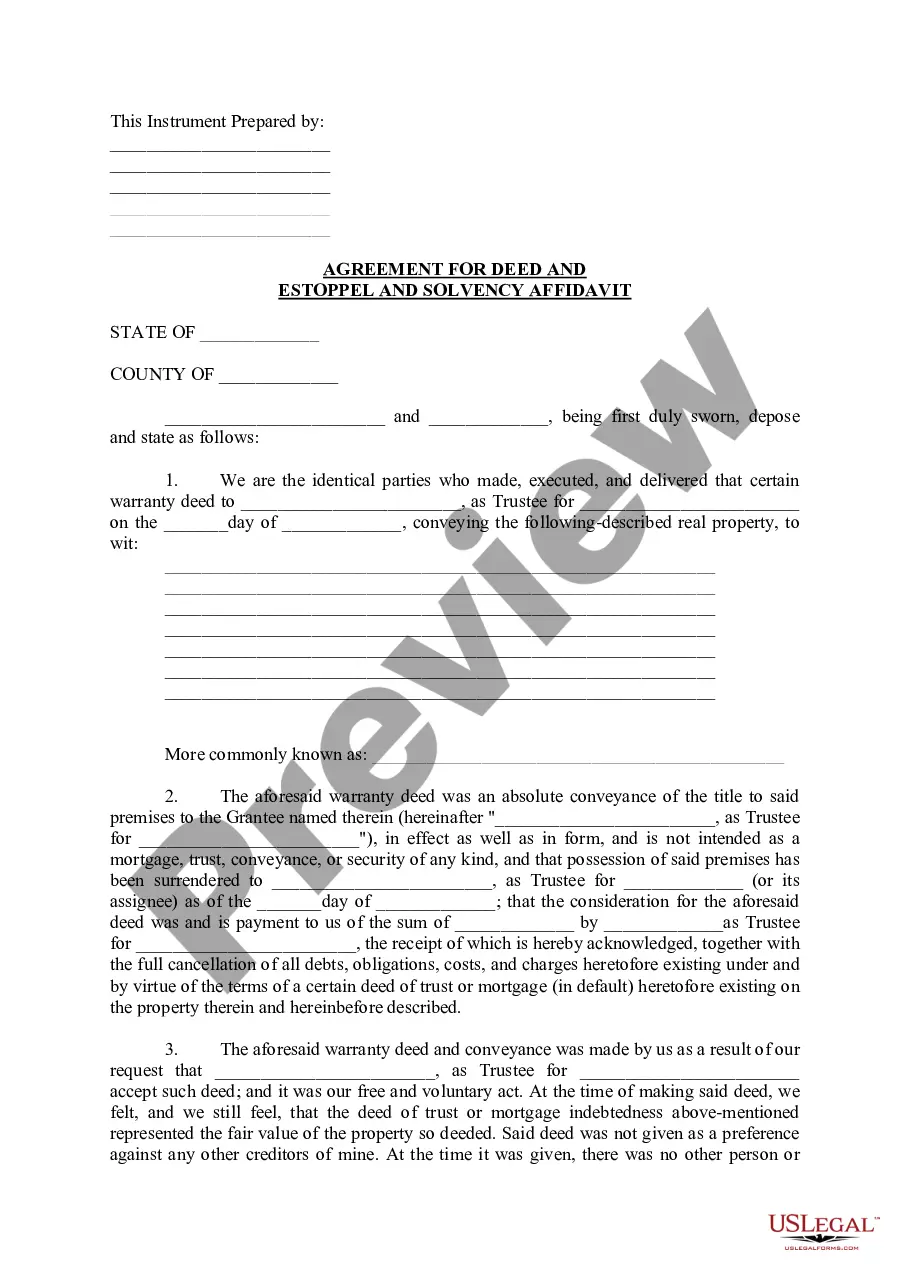

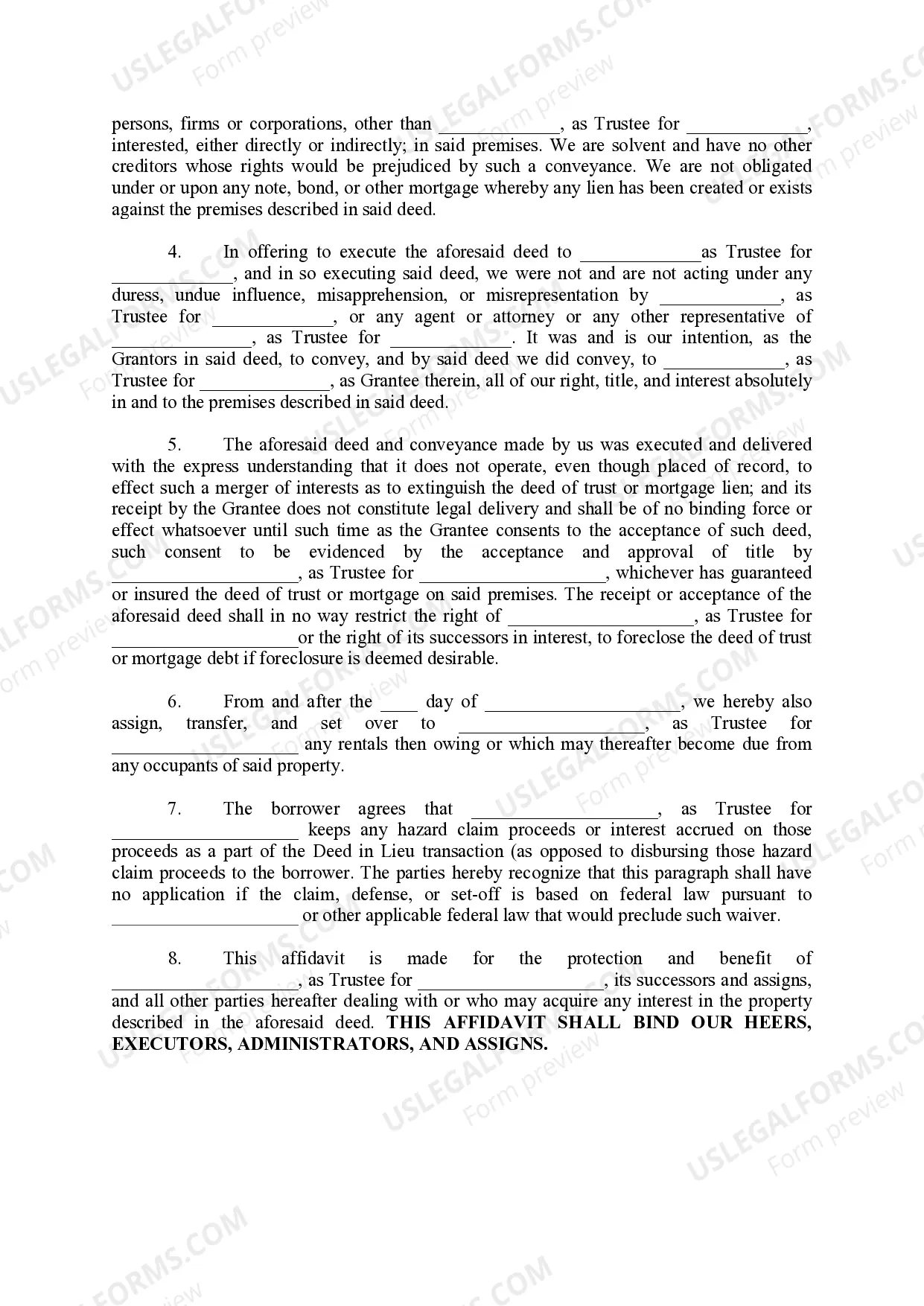

Estoppel Affidavit of Mortgagor sets out the status of the mortgage or deed of trust. The Affidavit is made for the protection benefit of all parties dealing with or who may acquire any interest in the property described in the deed.

mortgage or deed of trust. The Affidavit is made for the protection and benefit of all parties dealing with or who may acquire any

interest in the property described in the aforesaid deed

Tennessee Agreement for Deed and Estoppel and Solvency Affidavit

Instant download

Description

Free preview Solvency Affidavit

How to fill out Tennessee Agreement For Deed And Estoppel And Solvency Affidavit?

Access to quality Tennessee Agreement for Deed and Estoppel and Solvency Affidavit templates online with US Legal Forms. Avoid days of lost time seeking the internet and dropped money on forms that aren’t up-to-date. US Legal Forms provides you with a solution to exactly that. Find over 85,000 state-specific authorized and tax samples you can save and fill out in clicks within the Forms library.

To find the example, log in to your account and click Download. The document will be stored in two places: on the device and in the My Forms folder.

For individuals who don’t have a subscription yet, check out our how-guide listed below to make getting started simpler:

- See if the Tennessee Agreement for Deed and Estoppel and Solvency Affidavit you’re looking at is suitable for your state.

- View the sample making use of the Preview option and read its description.

- Check out the subscription page by clicking Buy Now.

- Choose the subscription plan to go on to sign up.

- Pay out by card or PayPal to finish making an account.

- Choose a preferred format to save the file (.pdf or .docx).

You can now open the Tennessee Agreement for Deed and Estoppel and Solvency Affidavit example and fill it out online or print it out and do it by hand. Consider sending the file to your legal counsel to be certain things are completed appropriately. If you make a error, print and fill sample again (once you’ve created an account all documents you download is reusable). Make your US Legal Forms account now and get access to much more forms.

Form popularity

FAQ

If your lender agrees to a short sale or to accept a deed in lieu of foreclosure, you might owe federal income tax on any forgiven deficiency. The IRS learns of the deficiency when the lender sends it a Form 1099-C, which reports the forgiven debt as income to you.

A deed in lieu is different from a foreclosure. A deed in lieu means you and your lender reach a mutual understanding that you cannot make your loan payments. The lender agrees to avoid putting you into foreclosure when you hand the property over amicably.

A deed in lieu of foreclosure is different from a short sale because it transfers the property to the lender instead of selling it to a new buyer.Similar to a short sale, a deed in lieu of foreclosure likely will not damage your credit as severely as a foreclosure or a bankruptcy.

A short sale in real estate is when a financially distressed homeowner sells their property for less than the amount due on the mortgage. The buyer of the property is a third party (not the bank), and all proceeds from the sale go to the lender.

Final Thoughts On Deed In Lieu Of Foreclosure When you take a deed in lieu agreement, you transfer your home's deed to your lender voluntarily. In exchange, the lender agrees to forgive the amount left on your loan. A deed in lieu agreement won't stay on your credit report if a foreclosure will.

An estoppel affidavit is a legal document that prohibits the parties from taking any action that's contrary to an agreement previously made.The affidavit usually states that the parties entered into the agreement willingly and cites the fair market value of the property at the time the deal is made.

Disadvantages of a Deed in Lieu of Foreclosure. Perhaps the biggest disadvantage of a deed in lieu is that the Lender takes subject to all other encumbrances and interests in the Property. Therefore if there is a second mortgage, for example, a deed in lieu would likely not be a viable strategy.

Short sales and foreclosures can get homeowners out of paying for their mortgages. Short sales are voluntary and require approval from the lender. Foreclosures are involuntary, where the lender takes legal action to take control of and sell the property.