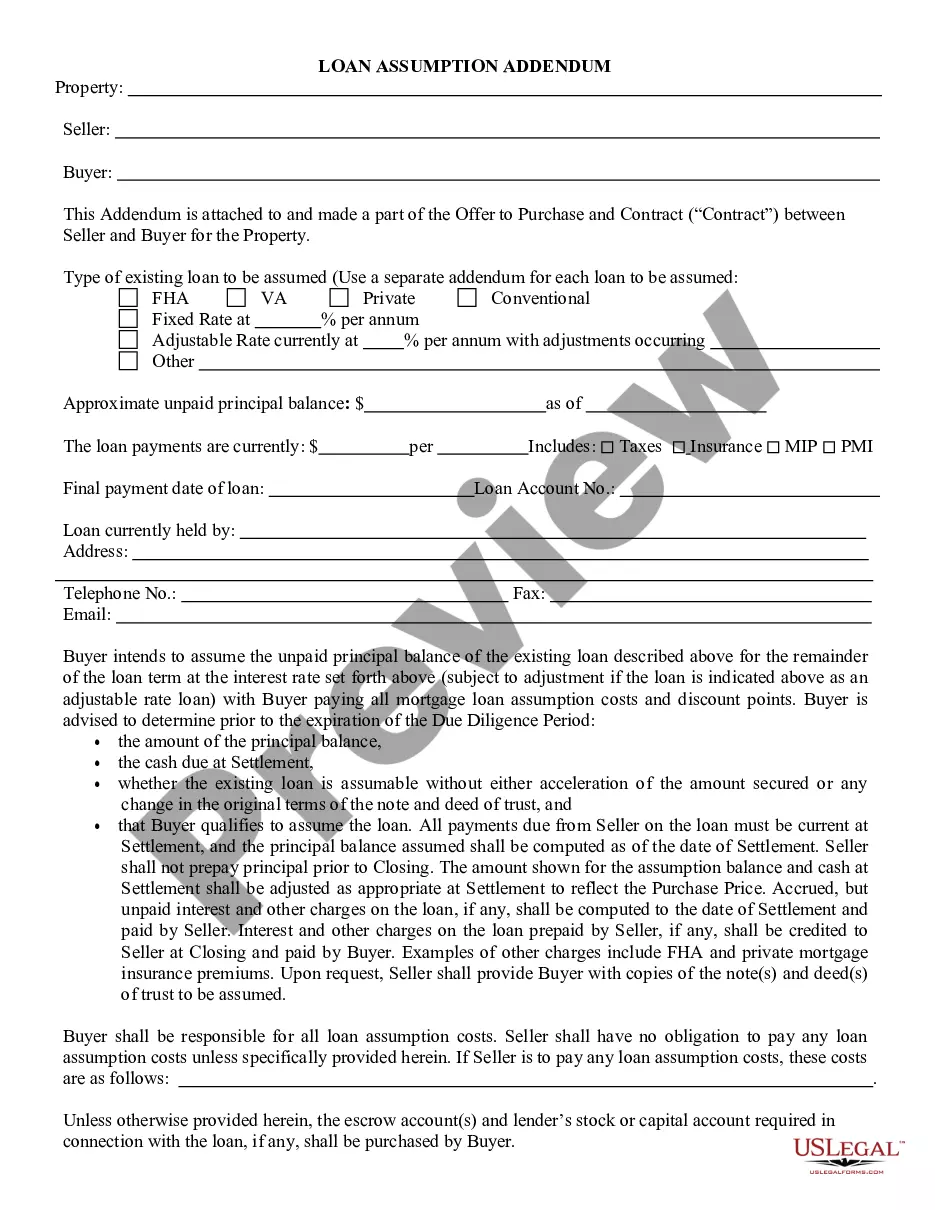

This form is an Assumption Agreement. The grantor desires to convey certain property to the grantee and the grantee agrees to assume the lien and the loan. The agreement must also be signed in the presence of a notary public.

Tennessee Loan Assumption Agreement

Category:

State:

Multi-State

Control #:

US-00561

Format:

Word;

Rich Text

Instant download

Description

Free preview

How to fill out Loan Assumption Agreement?

US Legal Forms - one of the largest collections of legal documents in the United States - provides a vast selection of legal form templates that you can download or create.

By using the website, you can access thousands of forms for business and personal purposes, organized by categories, states, or keywords. You can obtain the latest versions of forms such as the Tennessee Loan Assumption Agreement in just a few minutes.

If you have a subscription, Log In and download the Tennessee Loan Assumption Agreement from the US Legal Forms library. The Download button will be available on each form you view. You can access all previously downloaded forms in the My documents section of your account.

Process the payment. Use a credit card or PayPal account to complete the transaction. Choose the format and download the form to your device. Make edits. Fill out, modify, print, and sign the downloaded Tennessee Loan Assumption Agreement.

Each form you add to your account has no expiration date and is yours forever. Therefore, if you wish to download or print another copy, simply go to the My documents section and click on the form you need. Access the Tennessee Loan Assumption Agreement with US Legal Forms, the most extensive library of legal document templates. Utilize thousands of professional and state-specific templates that meet your business or personal needs and requirements.

- If you are using US Legal Forms for the first time, here are simple steps to help you get started.

- Ensure you have selected the correct form for your location/area.

- Click the Preview button to review the form's content.

- Check the form description to confirm that you have chosen the right form.

- If the form does not meet your needs, use the Search field at the top of the screen to find one that does.

- If you are satisfied with the form, confirm your choice by clicking the Download now button.

- Then, select the pricing plan you want and provide your information to register for an account.

Form popularity

FAQ

A loan assumption agreement is an agreement between a lender, original borrower, and a new borrower, where the new borrower agrees to assume responsibility for the debt owed by original borrower. These agreements are commonly seen in mortgages and real estate.

"Assume" means the buyer takes on liability, and the seller is no longer primarily liable. "Subject to" means the seller is not released from responsibility. The word "assumption" is used when a buyer assumes personal liability for an existing debt.

A Loan Assumption occurs when a purchaser of a property assumes the existing mortgage loan debt of the original customer (who is now ?selling? the home and loan debt to the new buyer). Loan assumptions must be approved by the lender.

Lenders must typically approve an assumable mortgage. If done without approval, sellers run the risk of having to pay the full remaining balance upfront. Sellers also risk buyers missing payments, which can negatively impact their credit score.

An assumption clause is a provision in a mortgage contract that allows the seller of a home to pass responsibility for the existing mortgage to the buyer of the property. In other words, the new homeowner assumes the existing mortgage and?along with it?ownership of the property that secures the loan.

Assumption of Obligations. New Borrower covenants, promises, and agrees that New Borrower, jointly and severally if more than one, will unconditionally assume and be bound by all terms, provisions, and covenants of the Assumed Loan Documents as if New Borrower had been the original maker of the Assumed Loan Documents.