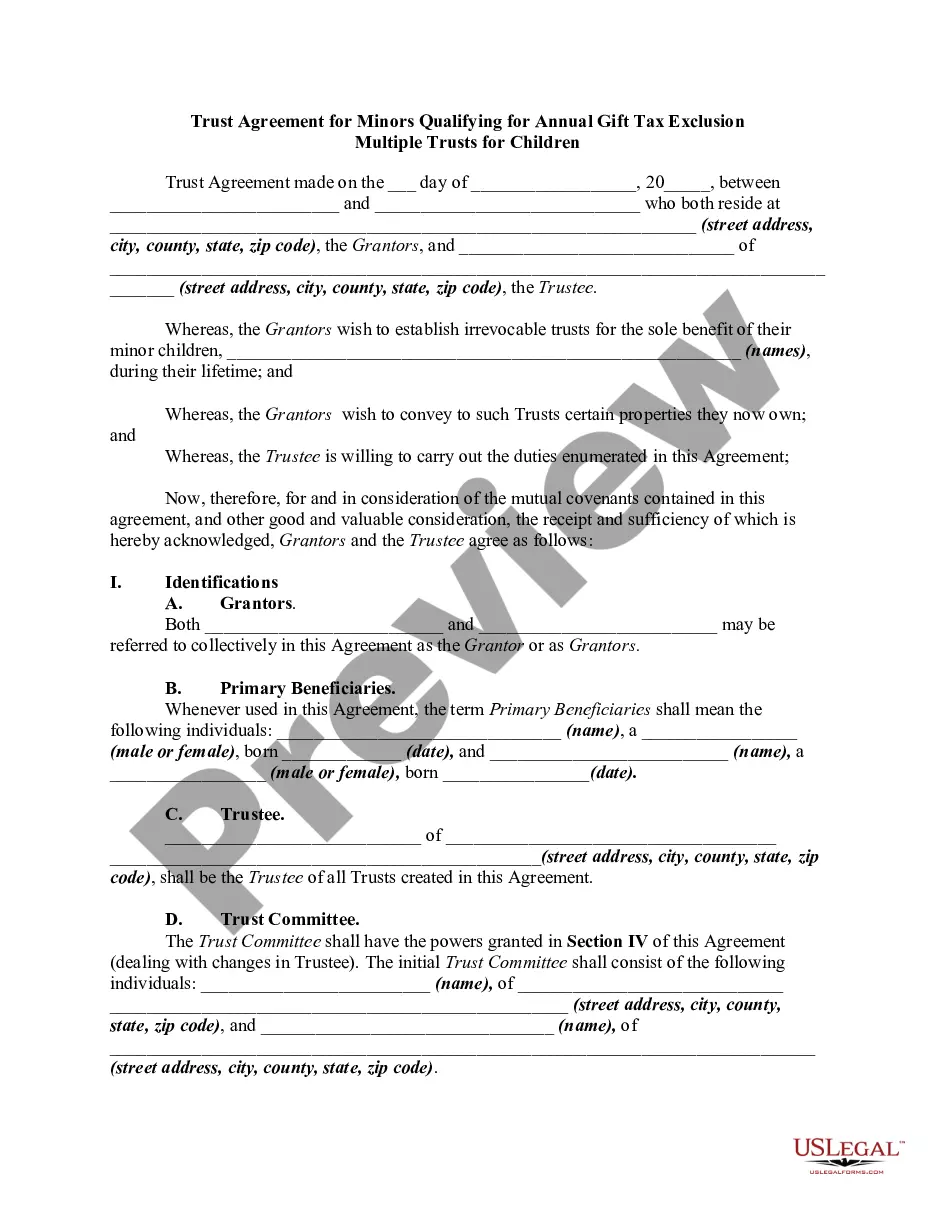

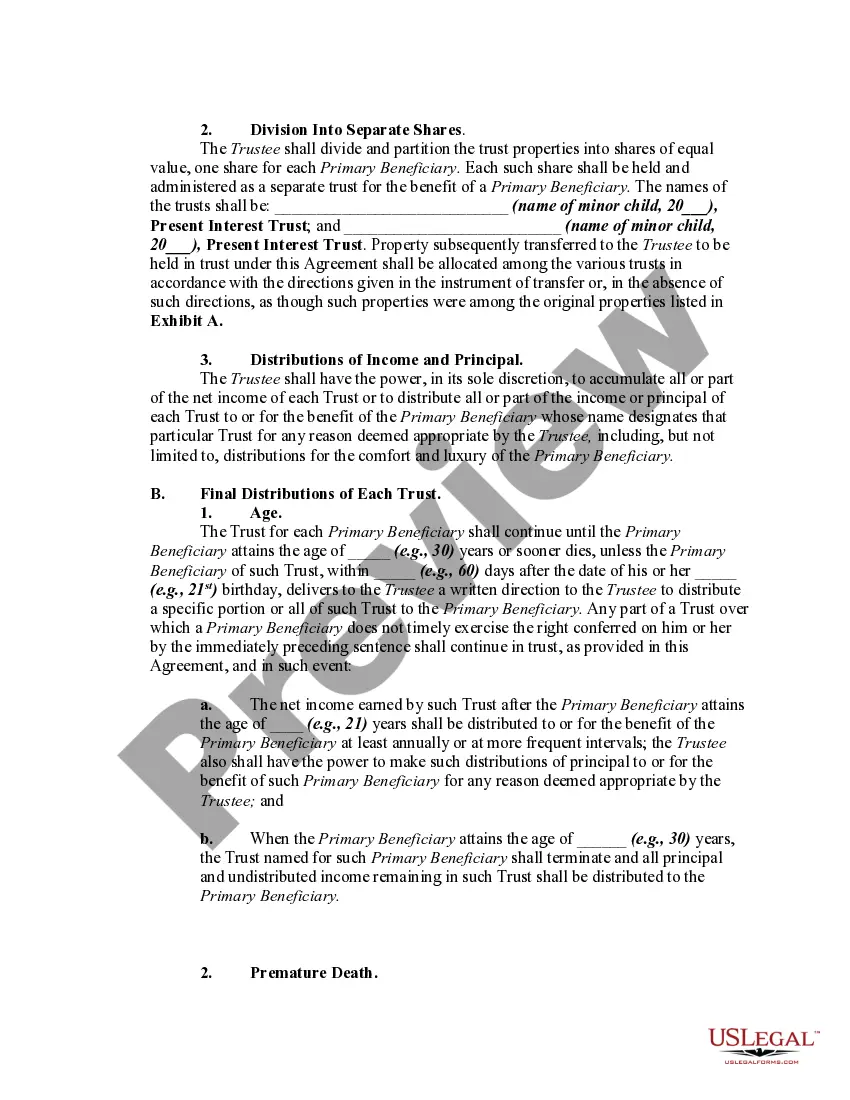

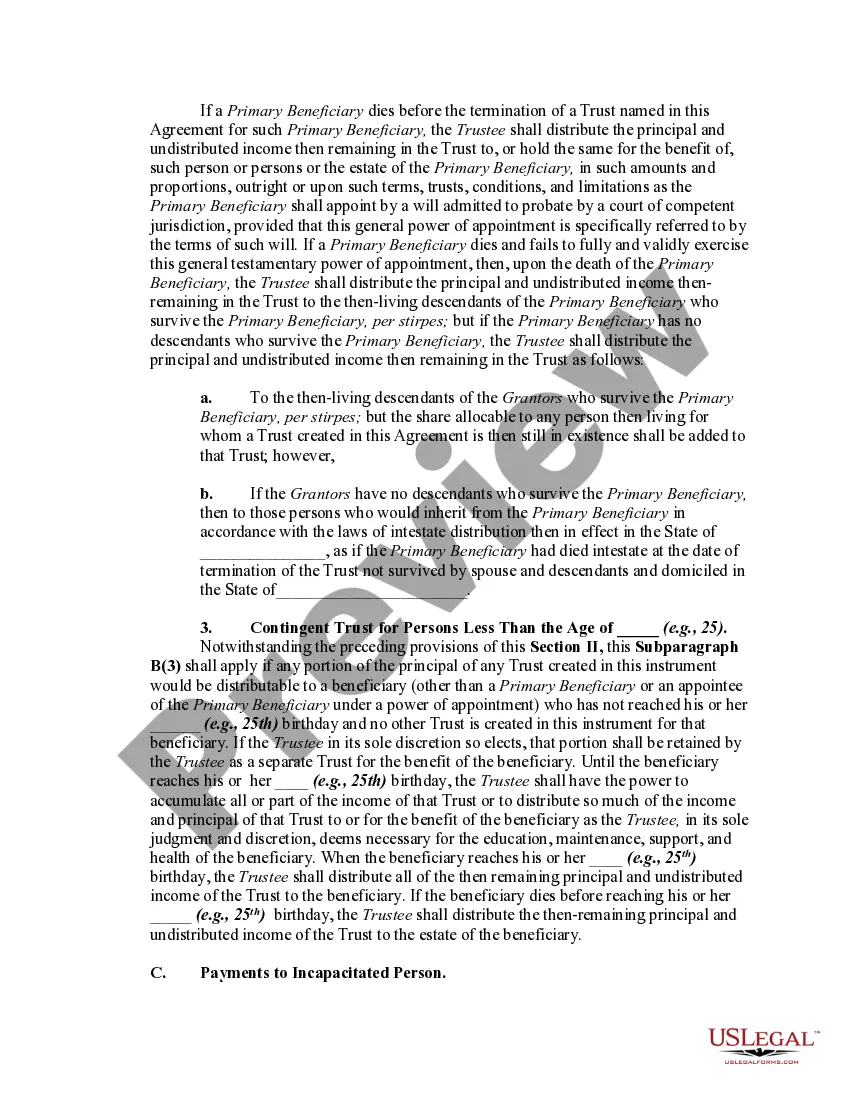

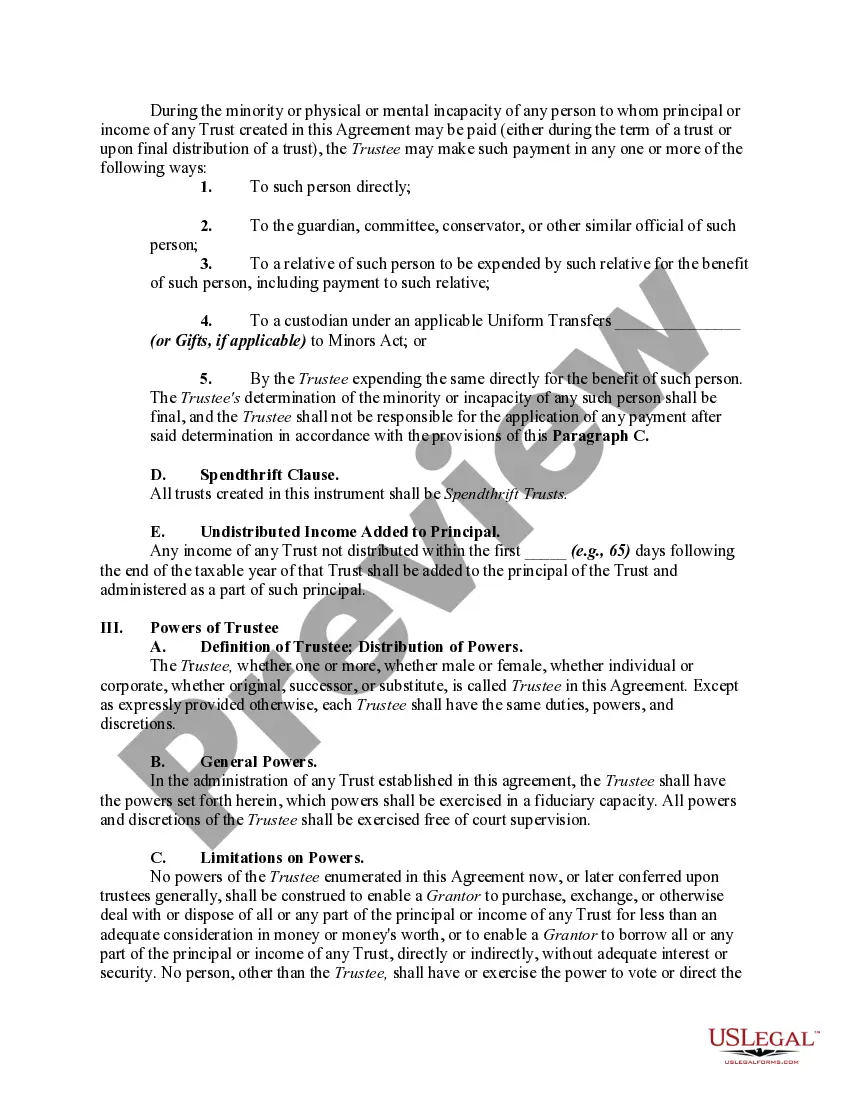

This form set up what is known as present interest trusts, with the intention of meeting the requirements of Section 2503(c) of the Internal Revenue Code.

A Tennessee Trust Agreement for Minors Qualifying for Annual Gift Tax Exclusion — Multiple Trusts for Children is a legal document that allows individuals to create multiple trusts for their minor children in order to take advantage of the annual gift tax exclusion. This arrangement helps ensure that assets gifted to minors are properly managed and protected until they reach adulthood. One type of Tennessee Trust Agreement for Minors Qualifying for Annual Gift Tax Exclusion is the Crummy Trust. It is named after the Crummy v. Commissioner case, which established the concept of making gifts to minors through irrevocable trusts. Crummy trusts allow individuals to take advantage of the annual gift tax exclusion by giving beneficiaries the right to withdraw funds from the trust within a specified time frame, typically 30 days. By providing this withdrawal right, gifts made to the trust are considered present interests, qualifying for the annual gift tax exclusion. Another type of Tennessee Trust Agreement for Minors Qualifying for Annual Gift Tax Exclusion is the Section 2503(c) trust, commonly known as a Section 2503© Minor's Trust. This trust allows individuals to make tax-free gifts to minors by creating a trust that meets the requirements outlined in Section 2503(c) of the Internal Revenue Code. The trust must distribute all income to the child at least annually until they reach a certain age, typically 21, and can then either terminate or continue as a discretionary trust. Creating multiple trusts for children under the Tennessee Trust Agreement for Minors Qualifying for Annual Gift Tax Exclusion provides flexibility in managing gifts and tailoring the terms of each trust to the specific needs of each child. It allows individuals to provide for their children's financial well-being, education, or other specific purposes without being subject to the annual gift tax limitation. By establishing these trusts, parents or guardians can effectively manage and control the assets gifted to minors, ensuring that the funds are used for their intended purposes and are not subject to unnecessary taxation. Additionally, by using the annual gift tax exclusion, individuals can reduce their overall estate tax liability and maximize the value of their estate for future generations. In conclusion, a Tennessee Trust Agreement for Minors Qualifying for Annual Gift Tax Exclusion — Multiple Trusts for Children enables individuals to create various types of trust arrangements, such as Crummy trusts and Section 2503© Minor's Trusts, to take advantage of the gift tax exclusion. This legal tool allows for the long-term care and financial security of minors while minimizing tax implications and maximizing the value of the estate.A Tennessee Trust Agreement for Minors Qualifying for Annual Gift Tax Exclusion — Multiple Trusts for Children is a legal document that allows individuals to create multiple trusts for their minor children in order to take advantage of the annual gift tax exclusion. This arrangement helps ensure that assets gifted to minors are properly managed and protected until they reach adulthood. One type of Tennessee Trust Agreement for Minors Qualifying for Annual Gift Tax Exclusion is the Crummy Trust. It is named after the Crummy v. Commissioner case, which established the concept of making gifts to minors through irrevocable trusts. Crummy trusts allow individuals to take advantage of the annual gift tax exclusion by giving beneficiaries the right to withdraw funds from the trust within a specified time frame, typically 30 days. By providing this withdrawal right, gifts made to the trust are considered present interests, qualifying for the annual gift tax exclusion. Another type of Tennessee Trust Agreement for Minors Qualifying for Annual Gift Tax Exclusion is the Section 2503(c) trust, commonly known as a Section 2503© Minor's Trust. This trust allows individuals to make tax-free gifts to minors by creating a trust that meets the requirements outlined in Section 2503(c) of the Internal Revenue Code. The trust must distribute all income to the child at least annually until they reach a certain age, typically 21, and can then either terminate or continue as a discretionary trust. Creating multiple trusts for children under the Tennessee Trust Agreement for Minors Qualifying for Annual Gift Tax Exclusion provides flexibility in managing gifts and tailoring the terms of each trust to the specific needs of each child. It allows individuals to provide for their children's financial well-being, education, or other specific purposes without being subject to the annual gift tax limitation. By establishing these trusts, parents or guardians can effectively manage and control the assets gifted to minors, ensuring that the funds are used for their intended purposes and are not subject to unnecessary taxation. Additionally, by using the annual gift tax exclusion, individuals can reduce their overall estate tax liability and maximize the value of their estate for future generations. In conclusion, a Tennessee Trust Agreement for Minors Qualifying for Annual Gift Tax Exclusion — Multiple Trusts for Children enables individuals to create various types of trust arrangements, such as Crummy trusts and Section 2503© Minor's Trusts, to take advantage of the gift tax exclusion. This legal tool allows for the long-term care and financial security of minors while minimizing tax implications and maximizing the value of the estate.