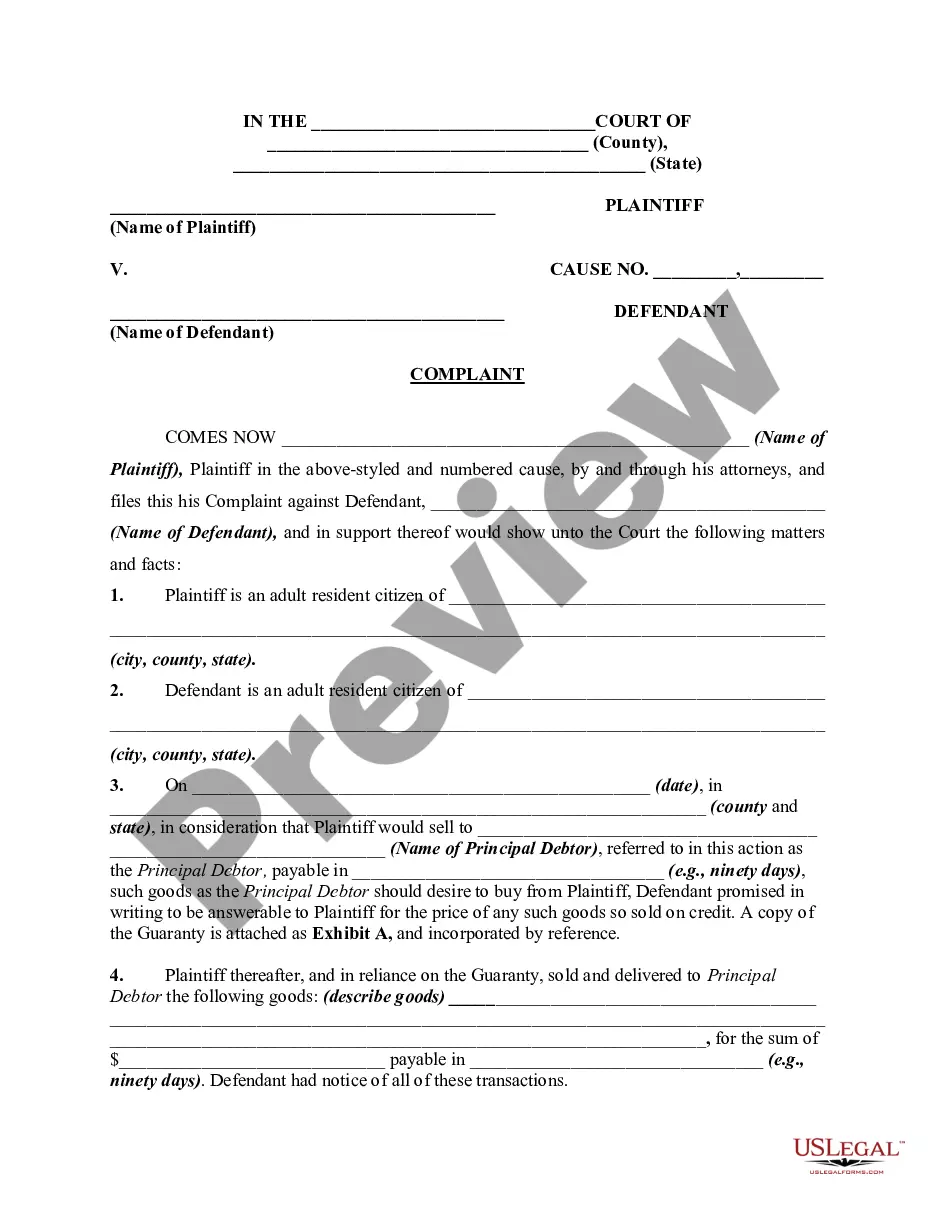

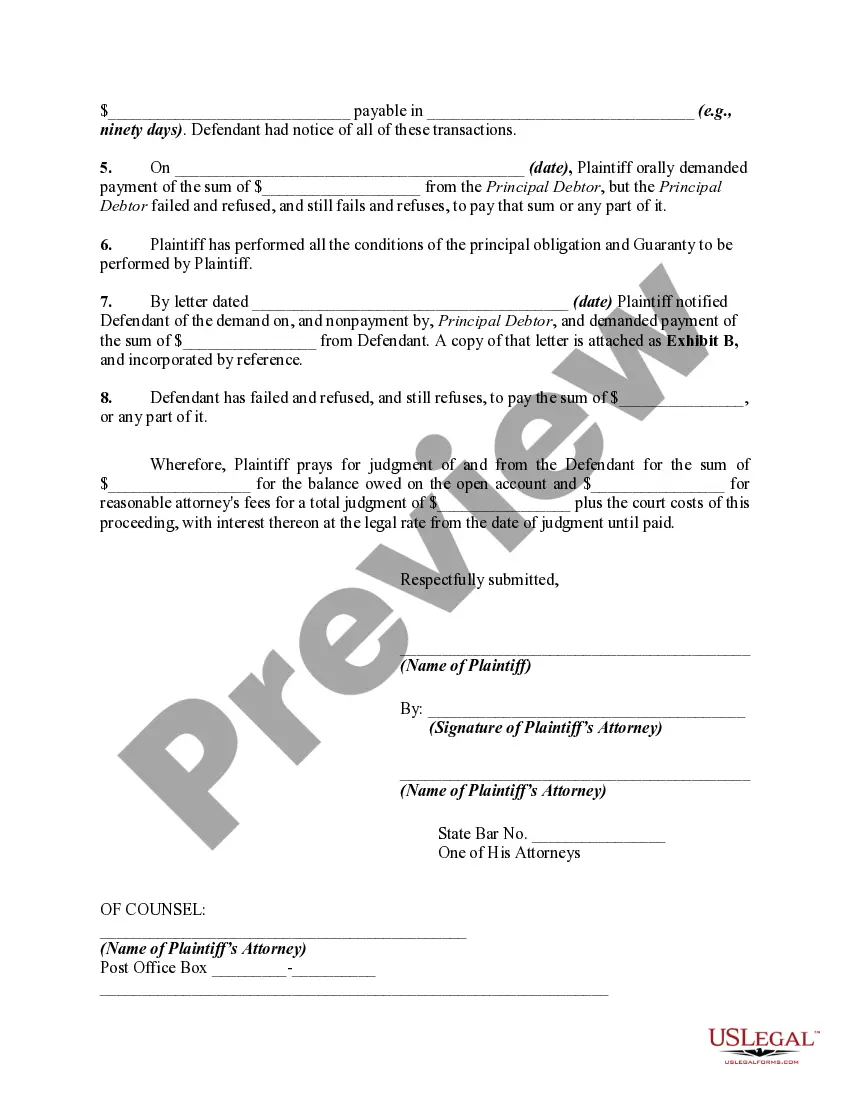

An open account is an account based on continuous dealing between the parties, which has not been closed, settled or stated, and which is kept open with the expectation of further transactions. An open account is created when the parties intend that the individual items of the account will not be considered independently, but as a connected series of transactions. In addition, the parties must intend that the account will be kept open and subject to a shifting balance as additional related entries of debits and credits are made, until either party decides to settle and close the account. This form is a complaint against a guarantor of such an account.

This form is a generic example that may be referred to when preparing such a form for your particular state. It is for illustrative purposes only. Local laws should be consulted to determine any specific requirements for such a form in a particular jurisdiction.

Title: Tennessee Complaint Against Guarantor of Open Account Credit Transactions — Breach of Oral or Implied Contracts Keywords: Tennessee complaint, guarantor, open account credit transactions, breach, oral contracts, implied contracts Introduction: In the state of Tennessee, individuals can file a complaint against a guarantor when there has been a breach of oral or implied contracts in open account credit transactions. Open account credit transactions refer to an agreement where a creditor allows a debtor to make purchases on a credit basis, often without fixed terms or a definite repayment schedule. This detailed description will explore the various types of Tennessee complaints against guarantors regarding the breach of such contracts. 1. Complaint for Breach of Oral Contract: When an open account credit transaction is based on an oral agreement between the creditor and debtor, a complaint can be filed against the guarantor if they fail to fulfill their obligations or violate the terms outlined in the oral contract. This type of complaint requires proper documentation and evidence to support the existence of an oral agreement. 2. Complaint for Breach of Implied Contract: In some cases, open account credit transactions may not involve explicit oral or written agreements but can still give rise to an implicit or implied contract. A complaint can be filed against the guarantor when they fail to meet the implied terms or obligations associated with the open account credit transaction. To support this claim, evidence that demonstrates a consistent pattern of conduct between the parties is essential. 3. Complaint for Breach of Contract Terms: Apart from oral and implied contracts, a complaint can be filed against a guarantor if they fail to comply with the terms explicitly stated in a written agreement related to an open account credit transaction. By demonstrating the violation of specific contractual provisions, such as repayment deadlines or interest rates, the plaintiff can seek remedies for the breach. 4. Complaint for Fraudulent Inducement: Fraudulent inducement occurs when a guarantor induces the creditor or debtor to enter into an open account credit transaction through false representations or misleading information. In such cases, a complaint can be filed against the guarantor for breach of contract and fraudulent conduct. Conclusion: Tennessee provides individuals the opportunity to file complaints against guarantors of open account credit transactions in cases of breach of oral or implied contracts. Whether there is an oral agreement, implied obligations, explicit written terms, or fraudulent inducement, individuals can pursue legal remedies to seek compensation or enforce compliance. It is important for the complainant to gather relevant evidence and consult with legal professionals when pursuing such complaints for a successful outcome.