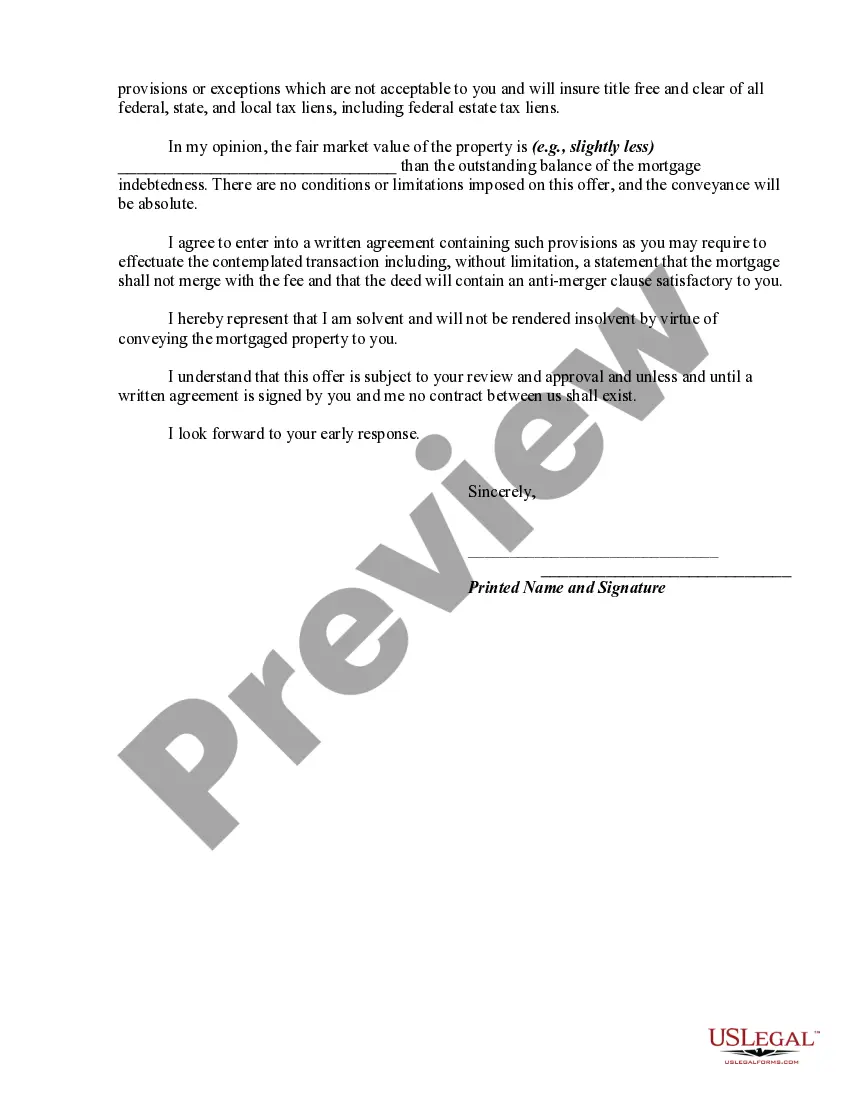

A deed in lieu of foreclosure is a method sometimes used by a lienholder on property to avoid a lengthy and expensive foreclosure process, with a deed in lieu of foreclosure a foreclosing lienholder agrees to have the ownership interest transferred to the bank/lienholder as payment in full. The debtor basically deeds the property to the bank instead of them paying for foreclosure proceedings. Therefore, if a debtor fails to make mortgage payments and the bank is about to foreclose on the property, the deed in lieu of foreclosure is an option that chooses to give the bank ownership of the property rather than having the bank use the legal process of foreclosure.

Tennessee Offer by Borrower of Deed in Lieu of Foreclosure is a legal option available to homeowners facing financial difficulties and potential foreclosure proceedings. This alternative allows borrowers to voluntarily transfer the title of their property to the lender, effectively satisfying the debt in exchange for avoiding the foreclosure process. By providing a deed in lieu of foreclosure, borrowers relinquish their ownership rights, enabling the lender to assume control of the property. This arrangement can be beneficial for both parties involved, as it allows the borrower to avoid the negative consequences of foreclosure while providing the lender with a quicker resolution to the unpaid debt. There are several types of Tennessee Offer by Borrower of Deed in Lieu of Foreclosure agreements available, depending on the specific circumstances and negotiations between the borrower and lender. Some common variations include: 1. Traditional Deed in Lieu: This is the standard option where the borrower voluntarily transfers the deed to the lender. The lender then releases the borrower from any further obligations associated with the mortgage. 2. Conditional Deed in Lieu: In some cases, the lender may require certain conditions to be met before accepting the deed in lieu. This could include property repairs, payment of outstanding liens, or other agreed-upon conditions. 3. Deed in Lieu with Cash for Keys: To incentivize borrowers to cooperate, lenders may offer cash incentives or relocation assistance in exchange for the property's deed. This arrangement helps borrowers with relocation costs and eases the transition. 4. Junior Lien holders' Subordination: If there are multiple liens on the property, especially if the first mortgage is in default, negotiation with junior lien holders becomes essential. In such cases, a deed in lieu agreement may involve subordinating the junior liens in order to proceed with the transfer of the property. It is crucial for borrowers to consult with legal professionals and/or financial advisors before pursuing a Tennessee Offer by Borrower of Deed in Lieu of Foreclosure. They can outline the potential benefits, implications, and any tax consequences associated with such arrangements. Additionally, lenders may have specific requirements and guidelines for accepting a deed in lieu, so borrowers should ensure they meet all necessary criteria to increase the likelihood of a successful resolution to their financial hardship.Tennessee Offer by Borrower of Deed in Lieu of Foreclosure is a legal option available to homeowners facing financial difficulties and potential foreclosure proceedings. This alternative allows borrowers to voluntarily transfer the title of their property to the lender, effectively satisfying the debt in exchange for avoiding the foreclosure process. By providing a deed in lieu of foreclosure, borrowers relinquish their ownership rights, enabling the lender to assume control of the property. This arrangement can be beneficial for both parties involved, as it allows the borrower to avoid the negative consequences of foreclosure while providing the lender with a quicker resolution to the unpaid debt. There are several types of Tennessee Offer by Borrower of Deed in Lieu of Foreclosure agreements available, depending on the specific circumstances and negotiations between the borrower and lender. Some common variations include: 1. Traditional Deed in Lieu: This is the standard option where the borrower voluntarily transfers the deed to the lender. The lender then releases the borrower from any further obligations associated with the mortgage. 2. Conditional Deed in Lieu: In some cases, the lender may require certain conditions to be met before accepting the deed in lieu. This could include property repairs, payment of outstanding liens, or other agreed-upon conditions. 3. Deed in Lieu with Cash for Keys: To incentivize borrowers to cooperate, lenders may offer cash incentives or relocation assistance in exchange for the property's deed. This arrangement helps borrowers with relocation costs and eases the transition. 4. Junior Lien holders' Subordination: If there are multiple liens on the property, especially if the first mortgage is in default, negotiation with junior lien holders becomes essential. In such cases, a deed in lieu agreement may involve subordinating the junior liens in order to proceed with the transfer of the property. It is crucial for borrowers to consult with legal professionals and/or financial advisors before pursuing a Tennessee Offer by Borrower of Deed in Lieu of Foreclosure. They can outline the potential benefits, implications, and any tax consequences associated with such arrangements. Additionally, lenders may have specific requirements and guidelines for accepting a deed in lieu, so borrowers should ensure they meet all necessary criteria to increase the likelihood of a successful resolution to their financial hardship.