A secured transaction is created when a buyer or borrower (debtor) grants a seller or lender (creditor or secured party) a security interest in personal property (collateral). A security interest allows a creditor to repossess and sell the collateral if a debtor fails to pay a secured debt.

The Truth-in-Lending Act (TILA) is part of the Federal Consumer Credit Protection Act. The purpose of the TILA is to make full disclosure to debtors of what they are being charged for the credit they are receiving. The Act merely asks lenders to be honest to the debtors and not cover up what they are paying for the credit. Regulation Z is a federal regulation prepared by the Federal Reserve Board to carry out the details of the Act. TILA applies to consumer credit transactions. Consumer credit is credit for personal or household use and not commercial use or business purposes.

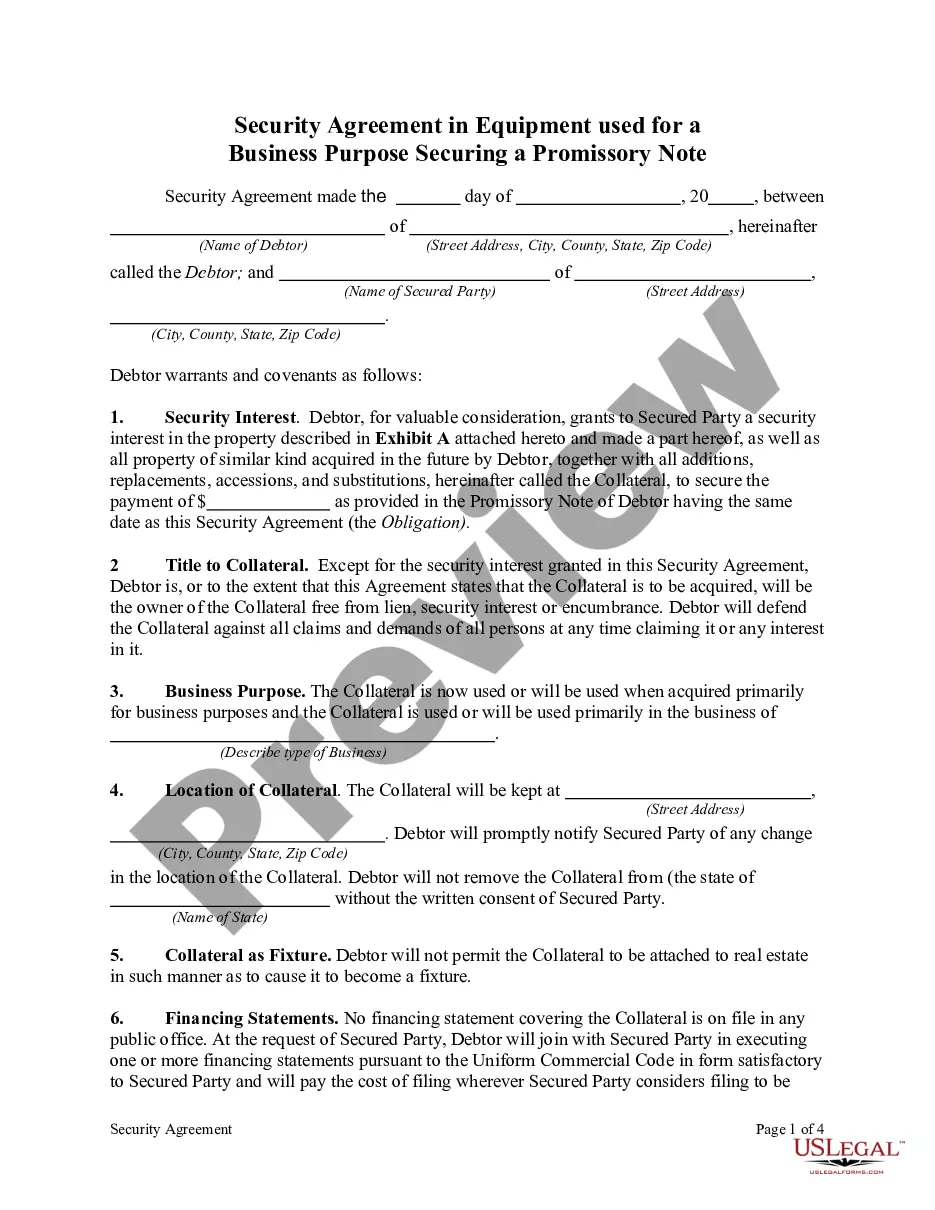

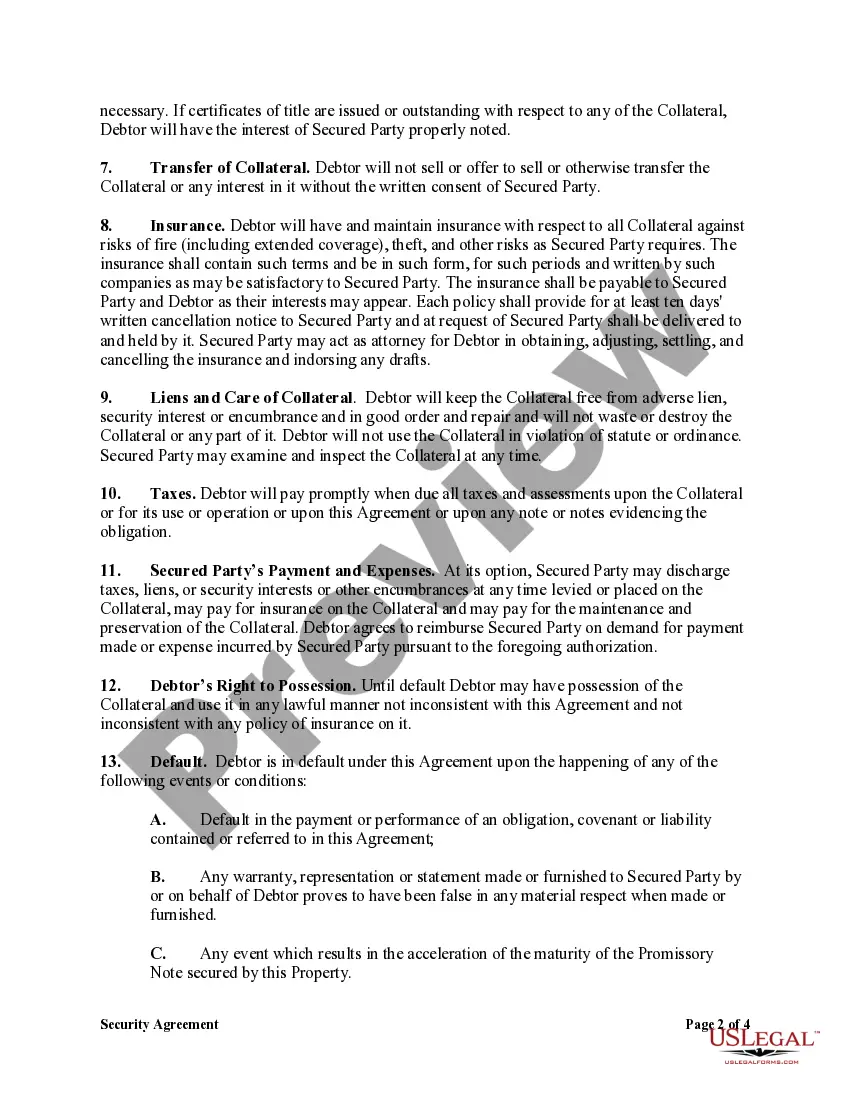

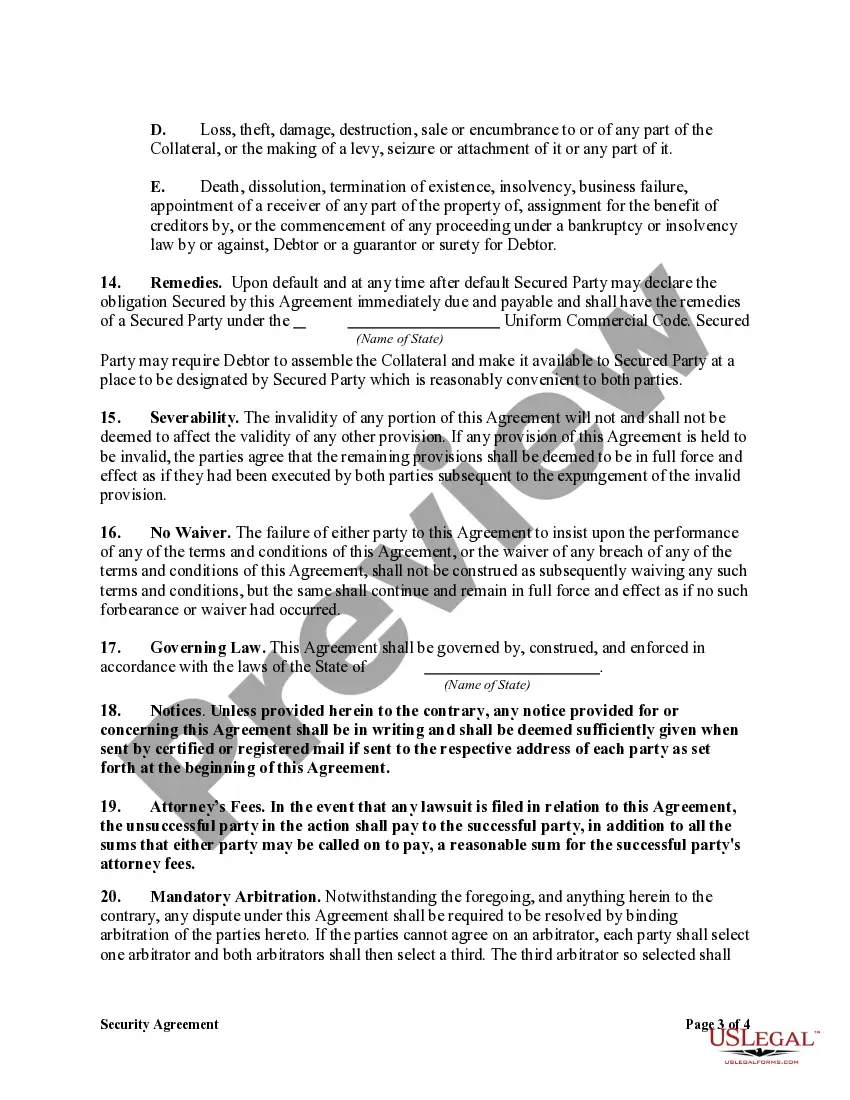

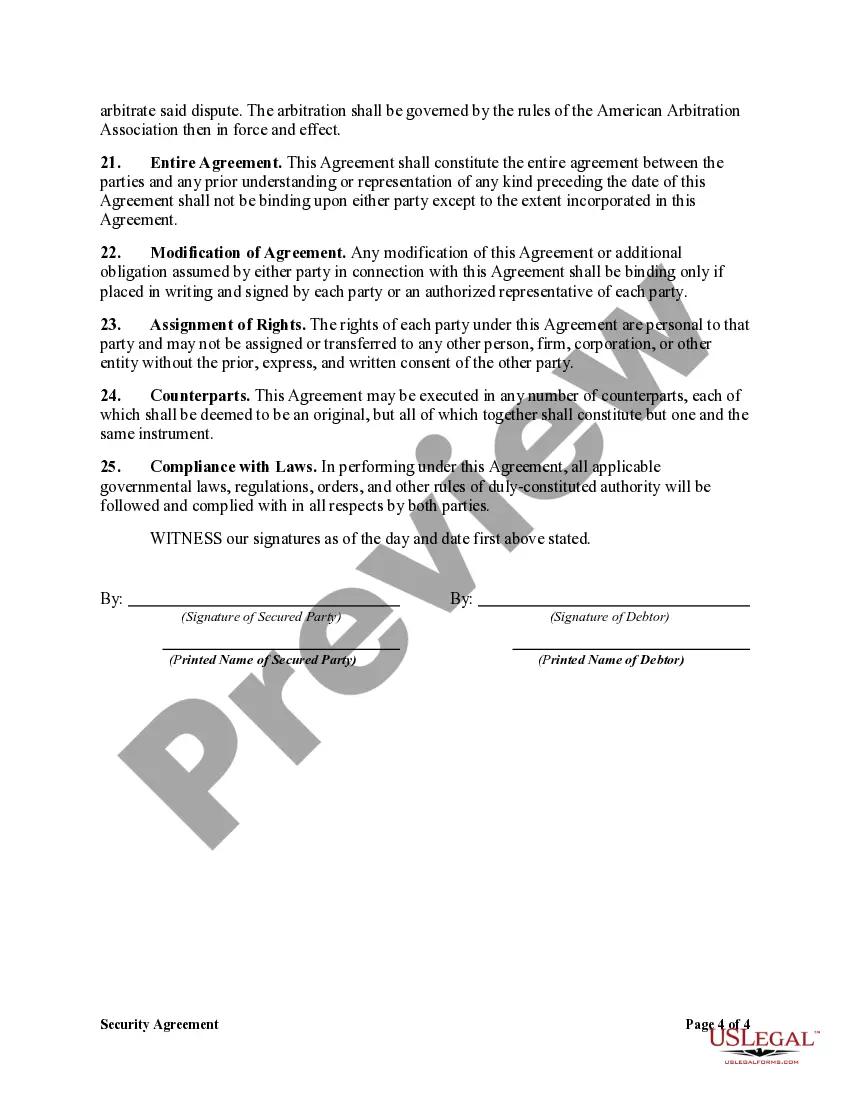

A Tennessee Security Agreement in Equipment for Business Purposes, securing a promissory note, is a legally binding contract that outlines the terms and conditions for the lateralization of specific equipment to guarantee payment on a promissory note. This agreement is crucial for businesses seeking financing or loans, as it provides security to lenders and ensures that they have means to recover their investment in the event of default. Keywords: Tennessee, Security Agreement, Equipment, Business Purposes, Promissory Note, Lateralization, Financing, Loans, Lenders, Default. There can be different types of Tennessee Security Agreements in Equipment for Business Purposes, securing a promissory note, depending on the specific circumstances and needs of the parties involved. Here are a few types: 1. General Tennessee Security Agreement: This type of agreement involves securing all types of equipment owned by the business as collateral for the promissory note. It provides a broader cover for lenders, encompassing various equipment assets. 2. Specific Equipment Security Agreement: In this type of agreement, only specific equipment, as defined in the contract, will be pledged as collateral. It allows businesses to retain ownership and control over non-pledged equipment while still securing financing for specific items. 3. Floating Lien Security Agreement: A floating lien agreement grants the lender a security interest in the business's equipment, which includes all present and future equipment. This type of agreement is beneficial when businesses have ongoing or changing equipment needs. 4. Third-Party Collateral Security Agreement: In some cases, businesses may secure a promissory note by offering equipment that is owned by a third party as collateral. This could involve arrangements with suppliers or equipment leasing companies, where they agree to pledge their equipment on behalf of the borrowing business. These various types of Tennessee Security Agreements in Equipment for Business Purposes provide flexibility for both lenders and borrowers in tailoring the terms to suit their unique requirements. It is important for businesses to carefully consider the type of agreement that best aligns with their financing needs and to seek legal advice to ensure compliance with Tennessee laws and regulations.A Tennessee Security Agreement in Equipment for Business Purposes, securing a promissory note, is a legally binding contract that outlines the terms and conditions for the lateralization of specific equipment to guarantee payment on a promissory note. This agreement is crucial for businesses seeking financing or loans, as it provides security to lenders and ensures that they have means to recover their investment in the event of default. Keywords: Tennessee, Security Agreement, Equipment, Business Purposes, Promissory Note, Lateralization, Financing, Loans, Lenders, Default. There can be different types of Tennessee Security Agreements in Equipment for Business Purposes, securing a promissory note, depending on the specific circumstances and needs of the parties involved. Here are a few types: 1. General Tennessee Security Agreement: This type of agreement involves securing all types of equipment owned by the business as collateral for the promissory note. It provides a broader cover for lenders, encompassing various equipment assets. 2. Specific Equipment Security Agreement: In this type of agreement, only specific equipment, as defined in the contract, will be pledged as collateral. It allows businesses to retain ownership and control over non-pledged equipment while still securing financing for specific items. 3. Floating Lien Security Agreement: A floating lien agreement grants the lender a security interest in the business's equipment, which includes all present and future equipment. This type of agreement is beneficial when businesses have ongoing or changing equipment needs. 4. Third-Party Collateral Security Agreement: In some cases, businesses may secure a promissory note by offering equipment that is owned by a third party as collateral. This could involve arrangements with suppliers or equipment leasing companies, where they agree to pledge their equipment on behalf of the borrowing business. These various types of Tennessee Security Agreements in Equipment for Business Purposes provide flexibility for both lenders and borrowers in tailoring the terms to suit their unique requirements. It is important for businesses to carefully consider the type of agreement that best aligns with their financing needs and to seek legal advice to ensure compliance with Tennessee laws and regulations.