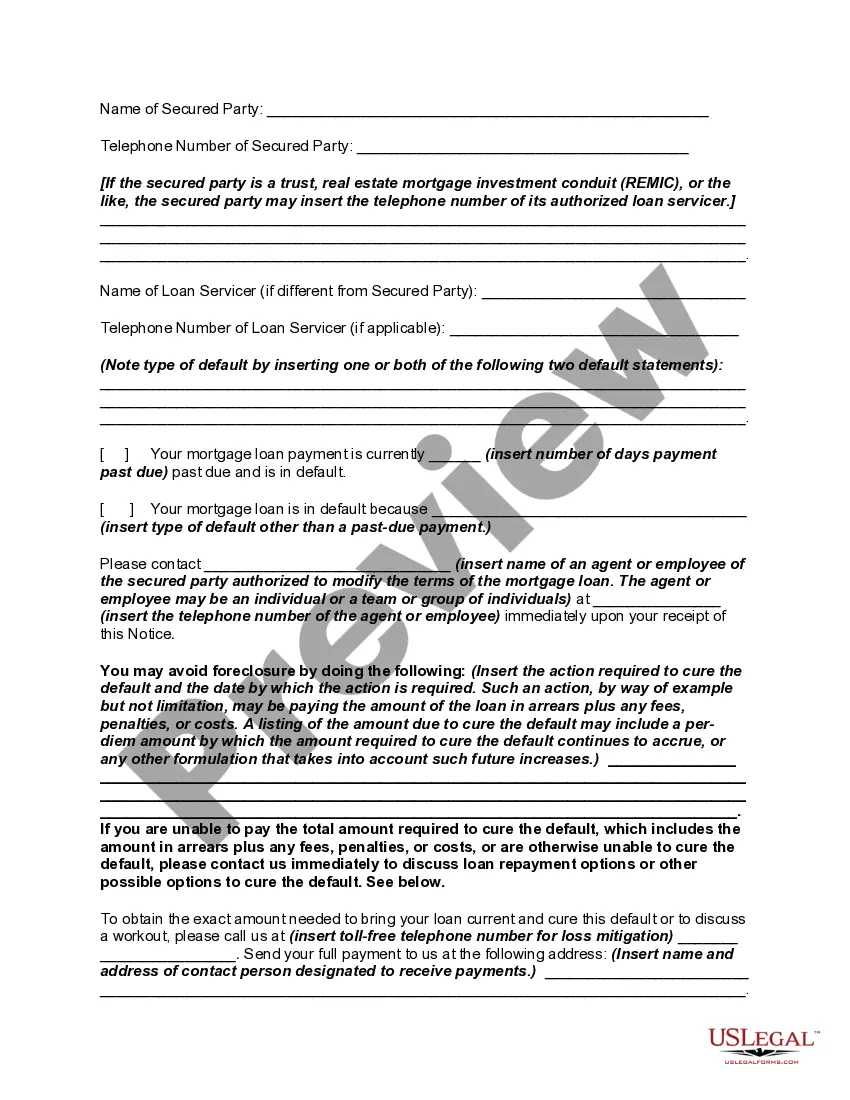

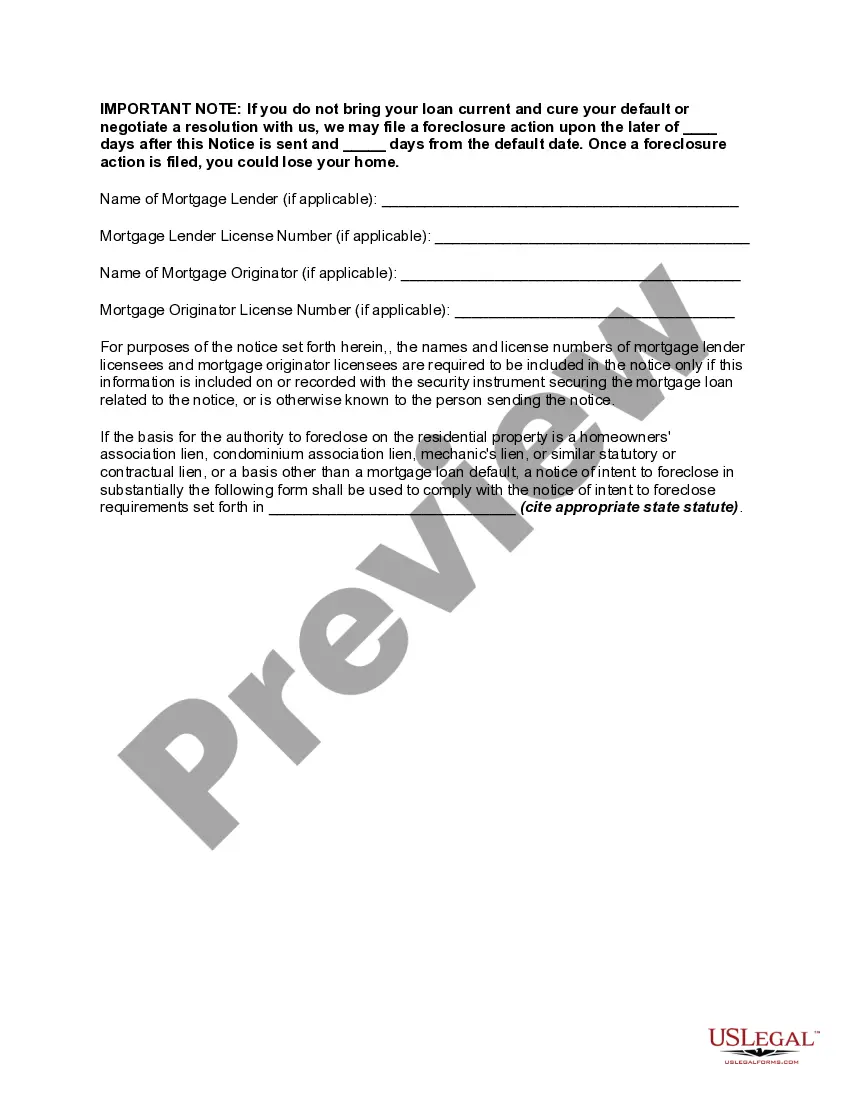

A number of states have enacted measures to facilitate greater communication between borrowers and lenders by requiring mortgage servicers to provide certain notices to defaulted borrowers prior to commencing a foreclosure action. The measures serve a dual purpose, providing more meaningful notice to borrowers of the status of their loans and slowing down the rate of foreclosures within these states. For instance, one state now requires a mortgagee to mail a homeowner a notice of intent to foreclose at least 45 days before initiating a foreclosure action on a loan. The notice must be in writing, and must detail all amounts that are past due and any itemized charges that must be paid to bring the loan current, inform the homeowner that he or she may have options as an alternative to foreclosure, and provide contact information of the servicer, HUD-approved foreclosure counseling agencies, and the state Office of Commissioner of Banks.

The Tennessee Notice of Intent to Foreclose is a legal document that notifies the borrower of a mortgage loan default that the lender intends to initiate foreclosure proceedings. This notice is crucial in keeping the borrower informed about the potential risks involved in the event of continued non-payment or default. Keywords: Tennessee, Notice of Intent to Foreclose, Mortgage Loan Default, foreclosure proceedings, borrower, lender, non-payment, risks. Types of Tennessee Notice of Intent to Foreclose — Mortgage Loan Default: 1. Pre-Foreclosure Notice: This type of notice is typically the initial communication from the lender to the borrower, informing them of the imminent default on their mortgage loan and explaining the consequences and steps towards foreclosure. 2. Formal Notice of Intent to Foreclose: In this stage, the lender issues a formal written notice stating their intention to foreclose on the property due to prolonged default or non-payment. The notice generally includes information about the outstanding debt, the required actions to prevent foreclosure, and the timeframe within which the borrower must respond. 3. Notice of Intent to Accelerate: If the borrower continues to default on their mortgage loan, the lender may issue a Notice of Intent to Accelerate. This notice notifies the borrower that the entire loan amount will become due unless the default is cured within a specified period. Failure to comply may result in foreclosure proceedings. 4. Notice of Foreclosure Sale: After exhausting all efforts to resolve the default, the lender may proceed with scheduling a foreclosure sale. The Notice of Foreclosure Sale serves as a public announcement of the pending sale, providing details such as the date, time, and location of the auction of the property. 5. Notice of Redemption: In Tennessee, borrowers have the right to redeem their property within a specified period after the foreclosure sale. The Notice of Redemption informs the borrower about their redemption rights and the timeframe within which they must proceed with the necessary steps to reclaim their property. 6. Notice of Non-Responsiveness: This notice is sent to borrowers who have not responded to previous notices or failed to take corrective actions regarding their mortgage loan default. It often signifies that the foreclosure process will proceed without further communication or negotiations. It is important to note that the names and specific requirements for these notices may vary under Tennessee law. Borrowers facing loan default should consult legal professionals familiar with Tennessee foreclosure statutes to understand the precise nature of the notices they receive and the corresponding actions they must take to protect their rights and interests.The Tennessee Notice of Intent to Foreclose is a legal document that notifies the borrower of a mortgage loan default that the lender intends to initiate foreclosure proceedings. This notice is crucial in keeping the borrower informed about the potential risks involved in the event of continued non-payment or default. Keywords: Tennessee, Notice of Intent to Foreclose, Mortgage Loan Default, foreclosure proceedings, borrower, lender, non-payment, risks. Types of Tennessee Notice of Intent to Foreclose — Mortgage Loan Default: 1. Pre-Foreclosure Notice: This type of notice is typically the initial communication from the lender to the borrower, informing them of the imminent default on their mortgage loan and explaining the consequences and steps towards foreclosure. 2. Formal Notice of Intent to Foreclose: In this stage, the lender issues a formal written notice stating their intention to foreclose on the property due to prolonged default or non-payment. The notice generally includes information about the outstanding debt, the required actions to prevent foreclosure, and the timeframe within which the borrower must respond. 3. Notice of Intent to Accelerate: If the borrower continues to default on their mortgage loan, the lender may issue a Notice of Intent to Accelerate. This notice notifies the borrower that the entire loan amount will become due unless the default is cured within a specified period. Failure to comply may result in foreclosure proceedings. 4. Notice of Foreclosure Sale: After exhausting all efforts to resolve the default, the lender may proceed with scheduling a foreclosure sale. The Notice of Foreclosure Sale serves as a public announcement of the pending sale, providing details such as the date, time, and location of the auction of the property. 5. Notice of Redemption: In Tennessee, borrowers have the right to redeem their property within a specified period after the foreclosure sale. The Notice of Redemption informs the borrower about their redemption rights and the timeframe within which they must proceed with the necessary steps to reclaim their property. 6. Notice of Non-Responsiveness: This notice is sent to borrowers who have not responded to previous notices or failed to take corrective actions regarding their mortgage loan default. It often signifies that the foreclosure process will proceed without further communication or negotiations. It is important to note that the names and specific requirements for these notices may vary under Tennessee law. Borrowers facing loan default should consult legal professionals familiar with Tennessee foreclosure statutes to understand the precise nature of the notices they receive and the corresponding actions they must take to protect their rights and interests.